When you close out a HELOC, you lose access to the credit line. Lenders may close it out after the repayment term ends once the balance is paid or convert the remaining balance into a new loan. Borrowers can also request cancellation under specific conditions.

Regardless of who initiates it, a HELOC close-out letter is required to confirm cancellation. This letter serves as official acknowledgment that the credit line is closed. Whether the lender or borrower sends the letter depends on who initiates the process. Here’s what you need to know about closing out a HELOC and the required documentation.

Table of Contents

Why might I send a HELOC close-out letter?

You might need to send a HELOC close-out letter to your lender in several scenarios, such as if you:

- Are selling the home. This situation results in an automatic closeout of your HELOC—after all, your home is being used as collateral. You may need to prove the HELOC is closed out and you no longer have access to your credit line as a condition of finalizing your home sale.

- Want to get a new HELOC or home equity loan. If you’re applying for a new HELOC or a home equity loan, the lender may require you to close out an existing line of credit first. You might need a HELOC close-out letter to document the cancellation.

- Don’t need your HELOC. You might end a HELOC early if you no longer need access to your credit line. In that case, you could ask the lender to close it out.

- Want to avoid fees. Lenders may charge monthly or annual fees to maintain a home equity line of credit. Your lender may also charge you an inactivity fee if you don’t use your HELOC. If you’re not using your HELOC and want to avoid those fees, you can ask the lender to end it.

- Need to reduce your debt-to-income (DTI) ratio. You may need to close out your HELOC to achieve an adequate DTI to obtain another loan.

- Want to reduce spending. Similar to cutting up credit cards, canceling a HELOC can help you avoid unnecessary spending.

When can I send my lender a HELOC close-out letter?

If you confirm your lender will allow you to terminate your HELOC early, you should be able to send a close-out letter any time during the draw period or repayment period. The draw period for a HELOC is the window in which you can withdraw money. You’ll pay back what you borrow during the repayment period.

A different time frame applies if you open a HELOC and then change your mind about using it. In that case, you must submit the request to cancel to your lender in writing within three days to cancel a HELOC and get a refund on the money you paid to the lender.

The lender has 20 days after receiving your request to return your money and release the interest in your home as collateral for the HELOC. You can keep any money you receive from the lender until it releases your home as collateral and refunds the fees.

However, you likely won’t have received your HELOC funds yet from the lender during this time. Even Figure, which has one of the fastest funding HELOCs, releases funds within five days of approval, once the three days have lapsed.

What to know about the three-day rule

The three-day rule allows you to cancel a HELOC in writing until midnight of the third business day after it’s opened. You can do this for any reason as long as the home that secures the HELOC is your primary residence. If you take out a HELOC on a vacation home or second home, the three-day rule may not apply.

Reasons might include: you find better terms with another lender, decide a home equity loan makes more sense, or you change your mind altogether on taking equity out of your home

Day one of the three-day rule begins the business day after the following three conditions are met:

- You sign the loan at closing.

- The lender provides you with a Truth in Lending disclosure form that includes details about your HELOC agreement.

- You receive two copies of a Truth in Lending notice explaining your right to cancel.

Saturdays, but not Sundays, are included when calculating the three business days. Public holidays are excluded.

For example: Say you close on your HELOC on a Friday afternoon, at which time you sign the loan documents and receive all the necessary disclosures. In this case, the end of the third business day would be Tuesday, so you have until midnight on Tuesday to notify the lender you want to cancel.

However, if your lender provides the necessary disclosures on Monday, that bumps your cancellation deadline to midnight on Thursday. Keeping track of when you receive each disclosure can help you avoid missing your cancellation window.

If your lender fails to provide the disclosure—or it did, but the disclosures are incorrect—you may have up to three years to cancel your HELOC. The Consumer Financial Protection Bureau advises consumers to consult an attorney if they believe they may still be eligible for cancellation under those circumstances.

Does the lender return the fees I paid if I cancel a HELOC?

If you cancel your HELOC within the three-day window, the lender must return all the fees you paid. These include:

- Finance charges

- Application fees

- Appraisal fees

- Title search fees

If you close out a HELOC after the three-day window, you are not refunded the fees you paid when you originally opened it. Additionally, your lender may charge a cancellation fee if you decide to terminate the line of credit before the end of the repayment term. All fees should be outlined in your HELOC agreement.

Can I send a HELOC close-out letter if I owe a balance?

Yes, you can request to close out a HELOC with a balance in place. Maybe you plan to use part of the proceeds from the sale of your home to pay off your HELOC, but you need to close out the HELOC to wrap up the sale.

In that case, you must send your lender a HELOC close-out letter for the sale to go through because you must end the HELOC after your home is sold.

Requesting cancellation of a HELOC doesn’t release you from the obligation to repay an outstanding balance, however. Depending on how the lender formats its HELOC close-out letter template, specific wording may detail your responsibility for any remaining balance.

Can my lender send me a HELOC close-out letter?

Generally, a lender can’t cancel a HELOC until the balance reaches $0 at the end of the repayment term. If you pay off your HELOC, your lender could send a letter acknowledging the loan has been paid in full.

However, Regulation Z of the Truth in Lending Act allows lenders to terminate a HELOC if:

- You misrepresented yourself or committed fraud in obtaining a line of credit.

- You fail to meet the repayment terms of your agreement.

- Action or inaction on your part harms the lender’s security interest in the home.

Your lender may also reduce your credit limit or freeze your HELOC for reasons including:

- A significant drop in the value of your home.

- A drastic change in your credit rating.

- It believes you won’t be able to make your payments.

- Failing to meet payment terms set in your agreement.

The lender must give you three business days’ written notice before freezing or reducing your HELOC. The notice will explain the reason.

If your lender sends a letter stating it’s reducing or freezing your HELOC limit, you could ask it to reinstate your line of credit if your situation changes. If the lender freezes your HELOC because your home value dropped, you might be able to regain access after your equity increases.

What is the difference between canceling and freezing a HELOC?

When a HELOC is canceled, it’s terminated. A lender may cancel a HELOC under the terms outlined in the Truth in Lending Act. You could also cancel the HELOC yourself by paying it off. (Your lender might not automatically cancel the account if you pay it off during the draw period, so if that’s your intention, we recommend contacting your lender.)

The table below shows situations in which your HELOC could be frozen vs. canceled.

| Situation | Cancel or freeze? |

| Evidence of fraud or misrepresentation on your part in obtaining the line of credit | Cancel |

| You don’t meet payment obligations | Cancel |

| You aren’t using the funds in a HELOC during the draw period | Cancel |

| Your home’s value significantly decreases | Freeze |

| A shift in your financial situation puts into question your ability to repay | Freeze |

| Your credit score plunges | Freeze |

If your HELOC is frozen, you might be able to unfreeze it. You can ask your lender to unlock your credit line if the reasons for the freeze no longer apply.

For example, suppose your lender froze your HELOC because your home value fell. If the value rises again, you might regain access by sharing a new appraisal with your lender.

The lender might also reinstate your HELOC without requiring you to request it if it determines the situation that prompted the freeze has changed.

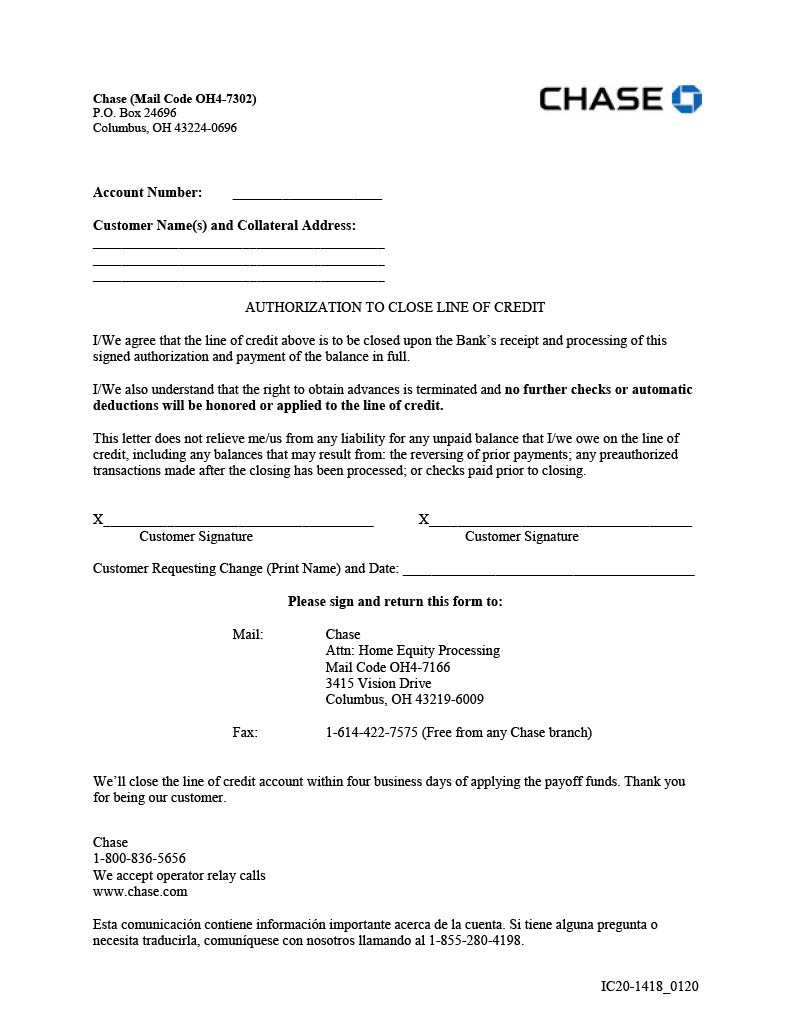

What does a HELOC close-out letter look like?

Here’s a sample HELOC close-out letter from Chase Bank:

Source: Chase Bank

Your lender might offer a HELOC close-out letter sample document or standardized form you can submit. It may be available on the lender’s website or via email by request.

Depending on your bank or lender, you may be able to return it by mail, fax, or in person at a branch.

A HELOC close-out form can vary by lender. You can expect to provide the following:

- HELOC loan number or account number

- Address of the property used as collateral for the credit line

- Your name and signature

- The date of your request

The letter should specify you’re requesting to end your HELOC and acknowledge you’ll no longer have access to your credit line. It should also state you assume responsibility for any remaining balance owed.

How do I know the lender received my HELOC close-out letter?

Once you request to close out a HELOC, your lender should send confirmation it received the request. It should send a separate notice it removed the lien on the property that secured the loan if you’re canceling a HELOC with a $0 balance.

It’s wise to follow up with the lender to ensure it received your letter. Maintenance fees could continue to accrue as long as the account remains open, which could mean a surprise bill if you assumed the account was closed out.

If you’re worried about your HELOC close-out letter getting lost in the mail, you could send it via certified mail with tracking or fax it. We also recommend making a copy of the letter for your records.

Check out our guide if you want to understand more about how HELOC repayment works.

FAQ

What should I do if my lender cancels my HELOC?

If a lender closes out a HELOC, it provides a notice containing details of the action. You should immediately review the document for accuracy. If you find inaccuracies, notify the financial institution as soon as possible, and maintain supporting documents in case you need them later.

How does canceling a HELOC affect my credit score?

If a lender cancels your HELOC, it could damage your credit score. It may lower the amount of credit available to you, affecting your credit utilization ratio. Your credit score could also take a hit if your HELOC is your only form of revolving credit. However, paying all debts on time and maintaining a low balance will help in maintaining a healthy credit score.

Can I reopen a closed out HELOC, or do I need to apply for a new one?

Reopening a closed out HELOC is not typically possible. Once it’s canceled, whether by you or the lender, you must apply for a new HELOC. The process would be the same as the initial application, involving credit checks, home appraisals, and a comprehensive financial review.

What happens if an error occurs in the close-out process?

If an error occurs, such as an incorrect balance or missing information, notify your lender right away. You should provide all necessary documents that refute the error and request your lender for a written acknowledgment of the issue. It’s essential to stay vigilant and responsive to protect your rights and minimize potential financial impacts.

About our contributors

-

Written by Rebecca Lake, CEPF®

Written by Rebecca Lake, CEPF®Rebecca Lake is a certified educator in personal finance (CEPF®) and freelance writer specializing in finance.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.