Cancer treatments are exhausting—and often expensive. Patients deserve a break from the other financial obligations in their lives, student loans included. That’s why Congress passed the Deferment for Active Cancer Treatment Act of 2017.

The act allows individuals with certain student loans to defer them when undergoing cancer treatments. Patients get an additional six months of deferment after treatment ends.

At the time of writing, all federal student loans are on pause. But when they resume, patients can continue to defer them for as long as needed with the help of the Deferment for Active Cancer Treatment Act.

Table of Contents

- How does the Deferment for Active Cancer Treatment Act help borrowers?

- What types of student loans are eligible for the Deferment for Active Cancer Treatment Act?

- What should I do if I want to defer my loans while receiving cancer treatment?

- How many times can I defer my federal student loans for cancer treatment?

- Do borrowers with private student loans who are getting cancer treatment have options?

- Can I defer paying my loans due to illnesses besides cancer?

How does the Deferment for Active Cancer Treatment Act help borrowers?

Qualifying for cancer treatment deferment has two requirements:

- Patient has a federal loan they’re making payments on.

- They’re undergoing cancer treatment.

The act offers loan deferment for the entire length of the cancer treatments plus six months after treatment ends. There’s no time limit on the deferment. As long you’re undergoing cancer treatment, you’ll qualify, even if treatments last for years.

The act got off to a rocky start, with borrowers unable to access an application for months after the act passed. Lenders were confused about handling requests for deferment, with little guidance from the Department of Education. Some patients found they were denied this deferment for no reason.

While many issues are now ironed out, it’s wise to contact your loan servicer before submitting an application to help ensure your request will be approved.

What types of student loans are eligible for the Deferment for Active Cancer Treatment Act?

The act only applies to federal student loans. These are loans issued by the U.S. government rather than private lenders.

Specific federal loans qualify under the act, including:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans made to students or parents

- Direct Subsidized Consolidation Loans

- Direct Unsubsidized Consolidation Loans

- Direct PLUS Consolidation Loans

- Federal Perkins Loans

- Federal Subsidized Stafford Loans

- Federal Unsubsidized Stafford Loans

- Federal Subsidized Consolidation Loans

During the deferment, the loans above won’t accrue interest the way loans in economic hardship deferment often do.

Loans that will continue accruing interest are ineligible for deferment and therefore placed in forbearance. These include:

- Federal PLUS Loans made to students or parents

- Federal Unsubsidized Consolidation Loans

- Supplemental Loans for Students (SLS)

What should I do if I want to defer my loans while receiving cancer treatment?

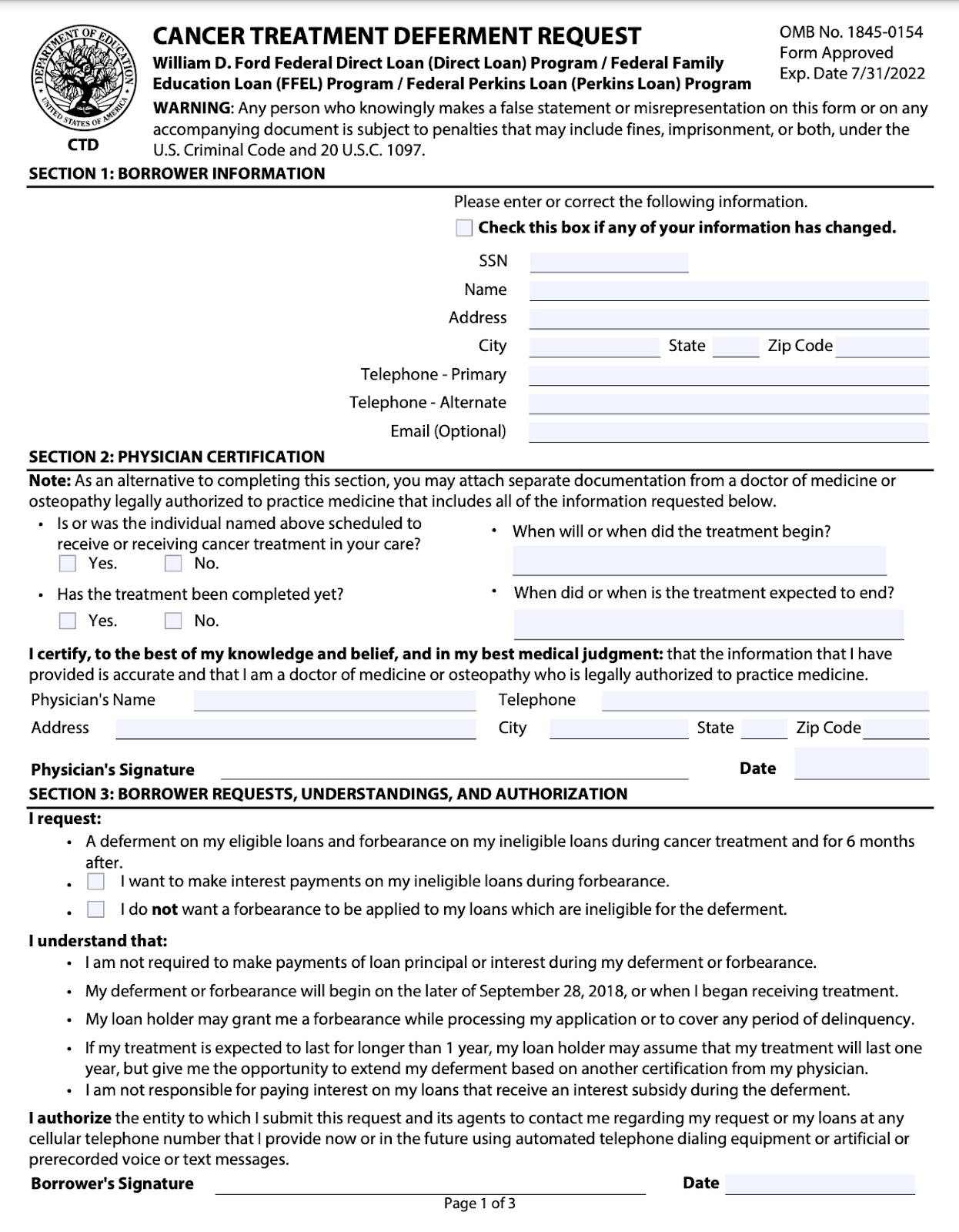

If you’re going through cancer treatment and want to request a deferment, you can fill out an application from the Department of Education. The linked form expired at the end of July 2022 and hasn’t been renewed. This is likely because the ongoing deferment of federal loans means there’s no need for an updated form. Continue to check back here for a new form when payments resume.

The application is simple:

Source: StudentAid.gov

It consists of a “personal information” section for your:

- Social Security number

- Address

- Phone number

Your physician must fill out the next section, which confirms you’re receiving cancer treatments. Rather than complete this section, you can also attach a letter from your doctor that confirms this.

Then you’ll select how to handle the forbearance on the deferment-ineligible loans listed above, if applicable.

To apply, you must print the PDF and send it to the address in Section 6 of the application.

If no address is shown, you must send it to your lender. When you make initial contact with your lender, it can help ensure you send the application to the correct place.

How many times can I defer my federal student loans for cancer treatment?

There’s no limit on deferment when you’re undergoing cancer treatment. So if you have to undergo treatment more than once, you can qualify each time.

If you have a physician confirm you’re undergoing treatment, you can submit another deferment application.

Do borrowers with private student loans who are getting cancer treatment have options?

The Deferment for Active Cancer Treatment Act only applies to federal loans, but those with private student loans may still have options. Plenty of private lenders offer deferment or forbearance options for borrowers in school, in the military, or going through difficult financial times.

These private lenders may offer deferment for patients with cancer. Speak with a customer service representative from your lender, and explain your situation. While lenders may not offer deferment for as long as the federal act does, they may offer something in the way of support.

If your lender doesn’t offer deferment for cancer treatments, you can refinance your loan with a lender that provides this or another kind of deferment. While this process isn’t immediate, it can help you work with a fairer lender—ideally at a lower interest rate.

Can I defer paying my loans due to illnesses besides cancer?

While this specific deferment act applies to cancer patients, cancer isn’t the only illness that qualifies borrowers for other forms of deferment or forgiveness.

For federal student loans, those diagnosed with a total and permanent disability can qualify for the discharge of their student loans.

Illnesses that may qualify include:

- Chronic fibromyalgia

- Major depression

- Bipolar disorder

- Degenerative disc disease

You can qualify with documentation from Veterans Affairs, the Social Security Administration, or your physician that shows you’ve been diagnosed with one of these illnesses.

Another form of deferment is rehabilitation training deferment, specific to veterans or active-duty military.

If you’re sent to a qualifying rehab facility to recover from an injury, you may be able to cease making payments during the program. The program you’re part of must be licensed or approved as a rehabilitation facility by the Department of Veterans Affairs.

About our contributors

-

Written by Christopher Murray

Written by Christopher MurrayChristopher Murray is a freelance personal finance and sustainability writer. He graduated from Smith College with bachelor’s degrees in English literature and gender studies. He also served as a personal finance editor for five years.