LendEDU’s Take

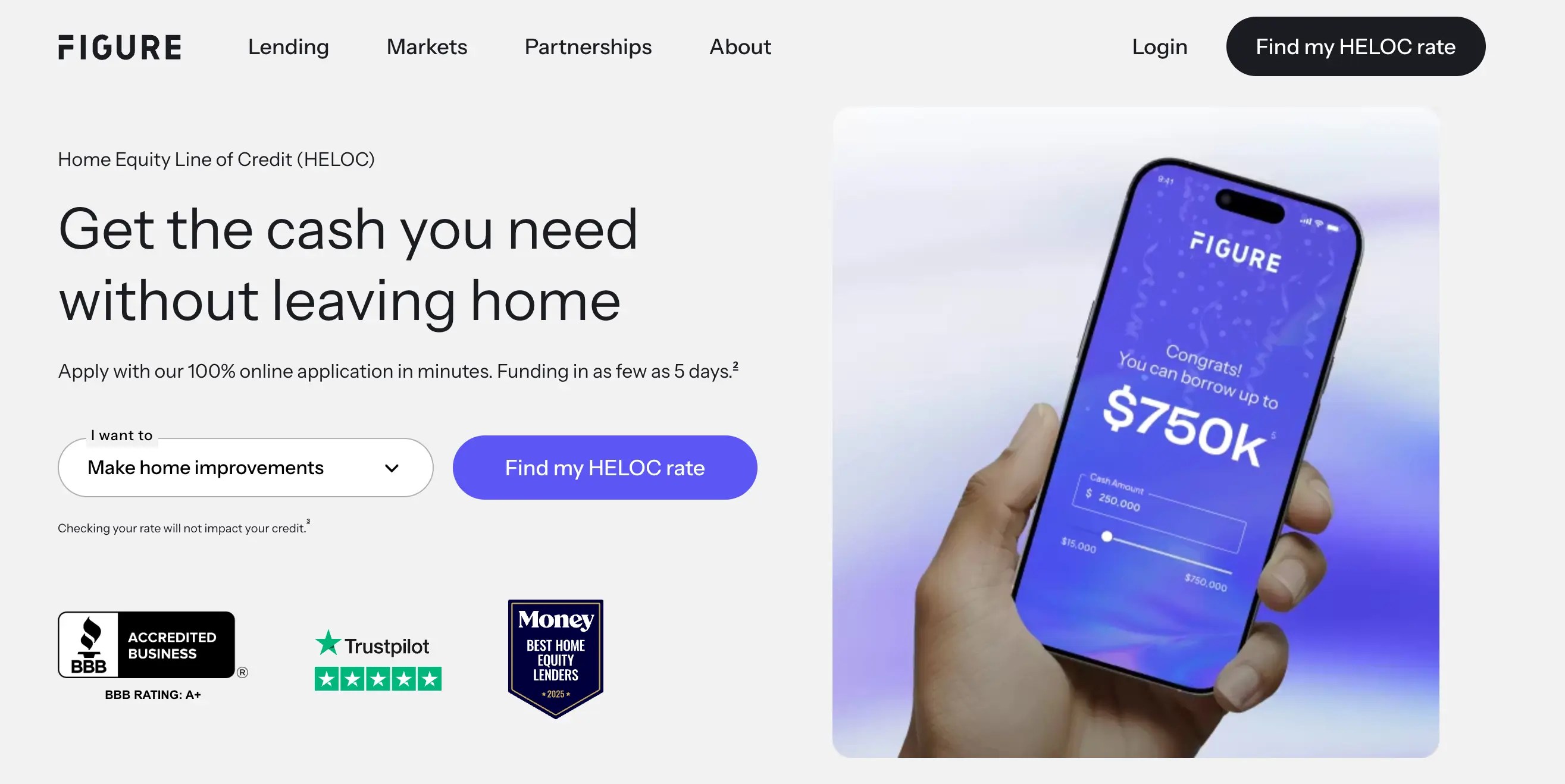

Figure is a top pick for a HELOC thanks to its offering of fixed rates, fast funding, and a fully online process. Just know it comes with a higher origination fee, limited availability, and you’ll have to draw the full amount upfront, which makes it feel a bit more like a home equity loan.

Rates (APR)

8.35% – 16.55%ⓘ

fixed or variableFunding

$15K – $750K

Repayment (Yrs.)

10, 15, 20, or 30

What we like

- Fixed APR HELOCs

- No in-person appraisal needed

- Redraw up to 100% of funds

- Checking your rate doesn’t affect your credit score

Things to keep in mind

- May charge an origination fee

- Typically requires good to excellent credit

Figure was founded in 2018 and has quickly made a name for itself by rethinking how home equity borrowing works. Instead of the slower, paperwork-heavy process you’ll find with many traditional lenders, Figure leans into a fully digital experience that can deliver approvals in minutes and funding in just a few days.

That digital-first approach carries through to its HELOC. The entire application happens online, and in many cases, there’s no need for an in-person appraisal. It’s a much faster and more streamlined option compared to the typical weeks-long timeline you might expect.

Here’s everything to know in our full Figure HELOC review.

Table of Contents

- How does a Figure HELOC work?

- Figure HELOC requirements

- Pros and cons of Figure HELOCs

- How Figure HELOCs compare to other options

- Is Figure lending legit? Customer reviews

- How to contact Figure

- How to apply for a Figure HELOC

- Is a Figure HELOC a good idea?

- FAQ

- Recap of our Figure Lending HELOC review

How does a Figure HELOC work?

Figure HELOC rates and terms

HELOCs are typically lines of credit that you can draw funds from as needed. Figure HELOCs work a bit differently in that, when you close on the loan, you must draw the full amount. In that way, it almost works like a home equity loan. However, as you repay the line of credit, you can redraw up to 100% of the funds during the draw period.

In addition, while many lenders only offer variable rates that change over time, Figure offers both variable and fixed-rate options. Its fixed-rate draw option allows you to lock in a new fixed rate for each draw you make from the line of credit, which can give you more predictability in your repayment.

Here’s a closer look at Figure’s HELOC rates and terms.

| Terms | Details |

| Rates (APR) | 6.10% – 14.74% fixed or variable* |

| Loan amounts | $15,000 – $750,000 |

| Min. draw requirement | 100% of the loan amount (minus the origination fee) at the time of loan origination; additional draws can be made during draw period |

| Draw period | 2 – 5 years |

| Repayment period | 10, 15, 20 or 30 years |

| Fees | Origination fee up to 4.99%; Possible manual notarization and recording fees |

| Discounts | 0.25% autopay rate discount |

| Unique features | Automation in approving loans, eNotary, blockchain, & AI technology |

Figure HELOC draw period and repayment

Figure’s HELOC follows a pretty straightforward structure, broken into three main stages:

- Initial draw: Once you’re approved, you’ll receive the full loan amount upfront (minus any fees). Instead of drawing funds as needed from the start, you begin with the full balance.

- Draw and repayment period: You’ll start making monthly payments right away at your fixed rate. As you pay down your balance, you can access those funds again during the two- to five-year draw period. Any additional withdrawals come with their own rates.

- Repayment period: After the draw period ends, you won’t be able to borrow more. You’ll continue paying off the remaining balance over a set term of 10, 15, 20, or 30 years, depending on what you selected.

Does Figure’s HELOC have an early payoff penalty?

No, it doesn’t. You can pay off your balance early without any extra fees. That’s a nice perk, especially since some lenders charge you for closing out your loan ahead of schedule.

Unique features of a Figure HELOC loan

Fully digital process

Figure keeps everything online, from application to funding. You can apply through its website or app, and there’s no need for in-person appointments or stacks of paperwork.

Blockchain technology

Behind the scenes, Figure uses blockchain to help process and store loan data more securely. For you, that mostly shows up as a smoother, faster experience with fewer manual delays.

No in-person appraisal (AVM technology)

Instead of sending someone out to appraise your home, Figure uses automated valuation models to estimate your property’s value. It pulls from market data and recent sales to come up with a number quickly, which helps speed up approval.

Funding in as little as 5 days

Because everything is streamlined, funding can happen pretty quickly. In some cases, borrowers get their money in as little as five business days, which is faster than many traditional HELOCs.

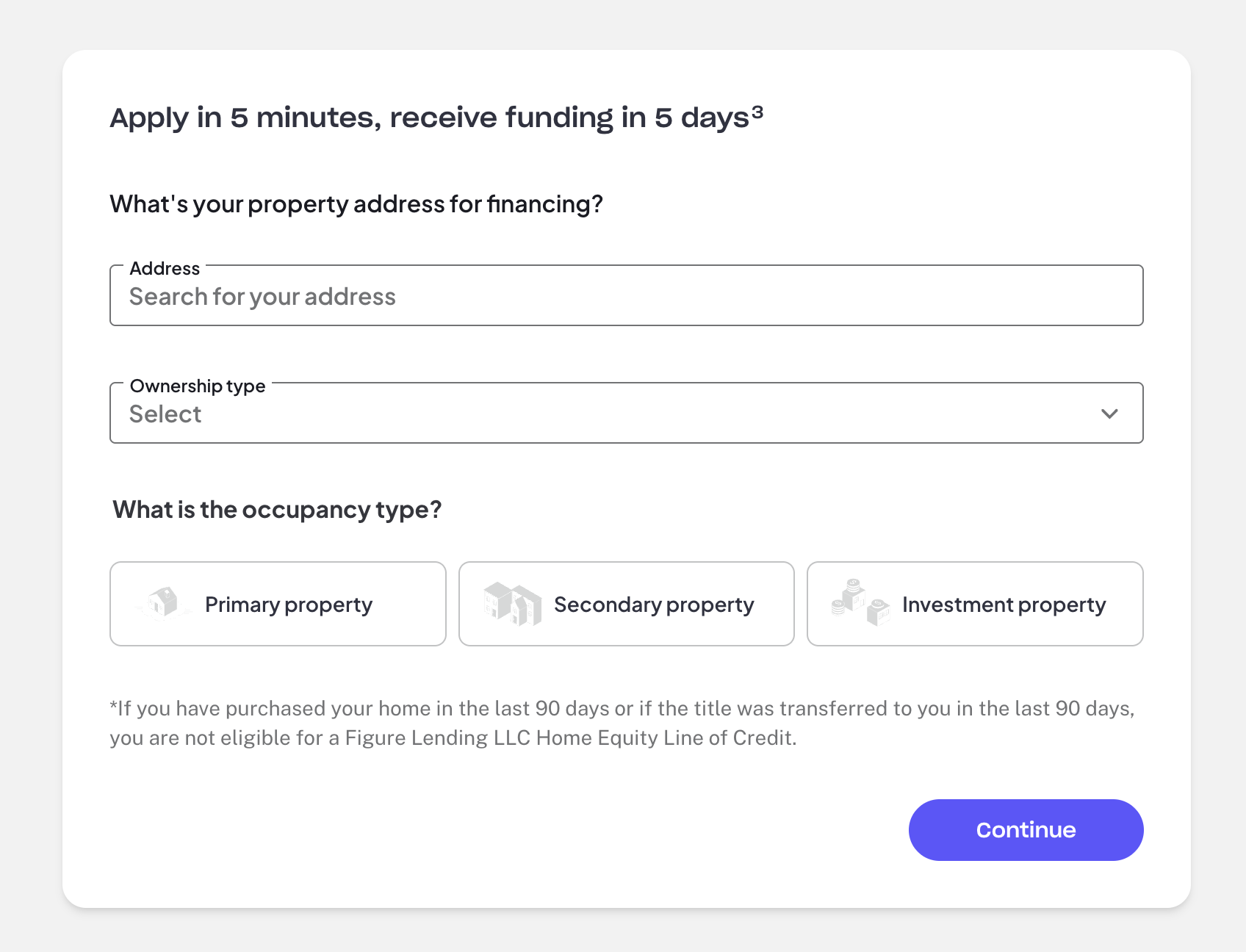

Figure HELOC requirements

To qualify for a Figure HELOC, you must meet the following criteria:

| Requirement | Details |

| Eligible properties | Single-family residences, townhomes, planned urban developments, and most condos are eligible properties |

| Eligible states | 49 and D.C. (not available in Hawaii) |

| Max LTV | 85% |

| Maximum DTI | 50% |

| Minimum credit score | 640, but 720+ is advised |

How does Figure calculate your home equity?

Your home’s value determines how much you can borrow with a Figure HELOC. Because Figure uses your home as collateral, the loan-to-value ratio (LTV), calculated by dividing your current mortgage balance by your home’s appraised value, is a major factor.

To determine how much you can borrow, Figure calculates your combined LTV (CLTV) by adding the desired HELOC amount to your current mortgage balance and dividing it by your home’s appraised value. Figure typically lends up to an 85% CLTV, but qualifying for this higher range requires a strong credit score, significant income, and assets. For most borrowers, Figure suggests having at least 30% equity in your home and a CLTV below 80%.

Example

If your home is valued at $800,000 and your mortgage balance is $450,000, you might qualify to borrow up to $190,000, representing 80% of your home’s value.

How a Figure appraisal works

Figure uses an AVM to estimate your home’s market value. This model analyzes recent sales, public records, and neighborhood market trends to quickly generate a reliable valuation—often within a few days. During the application, you’ll be asked to provide basic property details like the type of home, year built, square footage, number of bedrooms and bathrooms, and any significant renovations.

By skipping the manual appraisal, Figure significantly shortens the approval timeline.

Pros and cons of Figure HELOCs

Let’s explore the risks and benefits of Figure’s HELOC.

Pros

-

Fast approval

One of Figure’s major advantages is the speed of approval. It uses eNotary to avoid in-person appraisals and closings.

-

Quick disbursement

Figure claims to disburse loans in as little as five days.

-

Ability to re-draw 100% of the funds

If you repay the funds in your line of credit during the draw period, you can re-draw up to 100% of them to use for additional expenses.

Cons

-

Short draw period

If you’re seeking a lengthy draw period, Figure might not be the best fit. Its draw periods last between two and five years.

-

Full loan balance upfront

Figure requires borrowers to draw the full loan balance at closing, which might not offer the flexibility you need.

-

High credit score likely required

Figure lists a minimum credit score of 640, but 720+ is advised for approval and the best rates.

How Figure HELOCs compare to other options

Figure’s HELOC can be a great fit, but it’s not the only option out there. Depending on what matters most to you, like flexibility, fees, or how you access your funds, another lender might make more sense. The options below are a good place to start comparing.

Check out our full roundup of the best HELOC lenders.

product

HELOC

HELOC

HELOC

Home equity investment

funding amounts

$15,000 – $750,000

$5,000 – $400,000 ($100,000 in some states)

$10,000 – $1 million

$15,000 – $600,000

Min. credit score

640

640

670

585

Figure HELOC vs. home equity investment

A home equity investment (HEI) works very differently from a HELOC like Figure’s. Instead of borrowing money and making monthly payments, you receive a lump sum in exchange for giving the company a share of your home’s future value.

That means no monthly payments, but it also means you’ll owe more if your home appreciates over time. With Figure, you’re still making regular payments, but you exclusively benefit from any increase in its value.

HEIs may appeal to borrowers who want to avoid monthly payments altogether, or those who don’t qualify for a HELOC. HEI companies typically accept lower credit scores. Hometap, for example, lists a minimum credit score of 585. Meanwhile, a HELOC like Figure’s is better suited for those who want predictable repayment and have decent credit.

Read a more in-depth comparison between HELOCs and an HEA from Hometap.

How is a Figure HELOC different from a home equity loan?

Figure’s HELOC and a traditional home equity loan can look similar at first, especially since both offer fixed rates and require you to start repaying right away.

The biggest difference comes down to flexibility. With a home equity loan, you receive a lump sum and begin paying it back, with no option to borrow more without taking out a new loan. With Figure’s HELOC, you also receive your funds upfront, but as you repay the balance, you can draw from your line again during the draw period.

If you prefer a simple, one-time loan with a fixed repayment schedule, a home equity loan may be a better fit. If you like the idea of reusing your credit line as you pay it down, Figure’s HELOC offers a bit more flexibility.

Read more about the top-rated home equity loans.

Is Figure lending legit? Customer reviews

| Source | Customer rating | Number of reviews |

| Trustpilot | 4.8/5 | 4,541 |

| Better Business Bureau (BBB) | 1.42/5 | 38 |

Overall, Figure comes across as a legitimate lender with a strong track record, especially on Trustpilot, where it has a high rating across thousands of reviews. That kind of volume usually points to a consistently positive experience for many borrowers.

That said, reviews aren’t as strong across every platform. On the BBB, the rating is much lower, though it’s based on a relatively small number of reviews. Figure does still hold an A+ rating from the BBB itself, which reflects how it handles complaints rather than customer sentiment.

As with most lenders, experiences can vary. But taken together, the high volume of positive feedback suggests that many borrowers have had a smooth experience with Figure’s process.

How to contact Figure

If you need help with your application or have questions about your loan, Figure offers a few ways to get in touch:

- Email (general inquiries): [email protected] or [email protected]

- Phone (general inquiries): 888-819-6388

- Phone (existing loans): 888-527-1950

- Live chat: Available on Figure’s website

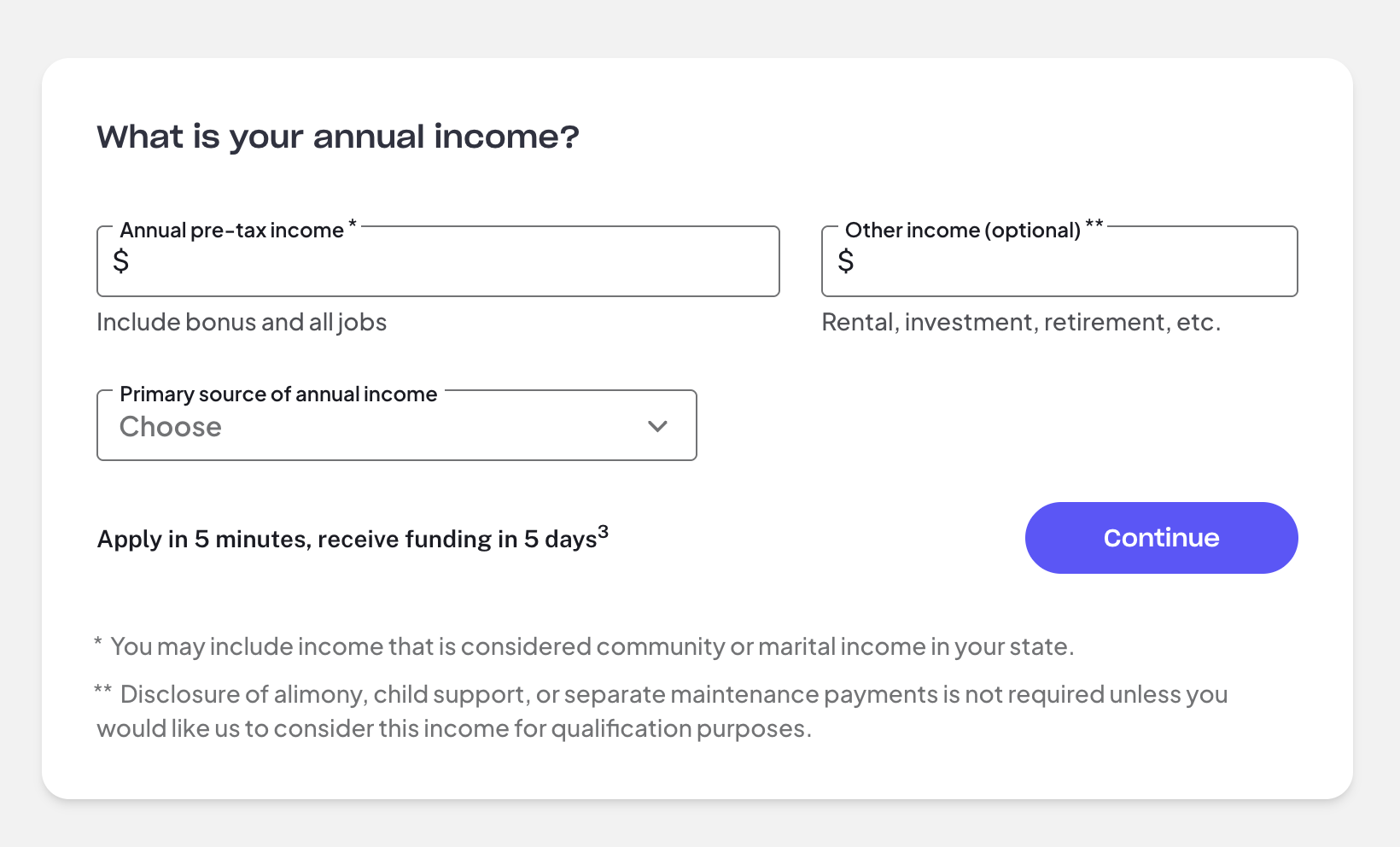

How to apply for a Figure HELOC

Applying for a Figure HELOC is pretty straightforward, especially compared to traditional lenders that require paperwork and in-person appointments. You can do everything online, and in some cases, get a final decision in just minutes.

Here’s what the process looks like:

Is a Figure HELOC a good idea?

A Figure HELOC can be a solid option, but it really comes down to how you plan to use your home equity.

If you like the idea of fixed rates, fast funding, and a fully online process, Figure stands out. It’s especially appealing if you want predictable monthly payments and don’t want to deal with the uncertainty that comes with variable-rate HELOCs.

That said, it’s not the best fit for everyone. Since you have to draw the full amount upfront, it may not work as well if you only need occasional access to funds. The origination fee can also be on the higher side, which is something to factor into your decision.

In general, Figure’s HELOC makes the most sense if you want speed, simplicity, and predictable payments. If flexibility or minimizing upfront costs is more important, you may want to compare a few other options before moving forward.

FAQ

Do you need to tell Figure what the funds are used for?

No, you don’t. Figure doesn’t ask how you plan to use the money during the application process, so you have flexibility in how you put your funds to work.

Are there any insurance requirements?

Yes. You’ll need to have homeowners’ insurance in place before your HELOC can be approved. The coverage just needs to be enough to protect the value of your home, which is pretty standard for this type of loan.

Can you back out of a HELOC contract?

Yes, you can. While you’re applying, you’re not locked into anything, so you can walk away at any point before accepting the loan.

Even after you’re approved, you can still decline the offer as long as the funds haven’t been sent. And once you do receive the funds, you typically have a three-day window to cancel the loan without penalty under federal law.

Can you close your HELOC account at any time?

Yes, but it depends on your loan terms. In most cases, you’ll need to pay off your remaining balance before closing the account, and there may be fees depending on your agreement.

It’s a good idea to double-check your contract so you know exactly what to expect before closing your HELOC.

How we rated Figure

We designed LendEDU’s editorial rating system to help readers find companies that offer the best home equity products. Our system awards higher ratings to companies with affordable solutions, positive customer reviews, and online transparency of benefits and terms.

We compared Figure to several home equity companies, using hundreds of data points from company websites, public disclosures, customer reviews, and direct communication with company representatives. We weighted, scored, and combined each factor to produce a final editorial rating. This rating is expressed on a scale from 1 to 5, with 5 being the highest possible score. Our take is represented in our rating and best-for designation, recapped below.

Recap of our Figure Lending HELOC review

Related articles

About our contributors

-

Written by Rebecca Lake, CEPF®

Written by Rebecca Lake, CEPF®Rebecca Lake is a certified educator in personal finance (CEPF®) and freelance writer specializing in finance.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.