How are boat loans calculated?

Boat loans are calculated using your loan amount, interest rate, and loan term. Your credit score largely determines how much you can borrow and at what rate. Your boat’s value plays a role, as well.

Older boats tend to be less expensive than newer boats. Used pontoons, for example, cost $8,000 to $12,000 on average. New pontoons can run anywhere from $19,000 to $65,000. No matter your boat’s price tag, down payment or trade-in funds can reduce your overall loan amount.

Keep in mind, though, that some lenders won’t finance boats older than 10 or 20 years. Lenders might also consider your boating history. After all, going from a jon boat to a skiff may be an easier sell than convincing a lender you can handle a 40-foot sailboat with no sailing experience.

How is the monthly payment for a boat loan calculated?

Your monthly payment amount depends on three primary factors, including your:

- Initial loan amount

- Interest rate

- Loan term

More specifically, we multiply your monthly interest rate by your loan amount. Then, we factor in your loan term to find your payment.

It might help to see these steps in action, so let’s say you’re borrowing $25,000 for your new pontoon. You qualify for a 7% interest rate, and you’re considering a 10-year term. Here’s what you’d pay monthly on your boat loan:

As long as you make each payment on time, you’ll pay about $290 each month. However, if you miss any payments, your lender might tack on late fees. Those fees can increase your monthly payments until you get caught up.

While paying extra toward your principal can help you save on interest and pay off your loan more quickly, it won’t lower your payment amount. Unless you refinance or consolidate, your boat loan payment won’t change.

How is the interest rate for a boat loan calculated?

Boat loan interest rates depend on two main elements: the prime rate and your credit score.

The prime rate is an industry standard set by the Federal Reserve. Most lenders use this as a benchmark to determine their own rates. Lenders then look at your credit to decide what rate you’ll qualify for.

The lower your interest rate, the less expensive your loan will be. In our previous example, we calculated a $290 monthly payment on a 10-year, $25,000 boat loan at 7% interest. But what if that interest rate jumped to 9%? How would your payments change?

Not only would your payment go up to around $317, but your interest expense would go up, too. Here’s a look at each loan’s borrowing cost:

While there’s only a two-percentage-point difference between these loans, the 9% interest rate costs nearly $4,000 more.

Calculating your interest expense is a necessary part of evaluating your loan offers. Keep in mind, though, that there are two ways to think about interest:

- Cumulative interest is how much interest you will pay over the life of your loan. That’s what we calculated in the example above.

- Total interest paid is how much interest you have paid so far.

The difference between cumulative interest and total interest paid is subtle but important. Understanding how each one works can help you choose a more cost-effective boat loan.

How is the loan term for a boat loan calculated?

While most boat loans come with 10- to 20-year terms, each lender sets its own range of loan terms. Which of your lender’s term lengths are available to you depends on your loan amount and credit score.

As you shop for a boat loan, resist the urge to select the loan with the longest term, especially if you’re buying an older boat. Long-term loans have their purpose, but they aren’t always the best idea.

Take our hypothetical $25,000 boat loan, for example. When we assumed a 10-year term, our payments were around $290. If we opt for a 15-year term instead, our payments will drop to roughly $225.

This looks good at the outset, right? But how does our longer term impact our interest expense and borrowing cost?

While our monthly payments dropped, our cumulative interest went up about $5,600. In this case, the longer repayment period was more detrimental than the 9% interest rate from the previous section.

How is the amortization for a boat loan calculated?

Amortization refers to paying down a loan in regular installments. Amortization schedules refer to how each of those installments is split between principal and interest. To formulate your amortization schedule, follow these steps:

- Multiply your loan amount by your interest rate.

- Divide by 12.

- Subtract this number from your monthly payment amount.

The result is how much of your monthly payment goes toward the principal. While it’s helpful to understand the underlying math, calculating amortization by hand each month probably isn’t on your to-do list. Instead, your lender should provide you with an amortization table.

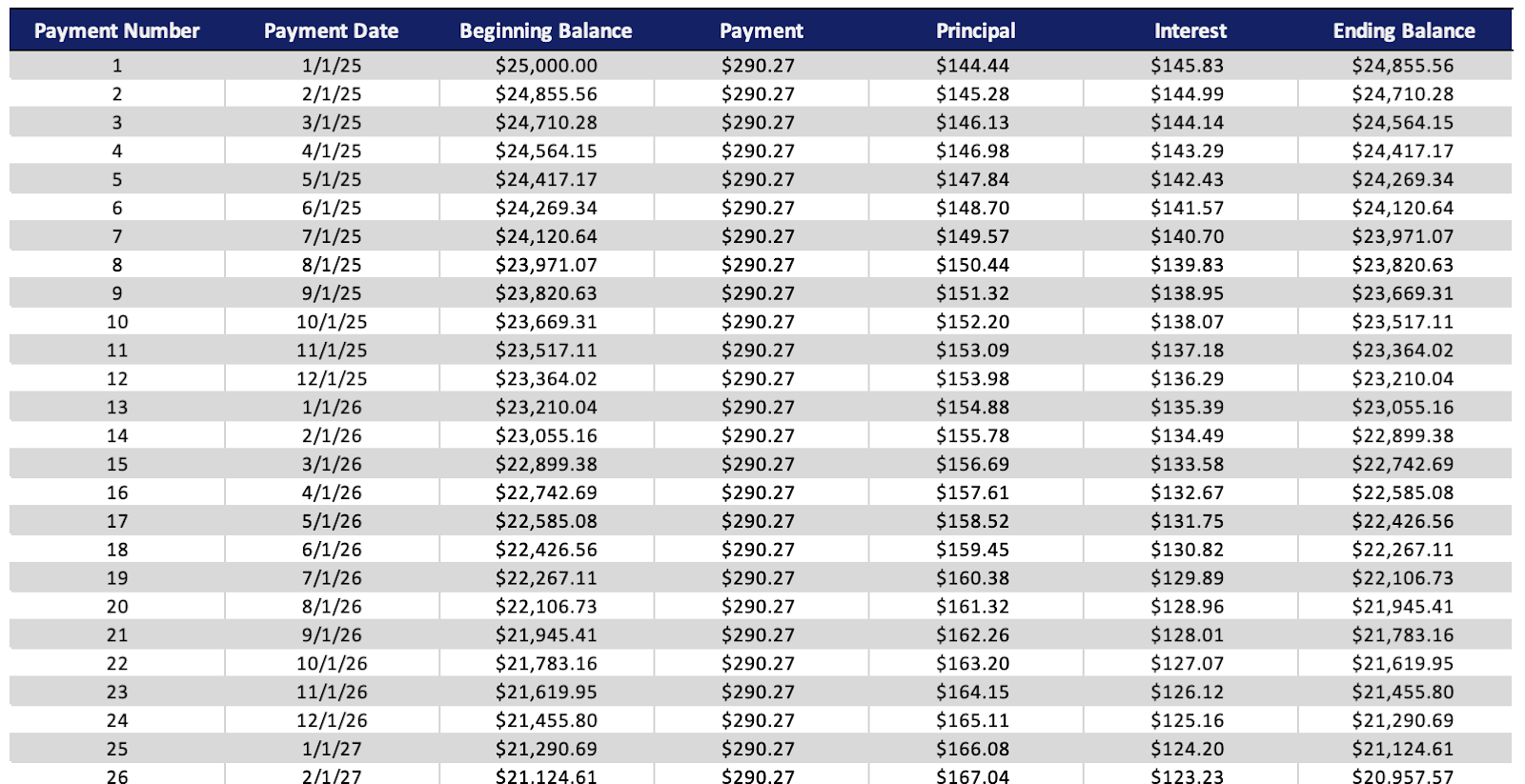

For our 10-year, $25,000 boat loan at 7% interest, the amortization table might look something like this:

In this case, your first several payments are nearly a 50-50 split between principal and interest. As you progress through your loan term, a larger portion of your payments goes toward the principal.

For easier analysis, here’s a visual representation of how this allocation looks:

Notice how many years it takes for our loan payments to make a significant dent in our principal. In other words, getting ahead of that amortization schedule is the best way to save money on your loan.

The best way to do this is to make extra, principal-only payments. Earmarking excess funds for principal will shave down your remaining balance, preventing interest from accumulating and getting you closer to loan payoff.

How do taxes and fees factor into boat loan payment calculations?

Sales tax and upfront fees are typically rolled into your loan amount. This increases your principal, which, in turn, increases your monthly payment.

Other fees, like late charges, are assessed on a case-by-case basis. These fees may be tacked onto your next payment, and your lender may charge interest on any accrued fees.

To minimize your boat loan cost, look for lenders that charge few fees, if any. Consider enrolling in autopay, too, to avoid paying late fees.

How to calculate the ideal boat loan

In our opinion, the ideal boat loan meets these criteria:

- The interest rate is no higher than 10% (and hopefully far less).

- The boat loan will be paid in full within 10 to 15 years.

- Your boat loan doesn’t put your debt-to-income ratio over 35%.

- Monthly payments are comfortably affordable.

When we say “comfortably affordable,” we mean you can cover your boat loan, boat expenses, regular bills, and savings goals with leftover money. If getting a boat loan requires dipping into your emergency fund or pausing your retirement contributions, it’s not worth it.

That said, consider why you’re buying a boat. Are you getting a liveaboard that’ll replace your mortgage? Do you have a commercial fishing license and can use your boat to generate income? It’s easier to justify taking on the added debt in those circumstances.

Beyond the financials, weigh how the new boat will impact your well-being. You can’t put a price on summer sunrises on the lake with the kids. If you’ll get enough usage out of your boat to warrant the cost—and you have a solid payoff plan in place—the boat loan may be well worth it.

About our contributors

-

Written by Christy Rakoczy

Written by Christy RakoczyChristy Rakoczy has been a personal finance and legal writer since 2008. She has a Juris Doctor degree from UCLA School of Law and was a college instructor before she began writing for the web.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.