When paying for college, students and parents should first apply for scholarships and grants, then federal student loans, and finally, private student loans if there are still gaps left to be filled.

For decades now, the cost of college has increased at a rate that has outpaced inflation. As a result, the private student loan market has boomed.

There is now $131 billion in outstanding private student loan debt in the U.S. and more than 100 private student loan lenders.

To capture this growing market, LendEDU dove into our private student loan data to uncover important trends and data points. The data derives from the hundreds of thousands of users who have gone through our private student loan portal since 2016.

Below, you will find key private student loan trends from 2020 and see how this year’s data compares to the previous four years.

Private Student Loan Data From 2016 to 2020

The data points that you will find below contained sufficient data from 2020 to include that year in the analysis.

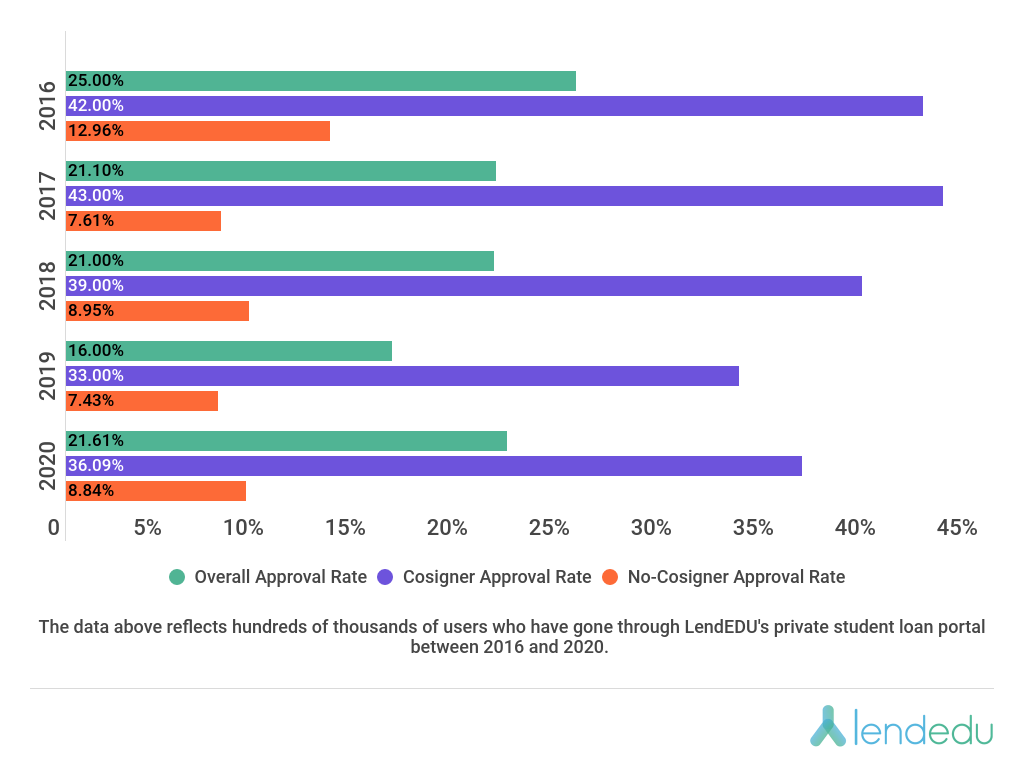

Approval Rates

- In 2020, the overall private student loan approval rate was 21.61%.

- In 2020, the private student loan approval rate for applicants who applied with a cosigner was 36.09%.

- In 2020, the private student loan approval rate for applicants who did NOT apply with a cosigner was 8.84%.

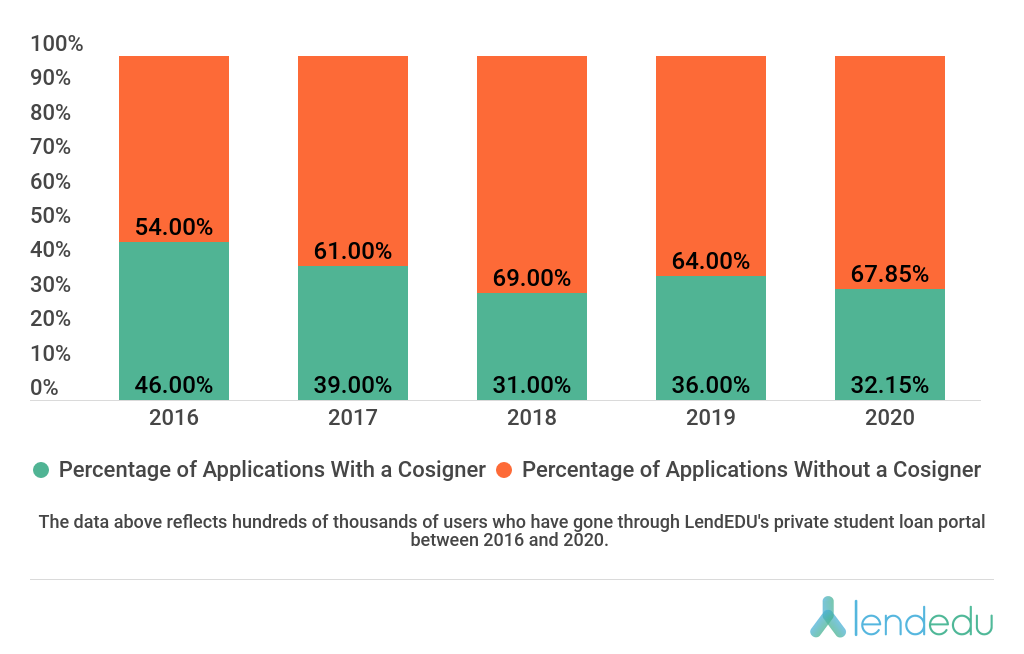

Cosigner vs. No-Cosigner Applications

- In 2020, 32.15% of private student loan applicants applied with a cosigner, while 67.85% of applicants applied without a cosigner.

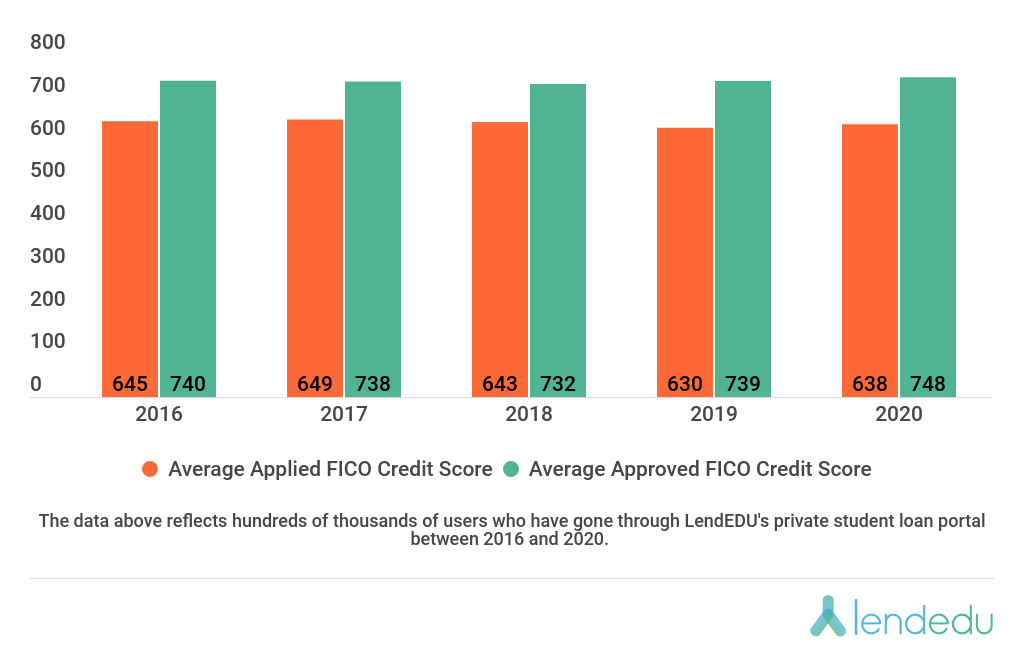

Average Applied vs. Approved Credit Score

- In 2020, the average private student loan applicant had a FICO credit score of 638.

- In 2020, the average APPROVED private student loan applicant had a FICO credit score of 748.

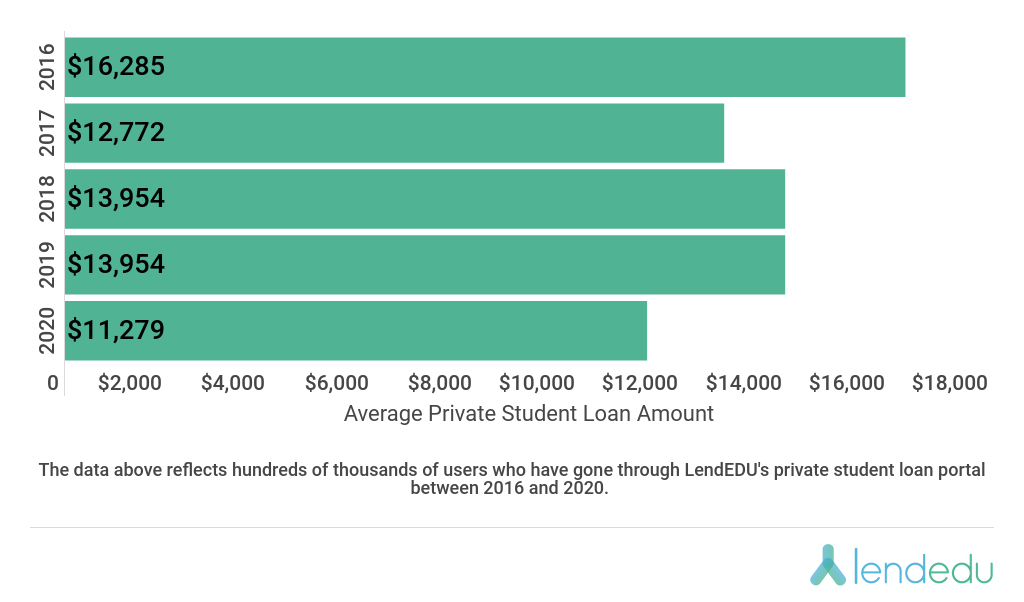

Average Funded Private Student Loan Amount

- In 2020, the average funded private student loan amount was $11,729.

Private Student Loan Data From 2016 to 2019

The data points that you will find below contained insufficient data from 2020 so only data from 2016 to 2019 was included in the analysis.

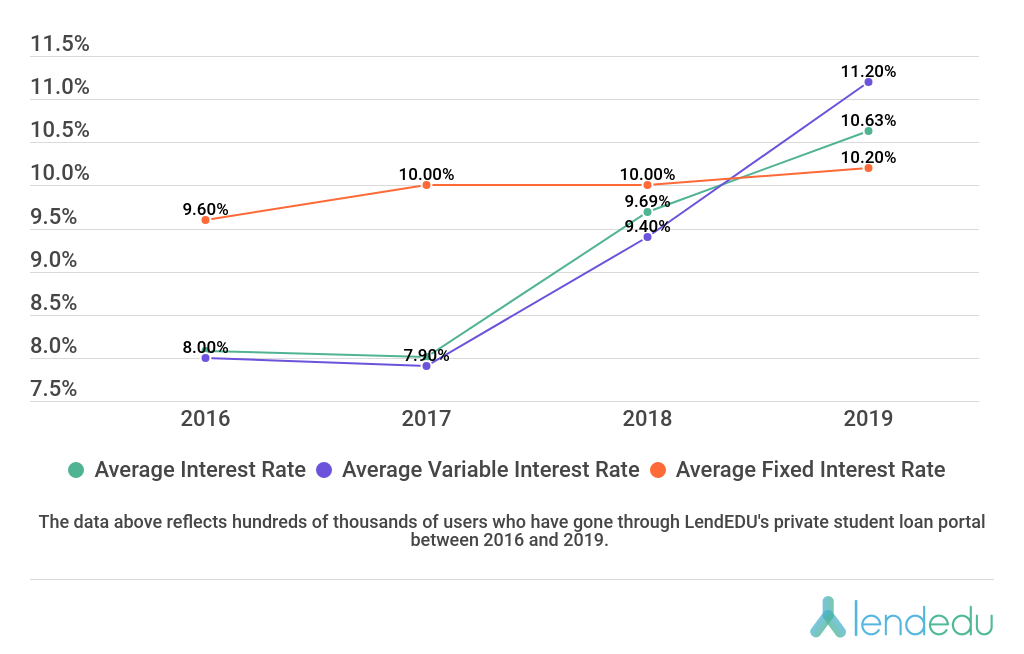

No-Cosigner Interest Rates

- In 2019, the average interest rate on a private student loan was 10.63%.

- In 2019, the average VARIABLE interest rate on a private student loan was 11.20%.

- In 2019, the average FIXED interest rate on a private student loan was 10.20%.

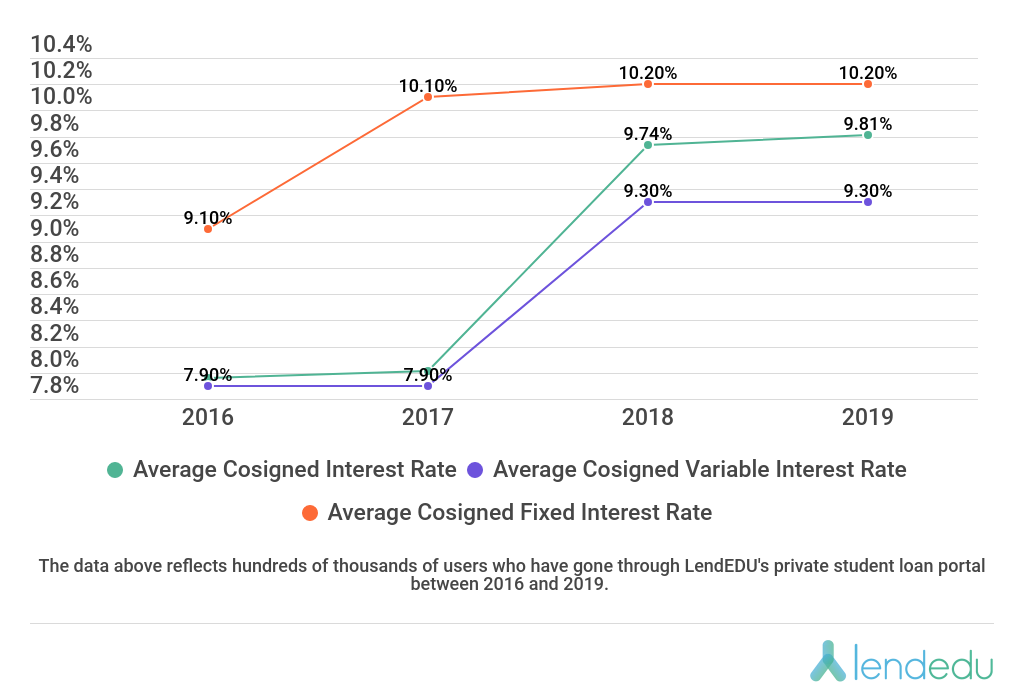

Cosigned Interest Rates

- In 2019, the average cosigned interest rate on a private student loan was 9.81%.

- In 2019, the average cosigned VARIABLE interest rate on a private student loan was 9.30%.

- In 2019, the average cosigned FIXED interest rate on a private student loan was 10.20%.

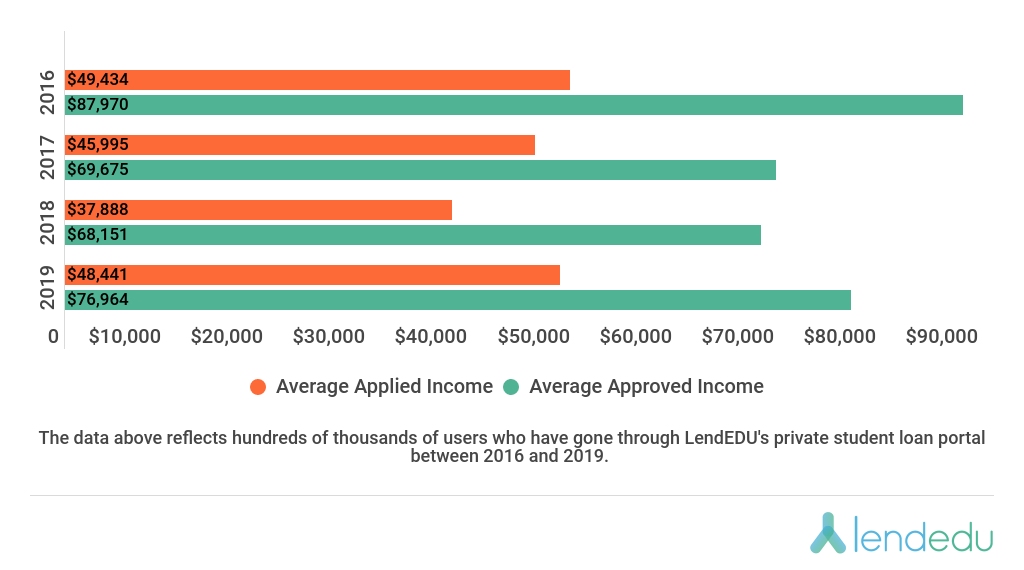

Average Applied vs. Approved Income

- In 2019, the average private student loan applicant had an income of $48,441.

- In 2019, the average APPROVED private student loan applicant had an income of $76,964.

Student Loan Tips

These days, most students will require student loans to complete their college education.

When it comes to taking out student loans and managing repayment, LendEDU gives a few tips below.

Compare All of Your Options

If you are in the market for private student loans, the most important thing you can do is compare the various lenders out there so that you can give yourself the best chance at getting favorable terms.

For example, you could look into private student loans from companies like College Ave, Citizens Bank, Earnest, and ELFI. Then, there are bad credit student loan options, in addition to student loans for parents.

Consider Refinancing Eventually

After you are done with college and have demonstrated a history of successful student loan repayment, you should consider refinancing your student loans to possibly receive a lower student loan interest rate or more favorable repayment terms.

You are even able to refinance your student loans more than once if you believe that you can get offered even better repayment terms than before.

Implement a Repayment Strategy

If you are trying to repay your student loans fast, you must implement a repayment strategy that will allow you to repay your debt in a timely and efficient manner.

For example, you could make bi-weekly student loan payments instead of just one per month, pay off high-interest student loans first, or pay more than the monthly minimum.

Methodology

All data used in this report was compiled from hundreds of thousands of users who went through LendEDU’s private student loan portal when applying for a private student loan between 2016 and 2020. Data has been provided from a variety of private student loan lenders.

The application data was pooled from the five aforementioned companies and averaged together.

Each lender provides slightly different reporting and data. Therefore, some lenders did not provide certain data fields. Due to privacy concerns, we are unable to provide or confirm lender-specific data. Some data points did not include data from 2020 due to an insufficient amount of data from all private student loan lenders.

See more of LendEDU’s Research

About our contributors

-

Written by Mike Brown

Written by Mike BrownMike Brown uses data from surveys and publicly available resources to identify emerging personal finance trends and tell unique stories.