Our take: Valley Strong’s HELOC mirrors the top-rated Figure HELOC in nearly every way. The main differences are branding, maximum funding amount, and availability in the state of Alaska. Applying through Valley Strong may appeal to members who prefer working with a familiar credit union name, but most borrowers can get the same product directly through Figure.

HELOC

- Quick application process

- Fixed interest rates

- Product is through Figure, our team’s pick for the best HELOC provider

- No in-person appraisal needed

- Option to redraw up to 100% of funds

- Funding can be available in as few as 5 days

- Check your rate without affecting your credit score

- Don’t need to be a Valley Strong Credit Union member to apply for the HELOC

- Mixed reviews

- 100% of funds are drawn at origination

- Origination fee of up to 4.99%

- No clear benefit to applying through Valley Strong rather than directly through Figure

| Rates (APR) | 8.35% – 16.55% |

| Funding amount | $15,000 – $750,000 |

| Repayment terms | 5, 10, 15, or 30 years |

| Min. credit score | 640, but 720+ is advised |

Valley Strong’s home equity line of credit (HELOC) is powered by Figure, the highest-rated HELOC provider LendEDU has rated. Figure’s proprietary blockchain-based loan processing allows for fast approvals, digital income verification, and funding in as little as five days.

Valley Strong HELOC overview

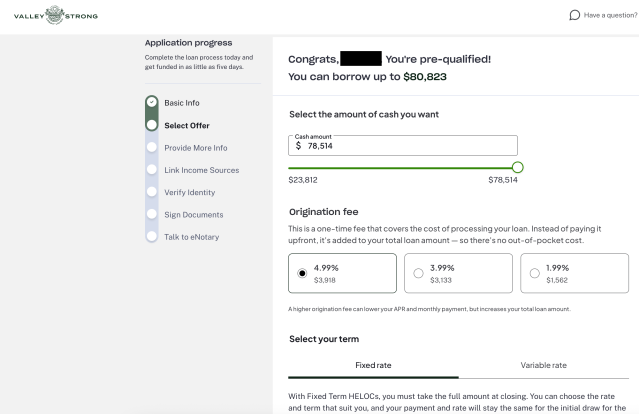

You can check your rate online without affecting your credit score and, once approved, receive funding in as little as five days. Valley Strong’s HELOC through Figure features fixed interest rates, flexible repayment terms of five, 10, 15, or 30 years, and borrowing limits of up to $750,000, depending on your credit, income, and home equity.

Funds can be used for nearly any major expense, such as home renovations, debt consolidation, education costs, or emergency expenses, and you can redraw up to 100% of your available credit once the balance is repaid.

HELOC highlights

Some details that may make this HELOC option appeal to eligible homeowners:

Repay anytime

Figure doesn’t impose any prepayment penalties on HELOCs, so you can repay your loan early and save on interest without risking extra fees.

Quick approval

The initial prequalification only takes minutes, and if approved, you may access the funds in as little as five days.

$1,000 bonus with a Makes Cents Checking Account

Right now, Valley Strong offers a $1,000 bonus if you open a Makes Cents Checking Account alongside a HELOC of at least $50,000.

Who is eligible?

Unlike most credit union HELOCs, the Valley Strong HELOC through Figure is available in 47 states and Washington, D.C. (Not available in New York, Hawaii, and Alaska.) You do not need to be a Valley Strong Credit Union member to apply.

Eligibility is based on Figure’s standard HELOC criteria, which generally include:

- Credit score: Minimum 640; a score of 720 or higher is recommended for approval.

- Loan-to-value ratio (LTV): Typically up to 85%, depending on your credit profile and state regulations.

- Property type: Single-family homes, townhomes, and condos are eligible. Manufactured and multi-unit properties generally do not qualify.

- Occupancy: Primary residences, second homes, and investment properties may all be eligible.

- Condition: The property must be in at least average condition and located within the United States.

Read more about HELOC requirements.

Because the product is underwritten by Figure, most of the process, including income verification, digital appraisal, and closing, is handled online. That means you can complete the entire HELOC process without visiting a branch or submitting paper documents.

Good to know: If you already bank with Valley Strong, you can still apply through the credit union to receive the same HELOC as Figure customers, plus access to Valley Strong’s $1,000 checking account bonus for qualifying HELOCs.

Application process

The application is handled through Figure’s online platform, which streamlines the process from start to finish.

You’ll begin by completing a brief prequalification form, which will not affect your credit score. During this step, you’ll provide:

- Property address and occupancy type (primary, secondary, or investment)

- Estimated home value and mortgage balance

- Income information

- Basic personal details such as your name and date of birth

Once prequalified, you’ll receive an estimated rate and terms.

If you choose to move forward, Figure will handle the full digital application, verification, and e-notary process. Funding is typically available within five days of final approval.

Because this HELOC is powered by Figure, applicants do not need to be Valley Strong members to apply.

Pros and cons

Pros

-

Risk-free prequalification that won’t affect your credit score

-

Quick, straightforward digital application process powered by Figure

-

No prepayment penalties

-

Available in most states (not limited to California)

-

Funding in as little as 5 days

-

$1,000 checking account bonus for qualified borrowers

-

Figure (the HELOC servicer) earns great customer service reviews.

Cons

-

The credit union’s online reviews are limited and mixed

No Trustpilot page, no BBB accreditation.

-

Essentially identical to the Figure HELOC, with little benefit for applying through Valley Strong

-

HELOC rates and terms not displayed transparently on Valley Strong’s site

Alternatives

If you want to make sure you’re getting a competitive offer, we always recommend comparing different HELOC lenders and rates, including these leading HELOC providers:

Valley Strong vs. Figure

Valley Strong’s HELOC is actually powered by Figure, which originates and services the loan. That means the two products share nearly identical features, including rates, funding amounts, term lengths, eligibility requirements, and the following:

- Availability: 47 states + D.C.

- Funding speed: As fast as five days after approval

The main difference is branding. When you apply through Valley Strong, you’re technically still applying for a Figure HELOC. The credit union acts as a white-label partner. Borrowers who already have accounts with Valley Strong may appreciate the consistency of seeing the credit union’s name on their documents, but there’s no difference in cost, eligibility, or processing.

What this means: Unless you specifically want to work through Valley Strong, applying directly with Figure offers the same HELOC with the same terms, and access to Figure’s award-winning customer support.

Valley Strong vs. Aven

Aven is another top-rated HELOC provider with an ultra-fast application process. If the screening goes smoothly, Aven may approve your HELOC application within 15 minutes.

Aven stands out thanks to its Lowest Rate Guarantee: If you can prove you have received a better HELOC deal from another provider, Aven commits to offering you a HELOC with a lower APR.

Valley Strong vs. FourLeaf

FourLeaf Federal Credit Union offers a 20-year HELOC with an initial 12-month fixed rate, no application, appraisal, or origination fees, and zero closing costs. The maximum borrowing amount is $1 million, substantially higher than Figure’s upper limit.

Customer reviews

Valley Strong has limited reviews, likely because it’s a regional credit union. It isn’t BBB-accredited and has no Trustpilot page.

Nevertheless, Valley Strong is a well-established financial institution with a strong local presence and a reputation built on nearly 90 years of service.

However, if you go through Valley Strong to get a HELOC, you’ll deal primarily with Figure. Here’s how Figure’s customer service rates:

| Source | Customer rating | Number of reviews |

| Trustpilot | 4.8/5 | 3,941 |

| Better Business Bureau (BBB) | 1.66/5 | 29 |

| 3.7/5 | 25 |

Who should apply for a HELOC with Valley Strong?

The Valley Strong HELOC could suit borrowers who want the convenience of Figure’s digital HELOC experience while maintaining a relationship with a trusted credit union. However, since the product and terms are identical, most homeowners will find it simpler to apply directly through Figure, which offers the same HELOC nationwide and earns LendEDU’s Best Overall HELOC designation.

Editor’s note: Valley Strong’s HELOC is powered by Figure and follows Figure’s eligibility criteria, rates, and approval process. Borrowers applying through either lender will receive the same HELOC terms.

About our contributors

-

Written by Anna Twitto

Written by Anna TwittoAnna Twitto is a money management writer passionate about financial freedom and security. Anna loves sharing tips and strategies for smart personal finance choices, saving money, and getting and staying out of debt.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.