Building equity is one of the most valuable parts of owning a home and over time, it can become one of your biggest financial assets. The good news? You don’t have to wait 30 years to see progress.

With the right strategies, you can speed up the process—and improve your financial flexibility along the way. In this article, we’ll walk through what home equity is, why it matters, and nine practical ways to build it faster.

Table of Contents

- What is building equity?

- Why building equity is a good thing

- How to build home equity faster

- 1. Make more frequent payments

- 2. Increase the size of your mortgage payment

- 3. Make extra mortgage payments

- 4. Choose a shorter mortgage repayment term

- 5. Lower your interest rate

- 6. Renovate your home

- 7. Keep your home in good repair

- 8. Make a larger down payment

- 9. Combine quick wins with long-term equity growth

- FAQs

What is building equity?

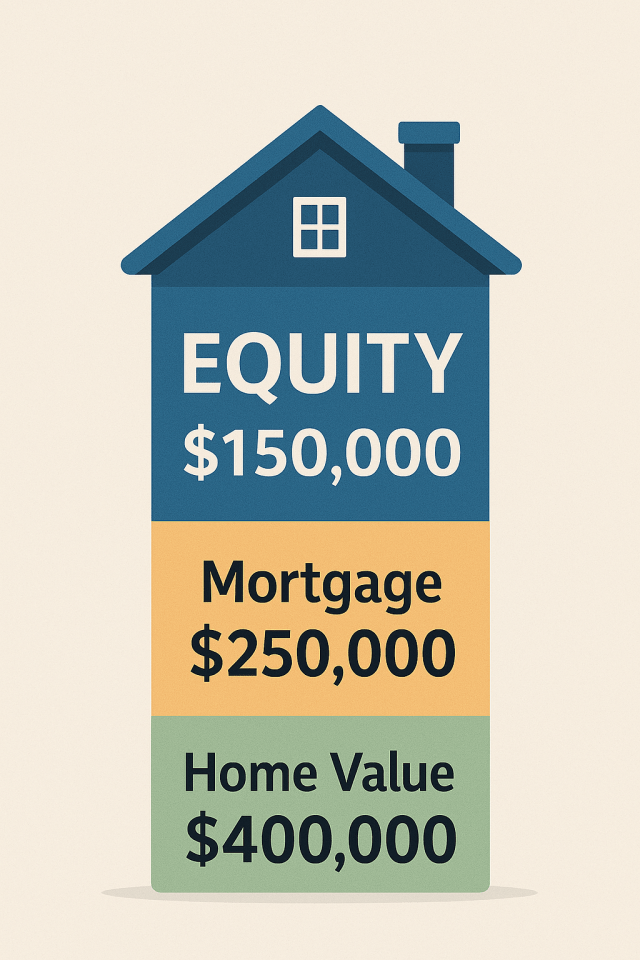

Home equity is the difference between what your home is worth and what you still owe on your mortgage. It’s calculated using this formula:

Home value – loan balance = home equity

For example, if your home is valued at $400,000 and you owe $250,000, your equity is $150,000. Your equity represents the portion of the home you truly own.

To estimate your home’s value, check recent sales in your area or ask a local real estate agent. You could also use online tools like those offered by Redfin. You can find your current loan balance on your most recent mortgage statement or through your lender’s online portal.

You can build equity over time in two ways—by paying down your mortgage and increasing your home value. The more equity you have, the more of your investment you’ve locked in. It’s a key part of long-term financial health.

Why building equity is a good thing

Home equity isn’t just a number—it’s a form of financial security. The more equity you build, the more options you’ll have down the road. Whether you’re staying put or planning for the future, equity gives you room to maneuver.

Here are a few examples of what building equity can do for you:

- Increase your net worth. Your home is an asset, and your mortgage is a liability. The difference between the two is your equity, which also counts toward your personal net worth. This means as your home’s value rises and loan balance drops, your net worth naturally increases.

- Support future borrowing. Equity can be accessed without selling your home. Many homeowners use a home equity loan or home equity line of credit (HELOC) to pay for major expenses or consolidate debt. It can be a great way to put your equity to work. Most home equity loan or HELOC lenders require at least 15% to 20% equity in your home to qualify, although, as top-rated lender Figure suggests, most borrowers should have around 30% before applying.

- Offer flexibility. With enough equity, you may be able to refinance into better loan terms or sell your home and keep the profit. Equity gives you more financial options when life changes.

Building equity turns your home into more than just a place to live. It becomes a financial resource you can use strategically. That’s why it pays to build equity faster if you can.

How to build home equity faster

There are two main ways to build equity in your home: pay down your mortgage or increase the value of the property. The fastest results usually come from doing both at once. Some strategies require extra money, but many don’t.

Below are nine ways to build equity faster:

1. Make more frequent payments

Most people make one mortgage payment each month. But if you split your monthly payment in half and pay every two weeks, you’ll make 26 half-payments in a year. That’s the same as 13 full payments each year, versus 12 if you just made a single monthly payment.

This extra payment helps reduce your loan balance faster. Over time, it can shorten your loan term and lower how much interest you pay.

You don’t need to double your payments—just shift the timing. Check with your lender before starting to make sure biweekly payments are allowed and properly applied to principal.

2. Increase the size of your mortgage payment

Adding even a small amount to your monthly mortgage payment can make a big difference. The key is to ask your lender to apply that extra amount directly to your loan’s principal.

When more of your payment goes to principal, your balance shrinks faster. That reduces how much interest you pay over time—and builds equity more quickly.

Try rounding up your payment or setting a fixed amount to add each month. Even $50 or $100 consistently can cut months or years off your loan.

Let’s say you have a $200,000 mortgage at 5% interest with a 30-year term. If you make no extra payments, you’ll be in debt for the full 30 years. But by adding just $100 each month, you could pay off your loan in about 25 years, as shown below:

| Standard Payment | With Extra Principal | |

| Mortgage amount | $200,000 | $200,000 |

| Loan term (amortization) | 30 years | 30 years |

| Interest rate | 5% | 5% |

| Extra monthly principal | $0 | $100 |

| Years to payoff | 30 years | ~25 years |

In this example, paying just $100 extra monthly knocks five years off the loan. Plus, repaying the loan faster saves more than $37,000 in interest. It’s a simple way to build equity faster, without a major change to your monthly budget.

3. Make extra mortgage payments

Anytime you have extra money—like a tax refund, work bonus, or gift—you can put it toward your mortgage. One-time lump-sum payments help reduce your loan balance faster.

You don’t need to schedule them regularly. Even occasional extra payments, when applied to the principal, can shorten your loan term and grow your equity.

Be clear with your lender that the money should go toward your principal balance—not just toward an upcoming monthly payment. That’s the only way it helps you build equity faster.

4. Choose a shorter mortgage repayment term

A shorter mortgage term—like 15 or 20 years instead of 30—helps you build equity faster. More of each payment goes to principal right away, and you pay off the loan in fewer years.

Shorter terms often come with lower interest rates, too. That means less total interest paid and more equity gained over time.

Monthly payments will be higher, so make sure it fits your budget. But if you can afford it, refinancing into a shorter term can save tens of thousands of dollars in the long run.

5. Lower your interest rate

Refinancing to a lower interest rate can help you build equity faster—even if your loan term stays the same. With a lower rate, more of each payment goes toward principal instead of interest.

That means your balance shrinks more quickly with each payment. Over time, you’ll build equity faster and pay less interest overall.

Be cautious about restarting your loan term. If you’ve already paid five years on a 30-year loan, try to refinance into a 25-year term—or shorter—to stay on track.

6. Renovate your home

Smart renovations can boost your home’s market value, which increases your equity. However, before starting a project, talk to a local real estate agent. They can help you estimate your home’s value before and after the renovation, so you can understand the project’s ROI.

If you can do some of the work yourself, you may also build “sweat equity.” Just make sure the cost of the project doesn’t outweigh the value it adds.

7. Keep your home in good repair

Ongoing maintenance helps protect your home’s value—and that protects your equity. Neglect can lead to bigger problems and costly repairs down the road.

Focus on key areas like the roof, plumbing, HVAC, exterior paint, and drainage. Keeping everything in good shape helps your home hold or increase its value over time.

When your home maintains its value, your equity grows naturally as you pay down your mortgage.

8. Make a larger down payment

One of the fastest ways to build equity is to start with more of it. A larger down payment means you owe less from day one—and own more of the home outright.

It can also help you avoid private mortgage insurance (PMI). PMI is usually required if you have less than 20% equity, though it depends on the loan type and lender.

This strategy works best for new buyers or anyone refinancing into a new loan.

9. Combine quick wins with long-term equity growth

Some equity strategies take time. Even if you’re making fast progress by paying down your mortgage, holding your home longer allows it to appreciate, increasing your equity passively.

Historically, homes have appreciated about 4% annually on average, which can add tens of thousands in equity over a five- to 10-year period. That growth, combined with your mortgage payments, builds equity from both directions.

To see how appreciation might affect your home’s value, try using a home appreciation calculator.

FAQs

How long does it take to build equity in your home?

It depends on your loan terms, payment habits, and local market conditions. Most people build equity slowly in the early years of a mortgage. You’ll build it faster by paying extra or if your home’s value increases.

How much equity can you build in a year?

There’s no set number—it depends on your payments and how much your home appreciates. Paying extra toward principal or refinancing into a shorter loan can speed it up. In a strong market, equity can grow even without changes to your payments.

Do manufactured homes build equity?

They can—but it depends on the home and how it’s classified. If the home is legally affixed to the land, it’s treated similarly to a site-built home and may appreciate with the local market. This allows you to build equity as the loan is paid down and the property value increases.

If the manufactured home is not affixed to land, it may depreciate over time like a vehicle, making it harder to build equity. However, you’ll still build some equity as any financing is paid down.

What can you do with home equity?

You may be able to borrow against it using a home equity loan, a HELOC, or even a cash-out refinance. The funds can be used for major expenses like renovations, education, or debt consolidation. Be sure to compare options and terms carefully.

Be consistent to build equity in a home fast

You don’t need a dramatic financial overhaul to build equity faster. Small, consistent steps can lead to real progress. Whether it’s rounding up your monthly payment, making one extra payment a year, or handling maintenance before it becomes costly—those actions add up.

Pick the strategies that fit your budget and your goals. Stay consistent, and revisit your plan when your finances or interest rates change.

Building equity is a long game, but it’s worth playing. The more equity you build, the more financial options you’ll have down the road.

About our contributors

-

Written by Megan Hanna, CFE, MBA, DBA

Written by Megan Hanna, CFE, MBA, DBADr. Megan Hanna is a finance writer with more than 20 years of experience in finance, accounting, and banking. She spent 13 years in commercial banking in roles of increasing responsibility related to lending. She also teaches college classes about finance and accounting.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Gail Urban, CFP®

Reviewed by Gail Urban, CFP®Gail Urban, CFP®, AAMS®, has been a licensed financial advisor since 2009, specializing in helping individuals. Before personal financial advising, she worked as a business financial manager in several industries for about 25 years.