The financial impact of the Coronavirus pandemic has been devastating for most Americans, and the federal government has taken a number of actions to soften the blow.

Measures to protect student loan borrowers have been implemented. For example, interest rates on federal student loans have been set to 0% until September 30, 2020, and federal borrowers can also skip payments until that date.

A new LendEDU survey of 1,000 adult Americans currently repaying their federal student loan debt found that these protective actions came just in time as many respondents were not sure if they would have been able to make even their next student loan payment.

And for borrowers that have lost their jobs in the wake of this global pandemic, as many Americans have, the measures may have saved them from financial ruin.

Click here to jump to the full survey results

If you would like to see a specific breakdown of the data other than those provided (ex. state-by-state, gender, age, employment status), or a full survey-to-survey comparison, please email me at [email protected].

Observations & Analysis

All data is based on a survey of 1,000 adult Americans currently repaying their federal student loan debt that was commissioned by LendEDU and conducted by survey platform Pollfish. The survey was conducted on April 20, 2020. For some questions, the answer percentages may not add up to 100% exactly due to rounding.

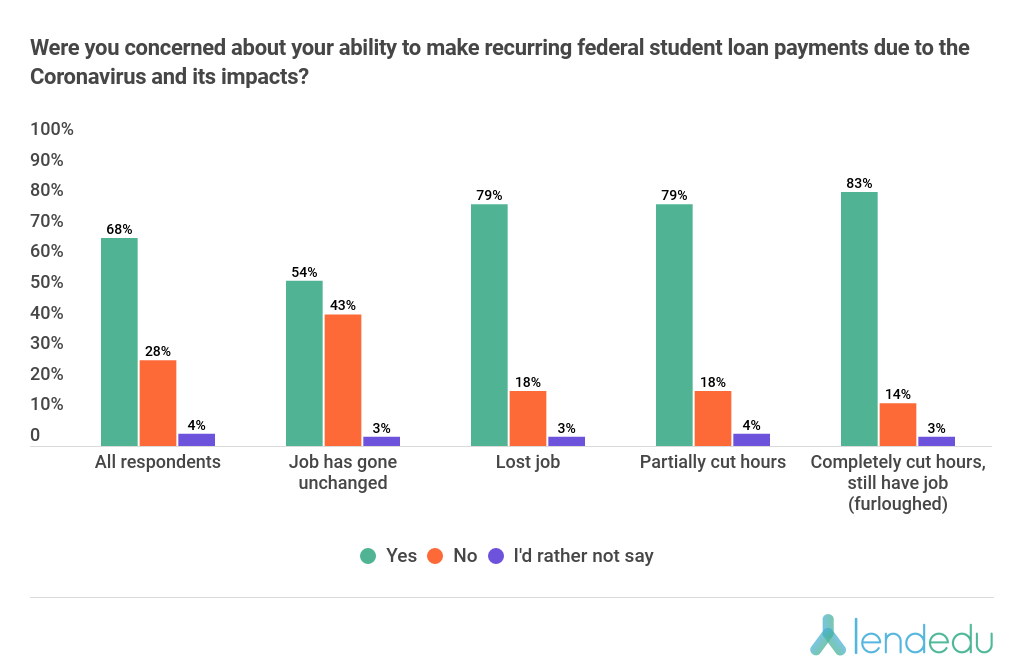

Many Borrowers Skeptical Of Their Ability to Make Student Loan Payments Had Government Relief Not Come

Including 68% of Federal Student Loan Borrowers

From March 13, 2020 through September 30, 2020, federal student loan borrowers will be in a grace period where monthly payments are not required and interest will be frozen at 0%.

The results from our survey indicated this policy change likely saved some folks from financial peril as the COVID-19 pandemic has forced business shutdowns, mass layoffs, and reduced or eliminated paychecks.

There was widespread concern amongst student loan borrowers regarding their ability to make federal student loan payments amid the Coronavirus and before the grace period was implemented.

Not only did 68% of all respondents share this worry, but so too did 79% of those that have either been laid off or seen their hours cut and 83% of those that have been furloughed because of COVID-19.

Amongst our poll participants, we found that 41% still plan to make federal student loan payments during the grace period, while 43% will not, and 15% are undecided.

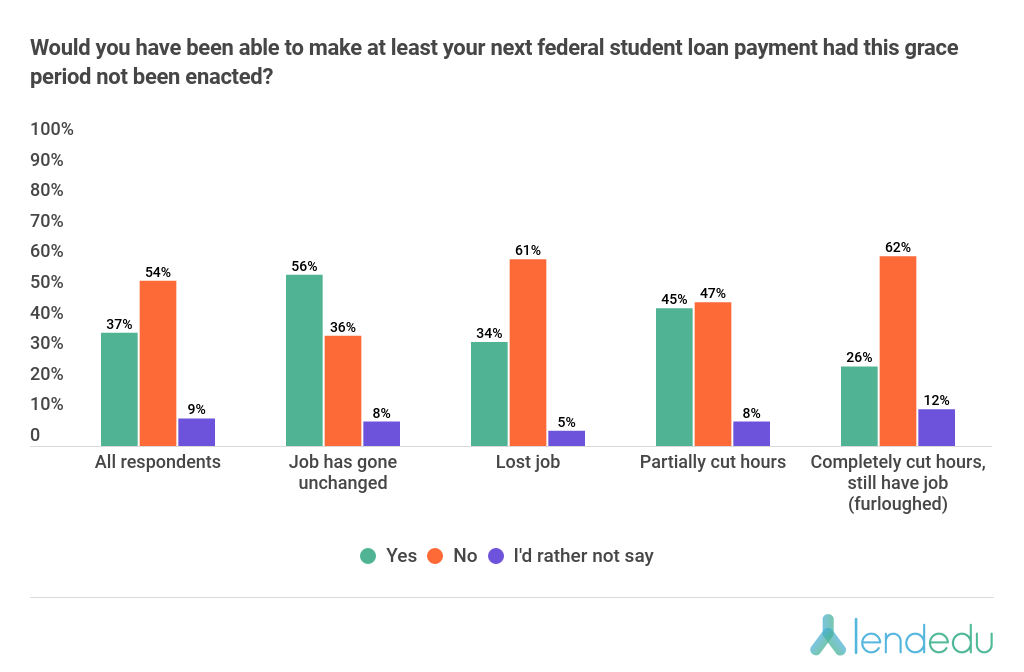

And for those that will not be making federal student loan payments, more than half of them wouldn’t have been able to make the very next payment had the grace period not been enacted.

Analyzing this data, one can only wonder what would have happened to the federal student loan ecosystem had the government not stepped in to protect federal student loan borrowers from the financial destruction being caused by the Coronavirus.

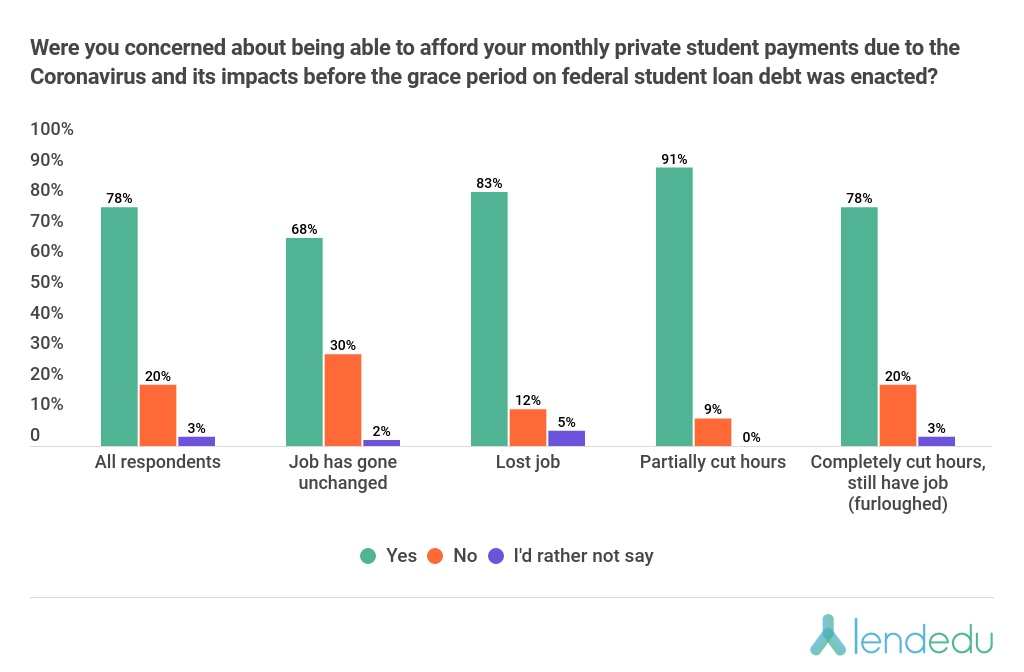

78% of Private Student Loan Borrowers Also Unsure Of Their Ability to Make Private Loan Payments

22% of our poll participants had private student loan debt. While the Coronavirus policy for federal student loans is uniform across all federal loan servicers, the relief policies amongst private student loan lenders will vary on a case-by-by basis.

We found that 78% of private student loan borrowers were concerned over their ability to make the monthly payments on that debt.

Just as it was for federal student loan borrowers, private loan borrowers were just as worried about meeting the monthly payments. But unlike federal student loans, there is no widespread interest rate freeze or payment suspension for private student loans, so borrowers could still face the financial consequences of not making payments regardless of their ability to do so.

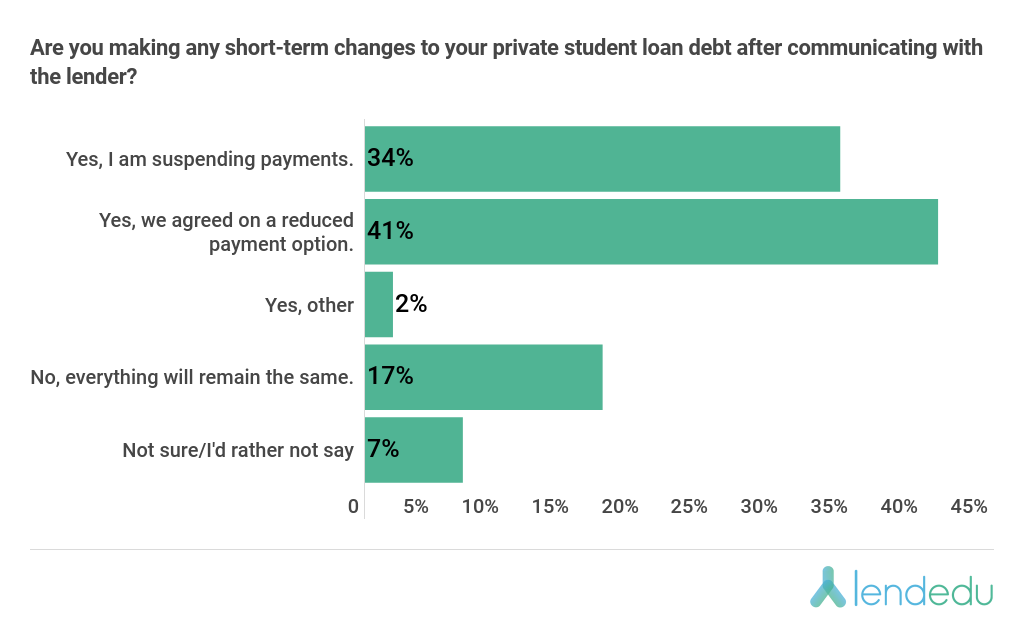

With that being said, private lenders, like many other financial institutions during this pandemic, have shown a willingness to be flexible with struggling borrowers if there is communication between both parties.

We found that 49% of private student loan borrowers have communicated with their lender to better understand their current options, while another 49% have not yet had that dialogue.

And amongst those that talked to their private lender, it appears from the survey data that a deal can be struck more times than not.

A combined 77% of respondents with private debt came to some sort of agreement with their lenders to either temporarily reduce or eliminate the financial stress that comes with having to make monthly student loan payments.

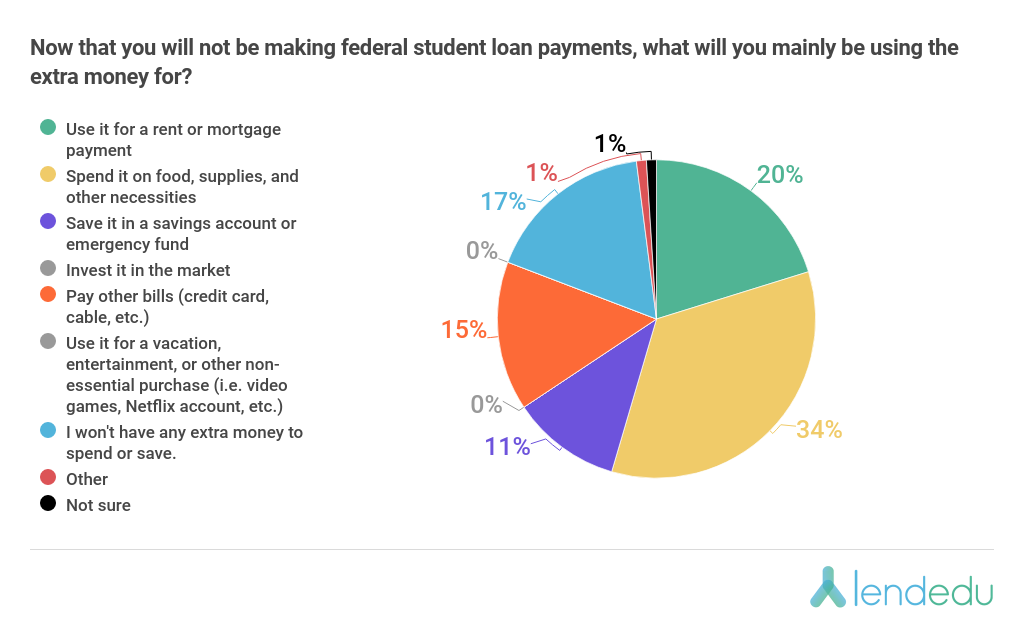

Those Not Making Federal Student Loan Payments Indicate a Desperate Need to Use the Funds For Essentials

As mentioned earlier, 43% of respondents will not be making federal student loan payments during the grace period. Let’s take a look at how they now plan to use that money.

The majority of respondents will be using this extra money for necessities. For example, 34% plan to spend it on food and supplies, 20% will use it for a rent or mortgage payment, and 15% will use it for other bills like a credit card payment.

Tellingly, no one is planning to either invest the money in the market or use it for a vacation or entertainment expense, while 17% indicated that they will have no extra money to spend or save. It is clear how tight the budgets have become for so many Americans due to the Coronavirus pandemic.

The federal student loan grace period will not only help borrowers manage their student loans, but it is also going to greatly assist many of these consumers in juggling their entire budget and making other payments like those for a mortgage.

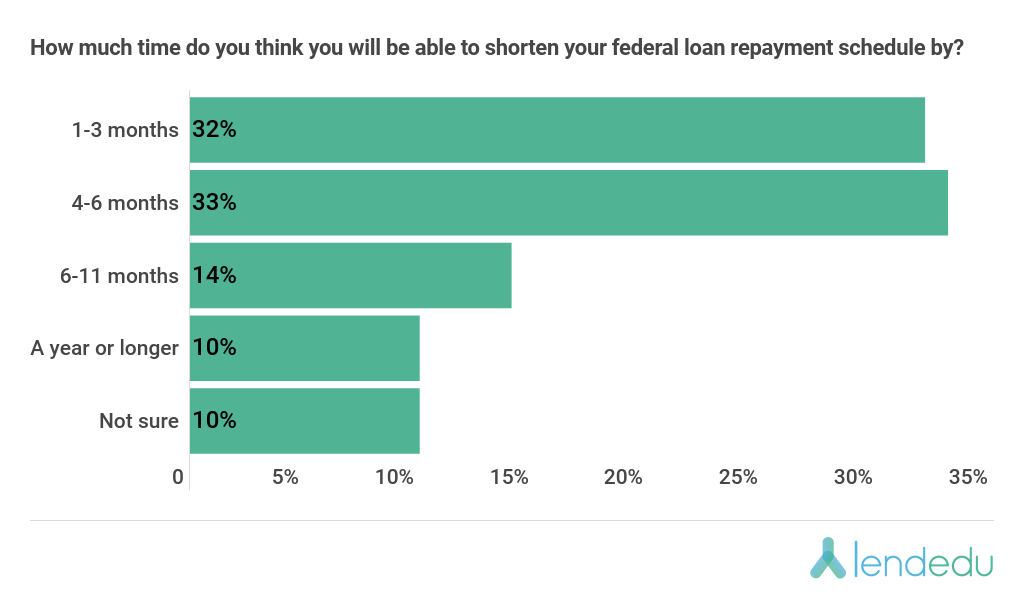

Those That Will Continue to Make Payments Anticipate Reducing Their Repayment Schedule by At Least a Few Months

Amongst the 41% of respondents that will continue to make payments on their federal student loans during the grace period, 65% of them believe they will shorten the time it takes them to fully repay their federal student loan debt.

With no interest accruing doing the grace period, borrowers can utilize their entire payments on the principal balance and certainly speed up their repayment timeline.

We asked them how many months they believe they can shave off.

The plurality of respondents, 34%, believe they can reduce their federal student loan repayment timeline by four to six months if they continue to make payments through the grace period.

Interestingly, 29%, or the plurality, of respondents that are not going to be making federal student loan payments during this time said that their federal loan repayment timeline would likely be extended by four to six months.

The grace period as it stands today is seven months so the answers on both sides make sense.

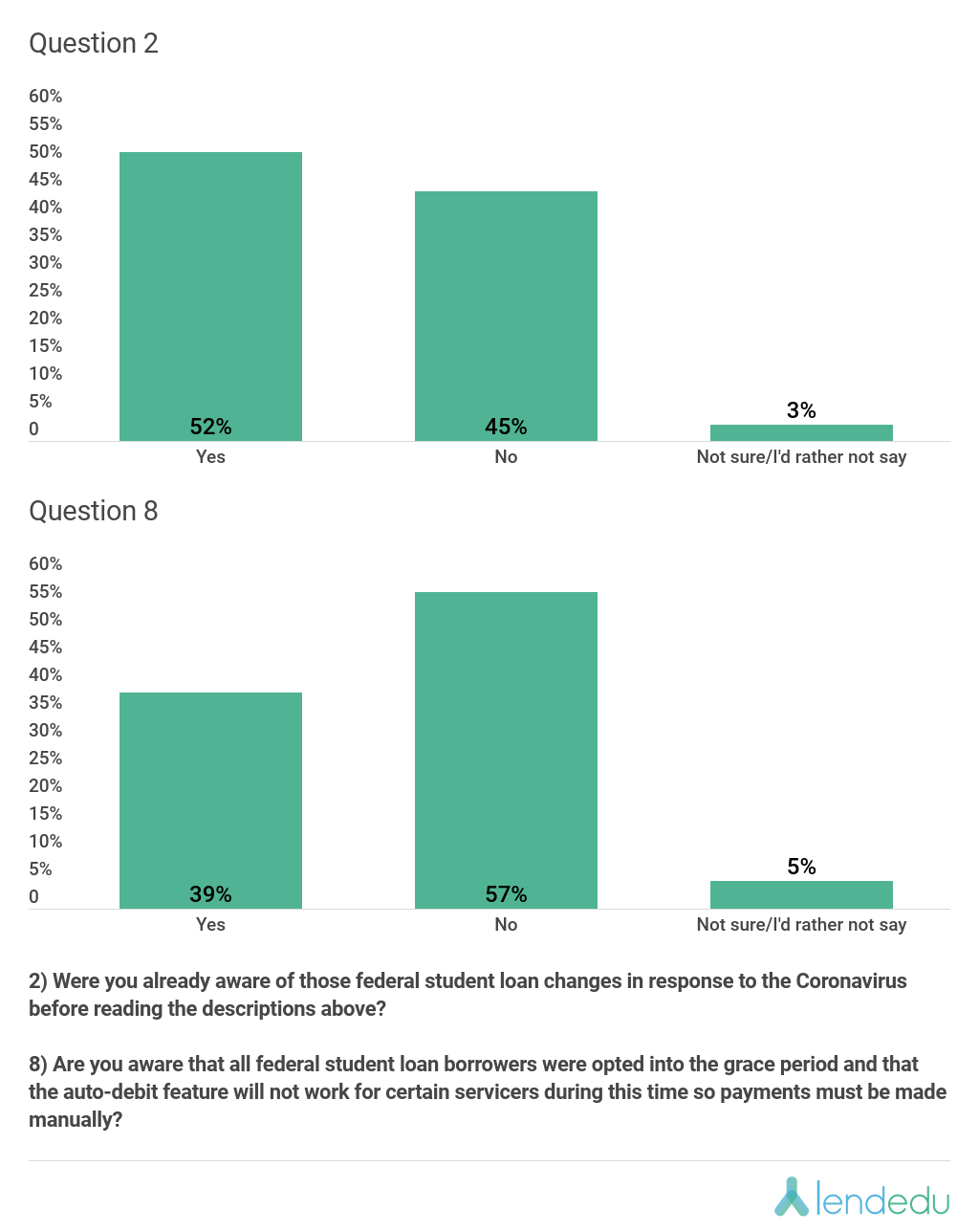

Borrower Knowledge of the Recent Federal Student Loan Changes Could Be Better

After respondents were given a description of the recent federal student loan changes, we asked them if they were aware of those changes before hand.

While the majority of borrowers were aware of the recent federal student loan changes, a considerable 45% were not. For the latter, learning of the changes will be welcomed news for many of them, but if they want to keep repaying their federal debt during the grace period there is another thing they should know.

The grace period changes were implemented uniformly across all federal student loan servicers, and all accounts were automatically placed into pandemic forbearance until September 30.

But for those who wish to keep making payments, certain servicers will still not allow them to utilize the auto-debit feature, and payments will have to be made manually each month.

As shown in the second tab of the graphic above, just 39% of borrowers that plan to keep paying their federal student loans during the grace period were aware of this change, while 57% were not.

If a borrower that wishes to keep making payments does not know this and does not actively stay on top of his or her account, they could potentially go through the entire grace period without ever making a payment.

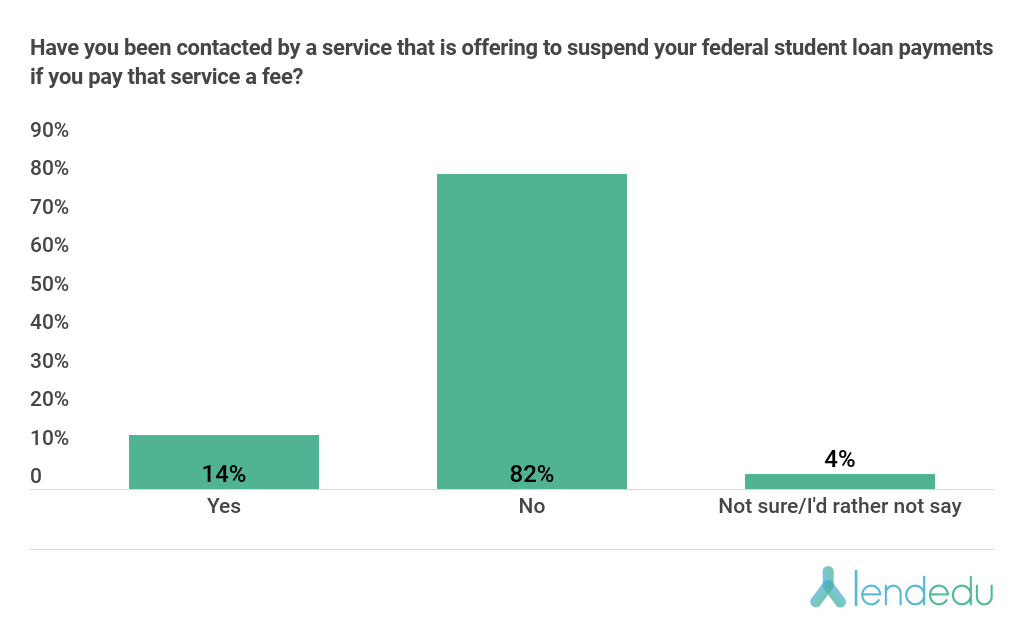

14% of Federal Student Loan Borrowers Indicate They Have Been Contacted by Scam Service Arising From Coronavirus Relief

When a monumental event takes place like a global pandemic, there is usually no shortage of scam operations looking to make a quick buck on the upheaval.

One of the many scams coming out of the COVID-19 outbreak involves a service contacting a federal student loan borrower and asking for a fee, personal information, or both in exchange for them suspending student loan payments for the borrower.

Since all federal borrowers have automatically been placed in forbearance during the grace period, there is no need for a fee or a service to do this. This is a scam and do not fall for it if such a service contacts you.

We asked our poll participants if they had been contacted by such a service.

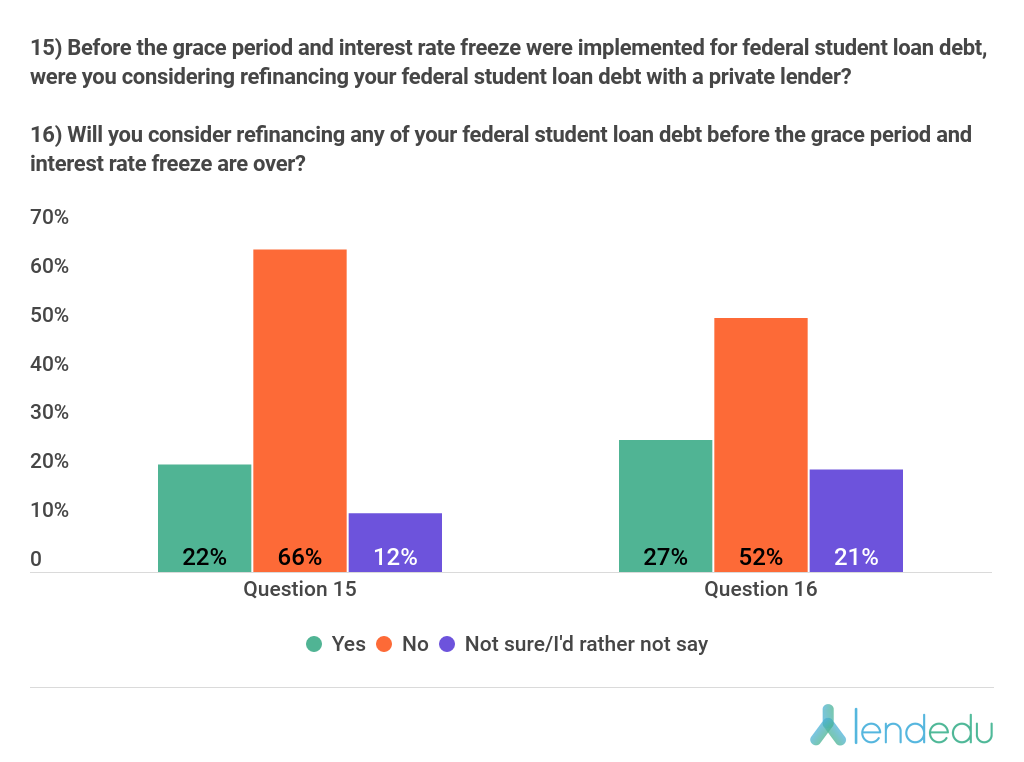

With Federal Student Loan Interest Rates Frozen at 0%, Refinancing Right Now May Not Be the Best Idea Yet Some Borrowers Are Thinking About It.

The main benefit of refinancing federal student loans with a private lender is to receive a lower interest rate. But since federal student loan interest rates are locked in at 0% until September 30 and all accounts are in pandemic forbearance, now is probably not the best time to refinance.

Amongst our survey respondents, we found that 22% of federal borrowers were considering refinancing their loans with a private lender before the grace period was implemented. 66% of poll participants were not, while 12% were undecided.

But, we also found that more than a quarter of borrowers may still consider refinancing their federal student loan debt before the grace period is over.

While everyone’s situation is different, the current grace period is a great time to take advantage of 0% interest and forbearance if necessary. Of all the times to take advantage of the possible benefits of refinancing, now is probably not the best.

Full Survey Results

All data is based on a survey of 1,000 adult Americans currently repaying their federal student loan debt that was commissioned by LendEDU and conducted by survey platform Pollfish. The survey was conducted on April 20, 2020. For some questions, the answer percentages may not add up to 100% exactly due to rounding.

If you would like to see a specific breakdown of the data other than those provided (ex. state-by-state, gender, age, employment status), or a full survey-to-survey comparison, please email me at [email protected].

1. How has the Coronavirus and its impacts changed your job status?

- 29% of respondents answered “I still have my same job, nothing has changed.”

- 14% of respondents answered “I lost my job.”

- 19% of respondents answered “My hours have been partially cut.”

- 18% of respondents answered “My hours have been completely cut, but I haven’t lost my job (furloughed).”

- 20% of respondents answered “None of the above/Already unemployed before it”

2. In response to the Coronavirus pandemic, the following changes have been made to federal student loans. Until September 30, 2020, interest rates on all federal student loans have been set to 0% and borrowers can also suspend their payments until this time. Also, borrowers who are seeking loan forgiveness through a federal program can still have skipped payments during this time count towards the forgiveness requirements. Also, borrowers in default will have suspended payments count towards the student loan rehabilitation requirements. Were you already aware of those federal student loan changes in response to the Coronavirus before reading the descriptions above?

- 52% of respondents answered “Yes”

- 45% of respondents answered “No”

- 3% of respondents answered “Not sure/I’d rather not say”

3. Before learning about these changes, were you concerned about your ability to make recurring federal student loan payments due to the Coronavirus and its impacts?

- 68% of respondents answered “Yes”

- 28% of respondents answered “No”

- 4% of respondents answered “Not sure/I’d rather not say”

4. Have you been contacted by a service that is offering to suspend your federal student loan payments if you pay that service a fee?

- 14% of respondents answered “Yes”

- 82% of respondents answered “No”

- 4% of respondents answered “Not sure/I’d rather not say”

5. Do you still plan on making federal student loan payments during this grace period when payments are not required?

- 41% of respondents answered “Yes”

- 44% of respondents answered “No”

- 15% of respondents answered “Not sure/I’d rather not say”

6. (If answered “Yes” to Q5) What do you estimate will be the size of your average monthly federal student loan payment during this grace period?

- The average estimated student loan payment amongst borrowers who intend to keep making their payments was $360.17.

7. (If answered “Yes” to Q5) Is the payment size you answered above more or less than the typical federal student loan payment you had been making?

- 8% of respondents answered “More”

- 64% of respondents answered “The same”

- 27% of respondents answered “Less”

- 1% of respondents answered “I’d rather not say.”

8. (If answered “Yes” to Q5) Are you aware that all federal student loan borrowers were opted into the grace period and that the auto-debit feature will not work for certain servicers during this time so payments must be made manually?

- 39% of respondents answered “Yes”

- 57% of respondents answered “No”

- 5% of respondents answered “Not sure/I’d rather not say”

9. (If answered “Yes” to Q5) With no interest accruing during the grace period, do you plan to use most of your monthly payment for your federal loan with the largest balance or highest interest rate?

- 18% of respondents answered “Largest balance”

- 25% of respondents answered “Highest interest rate”

- 18% of respondents answered “My largest balance has the highest interest rate, so that one.”

- 9% of respondents answered “Neither”

- 26% of respondents answered “I only have one federal loan to repay.”

- 4% of respondents answered “Not sure/I’d rather not say.”

10. (If answered “Yes” to Q5) Do you think that by repaying your federal student loans during the grace period when interest is not accruing that you will be able to shorten the time it takes you to fully repay your federal student loan debt?

- 65% of respondents answered “Yes”

- 27% of respondents answered “No, I will be on the same schedule.”

- 8% of respondents answered “Not sure”

11. (If answered “Yes” to Q5 & “Yes” to Q10) How much time do you think you will be able to shorten your federal loan repayment schedule by?

- 32% of respondents answered “1-3 months”

- 33% of respondents answered “4-6 months”

- 14% of respondents answered “6-11 months”

- 10% of respondents answered “A year or longer”

- 10% of respondents answered “Not sure”

12. (If answered “No” to Q5) Now that you will not be making federal student loan payments, what will you mainly be using the extra money for?

- 20% of respondents answered “Use it for a rent or mortgage payment”

- 34% of respondents answered “Spend it on food, supplies, and other necessities”

- 11% of respondents answered “Save it in a savings account or emergency fund”

- 0% of respondents answered “Invest it in the market”

- 15% of respondents answered “Pay other bills (credit card, cable, etc.)

- 0% of respondents answered “Use it for a vacation, entertainment, or other non-essential purchase (i.e. video games, Netflix account, etc.)

- 17% of respondents answered “I won’t have any extra money to spend or save.”

- 1% of respondents answered “Other”

- 1% of respondents answered “Not sure”

13. (If answered “No” to Q5) Without making any federal loan payments during the grace period, how much longer do you think you will be extending your federal repayment schedule by?

- 12% of respondents answered “1-3 months”

- 29% of respondents answered “4-6 months”

- 13% of respondents answered “6-11 months”

- 21% of respondents answered “A year or longer”

- 25% of respondents answered “Not sure”

14. (If answered “No” to Q5) Would you have been able to make at least your next federal student loan payment had this grace period not been enacted?

- 37% of respondents answered “Yes”

- 54% of respondents answered “No”

- 9% of respondents answered “Not sure/I’d rather not say”

15. Before the grace period and interest rate freeze were implemented for federal student loan debt, were you considering refinancing your federal student debt with a private lender?

- 22% of respondents answered “Yes”

- 66% of respondents answered “No”

- 12% of respondents answered “Not sure/I’d rather not say”

16. Will you consider refinancing any of your federal student loan debt before the grace period and interest rate freeze are over?

- 27% of respondents answered “Yes”

- 52% of respondents answered “No”

- 21% of respondents answered “Not sure/I’d rather not say”

17. Do you have any private student loan debt in addition to your federal student loan debt?

- 22% of respondents answered “Yes”

- 75% of respondents answered “No”

- 3% of respondents answered “I’d rather not say”

18. (If answered “Yes” to Q17) Were you concerned about being able to afford your monthly private student payments due to the Coronavirus and its impacts before the grace period on federal student loan debt was enacted?

- 78% of respondents answered “Yes”

- 20% of respondents answered “No”

- 3% of respondents answered “Not sure/I’d rather not say”

19. (If answered “Yes” to Q17) Have you communicated with your private student lender to better understand the possible options they are offering during this time, like suspending payments?

- 49% of respondents answered “Yes”

- 49% of respondents answered “No”

- 3% of respondents answered “I’d rather not say”

20. (If answered “Yes” to Q17 & “Yes” to Q19) Are you making any short-term changes to your private student loan debt after communicating with the lender?

- 34% of respondents answered “Yes, I am suspending payments.”

- 41% of respondents answered “Yes, we agreed on a reduced payment option.”

- 2% of respondents answered “Yes, other”

- 17% of respondents answered “No, everything will remain the same.”

- 7% of respondents answered “Not sure/I’d rather not say”

21. (If answered “Yes” to Q17 & “No” or “I’d rather not say” to Q19, or “No, everything will remain the same” to Q20) Will you be making a larger monthly private student loan debt payment than usual because of the grace period on federal student loans?

- 10% of respondents answered “Yes”

- 79% of respondents answered “No”

- 11% of respondents answered “Not sure/I’d rather not say”

Tips for Managing Your Student Loans During the Coronavirus

The coronavirus pandemic has brought about a ton of student loan changes that may impact you directly. In light of these changes, there are certain strategies you might want to implement in order to manage your student loans.

Continue Making Federal Student Loan Payments If You Can

Payments on federal student loans are not required until September 30, 2020. Additionally, there will be no interest accrued during this time. However, if you are fortunate enough to still be in a position where you can afford to make monthly student loan payments, now is a great time to do so.

With no interest accruing and the vast majority of your payments going toward the principal balance, you can really make progress toward paying off your student loans fast.

Hold Off On Refinancing Your Student Loans

Because federal student loan interest is frozen at 0% until September 30, it is not a great time to refinance your federal student loans with a private lender.

The main benefit of refinancing your student loans is to possibly receive a lower student loan interest rate, but for the time being, federal student loan interest is at 0%. Therefore, you likely won’t be reaping the benefits of student loan refinancing if you choose to go in that direction.

If You Have Private Student Loans, Talk To Your Lender if You’re Struggling With Payments

While federal student loan payments are not required until September 30, there is no such rule currently in place for private student loans. However, many private student loan lenders have shown a willingness to be flexible during this time, so communicate with your lender to better understand your repayment options.

Methodology

All data found within this report is based on a survey commissioned by LendEDU and conducted online by survey platform Pollfish. In total, 1,000 adult Americans that are currently repaying federal student loan debt were surveyed. The appropriate respondents were found via Pollfish’s age filtering feature, in addition to utilizing a screener question to ensure all respondents were repaying federal student loan debt. This survey was conducted on April 20, 2020. All respondents were asked to answer all questions truthfully and to the best of their abilities.

See more of LendEDU’s Research

About our contributors

-

Written by Mike Brown

Written by Mike BrownMike Brown uses data from surveys and publicly available resources to identify emerging personal finance trends and tell unique stories.