If you’re paying down an $80,000 student loan balance, you’re not alone. In fact, according to the U.S. Department of Education, 5 million borrowers carry $80,000 or more in student loan debt.

Chances are, you and many of those borrowers are eager to start chipping away at that balance—and the good news is, it might be more manageable than you think. In this guide, we’ll walk you through practical strategies for tackling your student loan debt when you owe at least $80K, and what you can expect along the way.

🎓 In the News: On June 24, 2025, a report published by TransUnion showed that nearly 6 million student loan borrowers are newly delinquent with around 2 million facing wage garnishment only months after payments resumed.

Read more: What to Do If Student Loans Are in Collections: FAQ About Repayment, Settlement and Bankruptcy

Already thinking about refinancing as part of your plan? It can be a smart move to reduce your interest rate or accelerate repayment. You can check out our top-rated student loan refinance lenders to explore your options. If you’re not quite there yet, don’t worry—we’ll cover all your repayment choices step by step.

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

|

Best for Comparison Shopping |

|

|

Best Online Lender |

|

|

|

Best Personalized Support |

|

|

Best Skip-a-Payment Benefit |

|

Table of Contents

Is $80,000 in student loans a lot?

In short: it’s a significant amount, but it’s not uncommon—especially for graduate students or borrowers who attended higher-cost institutions. An $80,000 balance puts you well above the national average, which sits around $41,000 per borrower. But compared to six-figure balances that many medical, law, or dental students take on, it’s far from the highest.

The good news? With a steady income, a smart repayment plan, and a bit of flexibility, paying off $80,000 in student loans is very doable. Whether you’re just getting started or looking to speed up the process, the steps that follow can help you build a payoff plan that fits your goals.

How to pay off $80K in student loans in 6 steps

We’ve broken down the student loan payoff process into six steps:

- Review your loan breakdown.

- Make a budget.

- Explore repayment and forgiveness options.

- Consider consolidating or refinancing.

- Determine your payment schedule.

- Incorporate side quests.

As we present each phase, know we’re taking a realistic approach. Most of us don’t have $80,000 lying around, and most of us are financially obligated to more than just our loans.

To that end, our six-step solution is both sustainable and straightforward. No matter your situation, you can adapt this plan to work for your timeline and priorities. Now, let’s dive into the details.

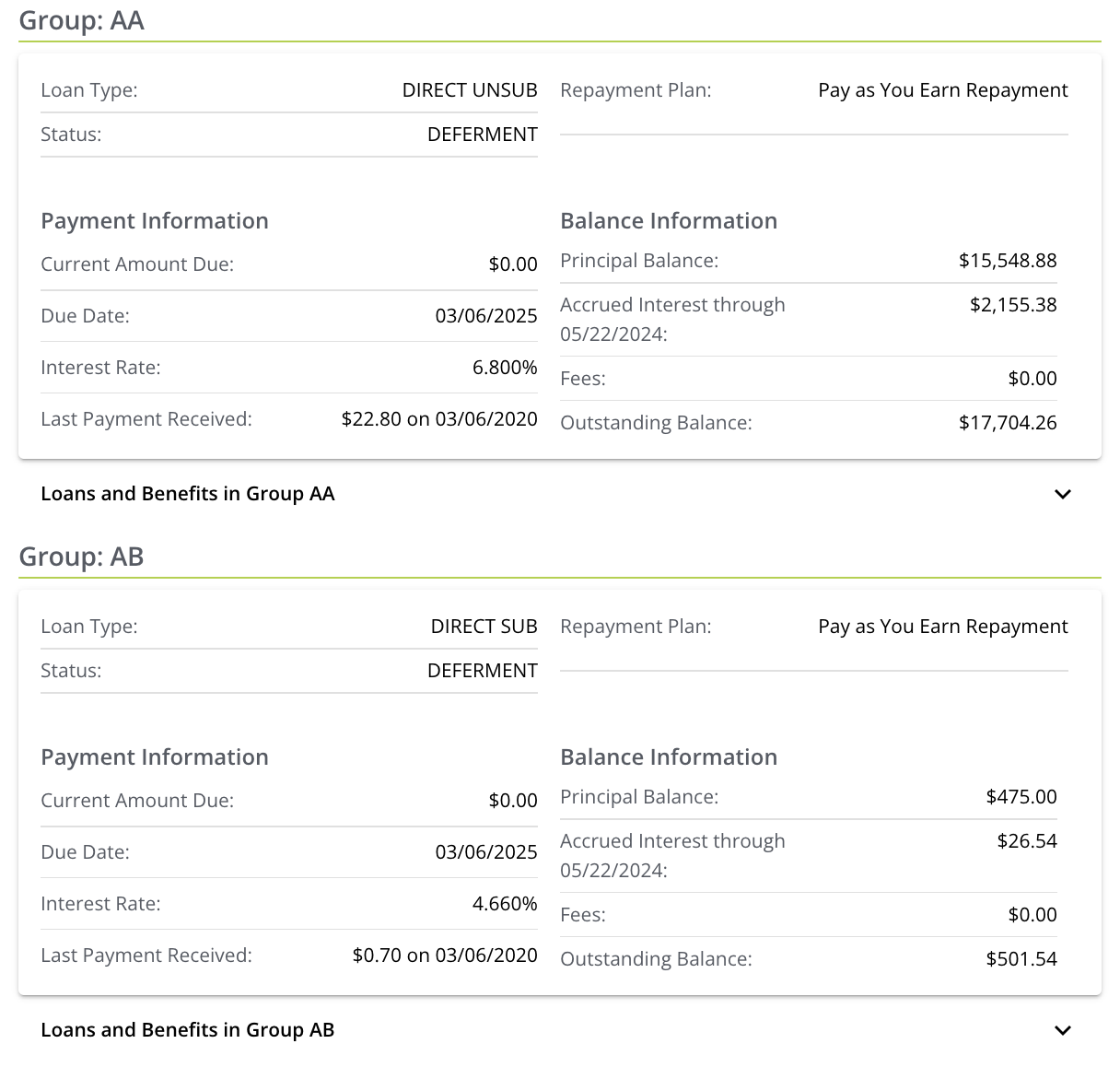

🔍 Step 1: Review your loan breakdown

While student loans are delivered to your school in one lump sum each term, federal loan servicers may separate them into multiple loan groups, as you see in the image below.

These smaller loans make up your overall loan balance, each with its own interest rate. Log in to your loan servicer’s website to see your loan breakdown. If you have private loans, you’ll want to check those balances and rates, too.

Aside from giving you greater insight into your student debt, knowing what comprises your total loan balance is helpful for three key reasons:

- You’ll see which loans generate the most interest.

- You’ll see how your loan payments are applied throughout your loan groups.

- You can use your loan groups as goalposts.

Achieving several milestones throughout your loan payoff journey—instead of waiting to celebrate until you’re debt-free—can increase your motivation. And if you prioritize loan groups with higher interest rates, you’ll save money and pay down your loans more quickly.

📊 Step 2: Make a budget

Along with learning what makes up your education debt, you need to calculate how much you can afford to pay toward your loans.

There are several budgeting styles to choose from, but each one shares a similar core process:

- Add up your monthly take-home pay.

- List your necessary expenses.

- Subtract your expenses from your income.

At this stage, you could track your spending to see where your leftover money goes each month. Alternatively, you could make the executive decision to allocate how you’ll spend that money going forward.

As much as possible, try to balance budgeting for student loans with building your emergency fund, paying down other debt, and enjoying your earnings. For example, if you have $600 to spare each month, you might divvy it up like this:

| Leftover earnings | $600 |

| Student loan payments | $200 |

| Savings | $125 |

| Investments | $125 |

| Fun money | $150 |

Be sure to base your budget around your lifestyle and goals. Revisit your budget once a quarter or after major financial changes, and tweak as needed.

🧾 Step 3: Explore repayment and forgiveness options

Once you know how much you can devote to your debt payoff, consider how student loan repayment plans could alter your strategy.

For private student loans, contact your lender to see if it offers modified repayment schedules. If you have federal loans, you may be eligible for one of these income-driven repayment (IDR) plans:

- Saving on a Valuable Education (SAVE)

- Pay As You Earn (PAYE)

- Income-Based Repayment (IBR)

- Income-Contingent Repayment (ICR)

You may also qualify to make graduated payments or to extend your federal loan term for 25 years instead of 10.

Longer loan terms can lower your monthly payments, but you might owe more over time. Use our student loan payment calculator to see how extended repayment can affect your total borrowing cost.

Work with your loan servicer to determine which of these plans is best for you. Be sure to ask how much of your balance may be forgiven at the end of your repayment term and factor that into your payoff strategy.

🔄 Step 4: Consider consolidating or refinancing

You’re almost ready to launch your $80,000 debt payoff plan. Before you do, it’s worth evaluating whether student loan consolidation or refinancing makes sense. Both options let you combine multiple loans into one payment, but each one can impact you in different ways:

| Consolidation | Refinancing | |

| Eligible loans | Federal | Federal, private |

| Credit check? | ✖️ | ✔️ |

| Rates based on… | Avg. rate of your federal loans | Your credit |

| Advantage | Retain federal loan benefits | Could get lower interest rate |

| Disadvantage | May not reduce interest rate or borrowing cost | Lose federal loan benefits |

Consolidating federal loans might be a wise move if interest rates vary widely between your loan groups. Lowering interest rates on some of your loans could help accelerate your payoff. The caveat, however, is that you run the risk of raising the rates on your other loans.

If you borrowed private loans at high interest rates, refinancing could usher in an opportunity for significant savings. Many of the best student loan refinance companies require credit scores above 650, so consider that as you weigh your choices.

📅 Step 5: Determine your payment schedule

You’ve researched your student loans, your finances, and your routes to repayment. Now, you can put all of that together into a full-fledged student loan payoff strategy. The penultimate step involves building out a payment schedule that kicks your loan reduction into high gear.

You must make at least one payment a month, but you are not limited to that amount. You also don’t have to pay it all at once.

Say, for example, that your interest rate is 5.50%, and you aim to pay off your loans in 10 years. If you divide your one-and-done monthly installment into biweekly payments, here’s how you’ll impact your $80,000 loan balance.

$80,000 student loan monthly payment vs. biweekly

| Frequency | Monthly | Biweekly |

| Payment amount | $868 | $434 |

| Total interest paid | $24,185 | $21,489 |

| Total principal + interest | $104,185 | $101,489 |

| Time to payoff | 10 years | 9 years |

By splitting your payments, you’ll save nearly $2,700 in interest. You’ll also pay off your loans one year sooner. Feeling inspired? Compound these results by paying toward your student loans every week.

💡 Step 6: Incorporate side quests

Alongside your established payoff plan, working toward complementary financial milestones can help you hit your student loan target faster. It’ll also keep you on track with other money matters.

The key is to find ways to augment your income while restructuring or reducing your expenses. This approach frees up funds you can funnel toward your student loan payments. Here are a few ideas to get you started:

- Negotiate a hybrid work arrangement.

- Apply for a better-paying job.

- Downsize to a lower-cost apartment.

- Sell unneeded clothes, furniture, or textbooks.

- Launch the side hustle you’ve been putting off.

- Pay down high-interest credit cards.

That last one may seem like a competing priority, but carrying debts with higher interest rates than your student loans only hinders your repayment progress. To that point, get creative and be strategic with your side quests. The best path forward isn’t always the most obvious.

Carrying $80,000 in debt increases your DTI ratio and can preclude one from being approved for future loans such as a mortgage or auto loan. Paying down the debt as agreed and potentially expediting the pay-off if your budget and time allow will enable you to be approved for mortgages or auto loans you need.

How long does it take to pay off $80,000 in student loans?

How long it will take to repay your loans depends on several factors, including the repayment plan you choose and the size of your monthly payment.

Here’s what your monthly payments could look like for an $80,000 student loan with a 6% interest rate and different repayment terms:

| Repayment term | Monthly payments | Total interest paid |

| 5 years | $1,546 | $12,797 |

| 10 years | $888 | $26,580 |

| 15 years | $675 | $41,587 |

| 20 years | $572 | $57,554 |

| 25 years | $515 | $74,632 |

As your income increases, making extra payments on a 10-year, $80,000 student loan at 4.75% can speed up your loan repayment. The table below shows how a borrower might increase their payments by $100 a month over five years:

| Repayment year | Monthly payment |

| 1 | $838 |

| 2 | $938 |

| 3 | $1,038 |

| 4 | $1,138 |

| 5 | $1,238 |

After five years, you would save $7,022 in interest and repay your loans 34 months sooner than if you just made the minimum payment of $838 the entire time.

How should you prioritize paying off $80,000 in student loans? It depends on your financial condition. Do you have higher-interest debt? If so, pay this first and then make additional payments toward the student loan. If you can’t pay off the student loan yet, it may be in your best interest to shop for refinancing to a lower interest rate or consolidate debt into one manageable payment.

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.