A home equity line of credit (HELOC) offers flexible access to your home’s equity, but understanding the details is crucial before you commit. The HELOC early disclosure form is your first glimpse into the terms, rates, fees, and potential risks of your line of credit. It’s more than just fine print—it’s a road map to how your HELOC works and what could happen if you don’t meet its requirements.

In this guide, we’ll break down why the early disclosure is essential, what it includes, and how to use it to make informed decisions about your financial future. Whether you’re borrowing for renovations, debt consolidation, or other expenses, this document is crucial to ensuring your HELOC aligns with your goals.

Advertisement

While many HELOC lenders advertise minimum credit scores around 640, approvals typically go to borrowers with scores closer to 720 or higher. If your credit is lower and you need fast funding, home equity agreements or other alternatives may be easier to qualify for.

Why is a HELOC early disclosure important?

A HELOC early disclosure is the best way to learn about the general terms and conditions of a HELOC before finalizing your application. It provides an overview of how the product works and what to expect, including:

- What can happen to your home if you don’t repay your HELOC as agreed

- Under what conditions your lender can terminate or reduce your credit line

- General guidelines for the draw period length and repayment terms

- How a variable rate may affect your payments

- Typical fees associated with a HELOC

HELOC early disclosures also outline common requirements, such as maintaining property insurance or minimum draw amounts. While this document gives a helpful overview, it may not include your specific interest rate or credit line amount.

Review your early disclosure to understand the potential risks and costs of a HELOC. Use it to make an informed decision about whether this product suits your financial needs.

Read More: What is a HELOC, and How Does It Work?

Is a HELOC early disclosure the same as a HELOC disclosure?

No, a HELOC early disclosure is not the same as a HELOC disclosure provided at account opening. These two documents serve different purposes and are delivered at different stages of the borrowing process.

- You’ll get your HELOC early disclosure, often referred to as the application disclosure, when you apply for a HELOC. It outlines general terms, costs, and risks associated with the HELOC product. Its purpose is to help you understand the features and decide whether to proceed with the application. Federal regulations, such as Regulation Z, require lenders to provide this disclosure at the time of application.

- In contrast, a HELOC disclosure provided at account opening includes specific details about your approved HELOC agreement. This document will list your actual interest rate, credit line amount, fees, repayment schedule, and other personalized terms. It ensures you have a full understanding of your agreement before accessing funds.

Both disclosures aim to inform borrowers, but the early disclosure is a preliminary overview, and the account opening disclosure is a finalized agreement tailored to your HELOC.

What does a HELOC early disclosure look like?

You can expect to get your HELOC early disclosure form after submitting your initial application. Even if you applied online or by phone, the document is often sent by mail or digitally for review.

The early disclosure is usually several pages long and provides an overview of the terms and features of a HELOC. While it won’t include details specific to your loan, such as your interest rate or approved credit line, it gives insight into how the product works. Sections are labeled in bold type or headings, making it easier to find the information you’re looking for.

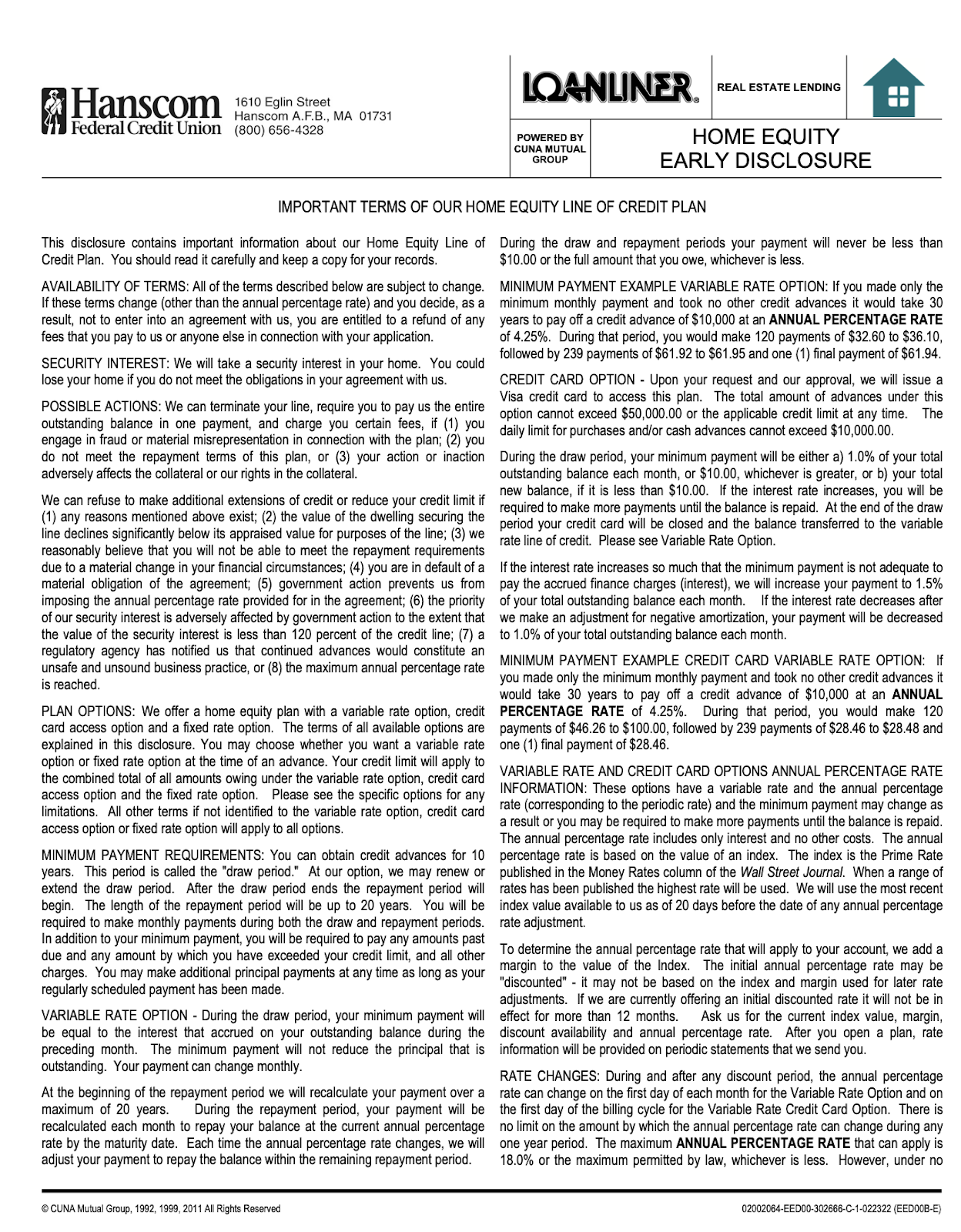

Below is an image of a sample early disclosure form from Hanscom Federal Credit Union (HFCU) in Massachusetts. Note that the format and content may vary depending on your lender.

Your early disclosure form may be formatted differently depending on your lender, but the information should be similar.

HELOC early disclosure requirements

The HELOC early disclosure form outlines general product terms and important considerations to help borrowers understand the risks and costs of a HELOC.

Common sections include:

- Availability of terms: Explains that terms may change before final approval. Borrowers may cancel the agreement if changes occur.

- Security interest: Clarifies the lender’s right to repossess your home if you fail to meet repayment terms.

- Variable-rate feature: Describes how variable interest rates are calculated, typically based on a benchmark (e.g., the prime rate), and includes examples of rate fluctuations.

- Fixed-rate feature (if applicable): Outlines whether a fixed-rate option is available and how it may apply to the draw and repayment periods.

- Fees and charges: Lists common fees, including annual, processing, and late fees. Specific amounts may not be finalized until your HELOC is approved.

- Maximum rate and payment example: Provides hypothetical scenarios of how high your interest rate and payment could go, helping you assess potential risks.

- Historical example: Shows how rates have fluctuated over time, giving you an idea of what to expect during economic shifts.

These sections aim to educate borrowers on the risks and costs of HELOCs before they finalize their agreement. For borrower-specific terms, consult the final HELOC disclosure provided at closing.

Not sure you want to borrow a HELOC because of the variable rate? Two of our team’s highest-rated HELOC lenders, Figure and Aven, offer 100% fixed-rate HELOCs.

Can any terms in the HELOC early disclosure change?

Yes. The HELOC early disclosure highlights that certain terms may change before you finalize your agreement. For instance, the lender may adjust the variable interest rate based on the current market conditions or make other modifications outlined in the “Availability of Terms” section.

Be sure to look for language explaining which factors could change before finalizing the HELOC. If you have concerns, contact your lender to confirm whether adjustments are likely and how they might influence your loan terms. Remember, the final HELOC disclosure, provided at closing, will include the exact terms of your agreement.

What to look out for in a HELOC early disclosure

Review your HELOC early disclosure to understand the product’s general risks and features. Pay special attention to the following:

- Interest rate details: If your HELOC has a variable rate, review how it’s calculated and whether the lender caps how high it can rise. This section will also include hypothetical examples of maximum payments.

- Fee structure: Check for any unclear fees, such as annual or processing fees, and confirm whether these are refundable if you decide not to proceed with the loan.

- • Security interest: Make sure you understand the lender’s right to repossess your home if you fail to meet repayment terms.

If any sections seem unclear or raise concerns, reach out to your lender for clarification. Keep in mind that the early disclosure provides general terms, and borrower-specific details will be available in the final disclosure once your HELOC is approved.

Read More: How to Apply for a HELOC in 5 Steps

About our contributors

-

Written by Zina Kumok

Written by Zina KumokZina Kumok is a personal finance writer dedicated to explaining complex financial topics so real people can understand them. As a former newspaper reporter, she has covered everything from murder trials to the Final Four.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.