Looking to lower your student loan interest rate? You’re in the right place.

Even a small rate drop could save you thousands. For example, lowering a $30,000 loan from 7% to 5% could reduce your monthly payment by about $30—and save you more than $3,600 in interest over 10 years.

Whether you’re managing federal or private loans, here are seven proven ways to lower your rate and keep more money in your pocket.

Table of Contents

1. Sign up for autopay

- Best for: Most borrowers with federal or private loans

- How hard it is to get: Easy

- Loan types: Federal, private

SoFi®, our choice for the best online lender, offers a 0.25% interest rate reduction if you enroll in automatic paymentsⓘ. This discount is offered for most federal loans and many private loans. Contact your servicer or log into your loan account to activate autopay.

2. Look for loyalty or relationship discounts

- Best for: Borrowers with multiple products at one bank or lender

- How hard it is to get: Easy

- Loan types: Private

For example, Citizens Bank provides a generous 0.25% loyalty discount in addition to its 0.25% autopay discount.

3. Negotiate with your lender

- Best for: Private loan borrowers who’ve found a better rate elsewhere

- How hard it is to get: Moderately hard

- Loan types: Private

If you have a strong payment history or a lower quote from another lender, contact your current lender and ask whether it will match or beat the offer. Some lenders will negotiate to keep your business, especially if you’re considering refinancing.

4. Apply with a cosigner

- Best for: Borrowers with limited credit or income

- How hard it is to get: Moderately hard

- Loan types: Private

Adding a creditworthy cosigner through refinancing could help you qualify for a lower rate. Some lenders will consider cosigner applications even after the loan is already issued—though you’ll need to refinance to benefit from the change.

EDvestinU offers student loan refinancing and will allow you to request to remove a cosigner after 24 consecutive on-time monthly payments—the shortest window we found in our research on refinance lenders.

5. Improve your credit score

- Best for: Borrowers with fair-to-good credit looking to refinance

- How hard it is to get: Moderately hard

- Loan types: Private

A higher credit score can unlock lower refinance rates. To boost your score: Pay bills on time, reduce credit card debt, and check your credit reports for errors. Even a small jump to the next credit tier can make a noticeable rate difference.

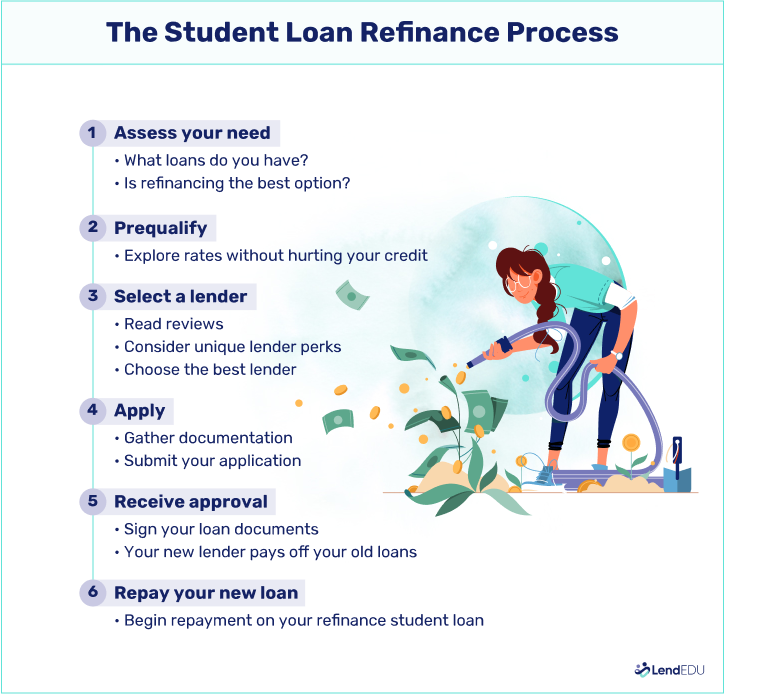

6. Refinance to a lower rate

- Best for: Borrowers with strong credit and stable income

- How hard it is to get: Difficult

- Loan types: Private, federal (if willing to give up protections)

Refinancing means replacing your loan with a new one at a better rate. It can save you money or reduce your monthly payment—but refinancing federal loans means losing access to benefits like income-driven repayment and forgiveness programs.

If you’re considering refinancing, start with a marketplace. Our favorite is Credible. It’s our pick for the best comparison shopping because it lets you check rates from multiple top lenders in one place—without affecting your credit score. You’ll get a clearer picture of what rates and terms you might qualify for, making it easier to find the best deal.

7. Choose a shorter repayment term through refinancing

- Best for: Borrowers who can afford a higher monthly payment

- How hard it is to get: Difficult

- Loan types: Private, federal (if refinanced)

Lenders often offer lower rates for shorter terms. If you’re refinancing, choosing a five- or seven-year term can secure a better rate and reduce interest paid overall. Just make sure the higher monthly payment fits your budget.

ELFI offers term lengths of five, seven, 10, 15, or 20 years.

When my clients want to lower their student loan interest rates, we begin by assessing their financial situation, including their credit report and debt-to-income ratio (DTI), to determine whether they can qualify for refinancing on their own.

If they are not in a position to secure a lower interest rate independently but have a trusted and financially capable friend or family member willing to cosign, I may recommend that option.

In either case, if their credit report or DTI is not in good standing, I will work with them to develop a realistic plan for improvement. If refinancing must be postponed until their credit profile improves, that will be the path forward.

What doesn’t lower your student loan interest rate?

Not all loan strategies reduce your rate. Here are a few common moves that won’t lower what you pay in interest:

- Federal loan consolidation: This combines multiple loans into one but uses a weighted average of your current rates—rounded up. It may simplify payments but won’t save you interest.

- Making extra payments: Paying more each month helps you pay off your loan faster, but it doesn’t reduce your interest rate.

- Income-driven repayment (IDR): These plans lower your monthly payment based on income, not your interest rate. You might pay more in interest over time.

- Loan deferment or forbearance: These options pause payments but allow interest to continue accruing, often increasing the overall cost.

Want to actually lower your rate? Stick with tactics like refinancing, autopay discounts, or applying with a cosigner.

About our contributors

-

Written by Rebecca Safier

Written by Rebecca SafierRebecca Safier is a personal finance writer with years of experience writing about student loans, personal loans, budgeting, and related topics. She is certified as a student loan counselor through the National Association of Certified Credit Counselors.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.