Filling out the Free Application for Federal Student Aid (FAFSA) has always been a chore for students and parents alike, but a necessary one at that. Part of the reason why it’s so difficult is because you’ll need to take full stock of your finances—and for parents with lots of accounts, that may not be so easy.

That’s why you might be tripped up by question 40 of the FAFSA, which asks for the dollar amount of the parent’s assets. It’s not always clear what counts as an asset or not, and your answer can affect the student’s eligibility for financial aid.

We’ll break down exactly how to answer question 40 of the FAFSA so you can move on with your college plans.

Table of Contents

How to answer question 40 of the FAFSA

Not everyone needs to report parental assets on the FAFSA. First, you’ll establish whether you’re a dependent student. Typically, parents of unmarried undergraduates below the age of 24 will need to complete this question.

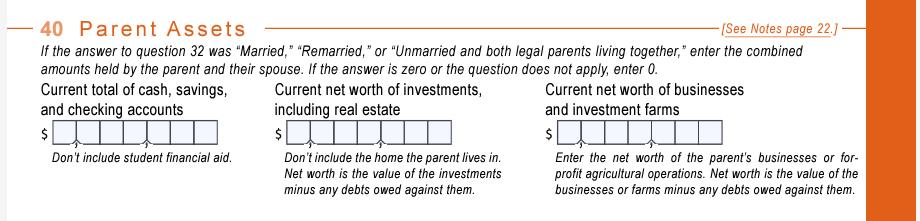

In the 2024-25 FAFSA, you’ll report parental assets on Question 40 of the FAFSA:

When it comes to reporting your assets, here are a few general rules to keep in mind for each of these three categories:

- Tally up each box for the day you submit the form—not from old financial statements.

- If you’re in the red regarding your total assets for a certain category, simply report it as “0” rather than a negative number.

- If you’re lucky enough to have $10 million or more for a certain category, simply report it as “9,999,999” since larger amounts won’t fit in the box.

What counts as current total of cash, savings, and checking accounts?

It’s usually pretty easy to calculate this first box since most people keep closer tabs on the money in their bank accounts.

Remember to include any assets held at other banks, such as if you opened an account during the year to earn a bank sign-up bonus and any physical cash you have stuffed under your mattress or buried in the backyard.

What counts as current net worth of investments, including real estate?

Things get a bit trickier for most people when it comes to the value of their investments, especially because the fine print actually excludes many types of investments.

Parents should not list the following types of investment assets on question 40 of the FAFSA:

- Primary home

- Life insurance

- ABLE accounts

- Retirement plans, such as 401(k)s or IRAs

- Education savings accounts for other children, such as Coverdell or 529 plans

On the other hand, parents should list these types of investment assets:

- Taxable brokerage accounts

- Investment real estate properties, such as rental units

A key point here is that parents are required to report the asset’s “net worth”—i.e., its value minus any debts tied to it. If parents own a $300,000 cabin they rent out on Airbnb, for example—but still owe $200,000 on that cabin’s mortgage, then they’d only report a net worth of $100,000.

What counts as current net worth of businesses and investment farms?

If the parents own any for-profit businesses or farms, they’ll also be required to list the net worth of these assets. If you only grow food for your own family to eat, however—without selling anything—then you won’t have to list this as an asset on the FAFSA.

The goal is to get your child grant and scholarship offers but be careful not to overlook other types of aid. For example, the FAFSA will ask if your child is interested in work-study opportunities. Answering no to this question will exclude your child from any work-study jobs, which is how many colleges hire their employees.

Eric Kirste, CFP®

Ad

Information advertised valid as of 08/03/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/03/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/03/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.

4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered.

7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION.

Sallie Mae loans are made by Sallie Mae Bank.

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.

4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered.

7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION.

Sallie Mae loans are made by Sallie Mae Bank.

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.

4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered.

7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION.

Sallie Mae loans are made by Sallie Mae Bank.

Why your answer to question 40 of the FAFSA must be accurate

Governments and schools rely on people answering the FAFSA questions correctly in order to make sure financial aid gets to the people who need it most. If you report an incorrect number for parental assets, you could affect the student’s ability to get financial aid and may even incur other penalties.

What happens if you lie on question 40 of the FAFSA?

People are often tempted to lie about their assets on the FAFSA since having fewer assets can mean bigger financial aid payouts. You may be able to get away with it if you’re lucky, but it’s not a risk worth taking.

Each year, about 18% of FAFSA filers are selected to verify the information they provide. If you cannot verify these items, your financial aid package may be delayed or reduced. If you’ve already received those funds, you may have to pay them back, even if you’ve already spent them.

In addition, people who blatantly lie on question 40 of the FAFSA may face a fine of up to $20,000 and/or be sent to prison for committing fraud.

Can you change your answers on the FAFSA?

Not everyone is trying to intentionally defraud the system when they report parental assets on the FAFSA. If you’ve discovered an error after the fact, you can easily fix it.

To make changes to your FAFSA, you can contact your school to notify them of the error, and the correct amount to report. You can also mail a paper FAFSA correction form, or submit a change in your online account. Your parents may also need to sign off on the change in their StudentAid.gov account.

For help with the FAFSA, start with the child’s high school counselors. They may have access to counselors and financial aid experts who can make the process easier by talking with families about FAFSA’s importance. Start the process early, they can connect parents to workshops and other resources. Check the Federal Student Aid Q&A for commonly asked questions. Finally, contact the university’s/college’s financial aid office for resources and help.

Eric-Kirste, CFP®

About our contributors

-

Written by Lindsay VanSomeren

Written by Lindsay VanSomerenLindsay VanSomeren is a personal finance writer living in Suquamish, Washington. She's passionate about helping people manage their money better so that they can live the life they want. In her spare time, she enjoys outdoor adventures, reading, and learning new languages and hobbies.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Eric Kirste, CFP®

Reviewed by Eric Kirste, CFP®Eric Kirste, CFP®, CIMA®, AIF®, is a founding principal wealth manager for Savvy Wealth. Eric brings more than two decades of wealth management experience working with clients, families, and their businesses, and serving in different leadership capacities.