Student loan default occurs when you fail to repay your loan as promised. Default time frames vary depending on whether you have federal or private student loans.

Once you’ve defaulted, your lender or loan servicer reports this information to the credit bureaus. As a result, it can cause severe damage to your credit file, making it harder for you to qualify for financial products such as mortgages and auto loans.

But the good news is that it’s possible to remove a default from your credit report in certain situations, even if the reported default is accurate.

- No application or repayment fees

- Great for borrowers with Poor or Fair credit

- Flexible payment terms

- Refinance without a degree

- 7+ years assisting distressed borrowers improve their credit score

- Checking rates will not impact your credit score

Can you remove student loan default from your credit report?

Whether you can remove a student loan default from your credit file largely depends on whether it’s accurately reported.

It also matters whether your loans are federal or private. Federal loans come with access to several options that allow you to remove even accurately reported defaults from credit reports.

Private lenders aren’t required to remove accurately reported defaults from your credit. But you can take steps to remove the default if it’s inaccurately reported.

How to remove an accurate student loan default from your credit report

You can get out of default in various ways, but not every method leads to removing an accurate student loan default from your credit profile.

For example, though it’s difficult to refinance a defaulted student loan—swap out an existing loan with a new private loan—it’s possible. But doing this doesn’t remove the default.

You can get out of federal student default by consolidating your loans with a Direct Consolidation Loan, but this also doesn’t lead to removing the default from your credit file.

The only surefire way to remove an accurate federal student loan default is loan rehabilitation or the Fresh Start program. Private lenders might not offer this as an option, but even if they do, there’s no guarantee the lender will remove the default.

| Removes federal loan defaults? | Removes private loan defaults? | |

| Loan rehabilitation | Yes | Varies by lender |

| Fresh Start program | Yes | No |

Loan rehabilitation

Here’s how federal loan rehabilitation works.

What it is

Loan rehabilitation is a type of repayment plan that allows you to get out of student loan default. For federal loans, you can rehabilitate your loans and remove an accurate student loan default from your credit history after making nine payments within 10 successive months.

What you need to know

Though federal loan rehabilitation removes a default from your report, it takes almost a year to complete the process and it doesn’t protect you from tax refund garnishment during that time period.

Who’s eligible?

To see whether you qualify, you must contact your student loan servicer and share your most recent tax return.

Fresh Start

Below is some information on how this federal program works.

What it is

The Fresh Start program is designed to help federal student loan borrowers who defaulted before the pandemic get out of default. Like loan rehabilitation, it removes a default from your credit reports.

What you need to know

The last day to enroll in the Fresh Start program is August 31, 2024. Enrolling stops your wages from being garnished because of a student loan default.

Who’s eligible?

You might be eligible if you defaulted on a Federal Direct Loan, Perkins Loan held by the Department of Education, or a Federal Family Education Loan (FFEL).

If you have a private student loan, an accurately reported default will likely stay on your credit report until information naturally falls off—after seven years.

If you’re working to repair credit after a default, consider looking into a secured credit card. You’ll pay a deposit and receive a credit card equal to the deposit amount. Every month you pay your bill on time, the lender will report it to the credit bureaus, improving your payment history and credit score. As a result, your payment history will improve, and so will your credit score.

Eric Kirste, CFP®

What to do if the reported default is not accurate

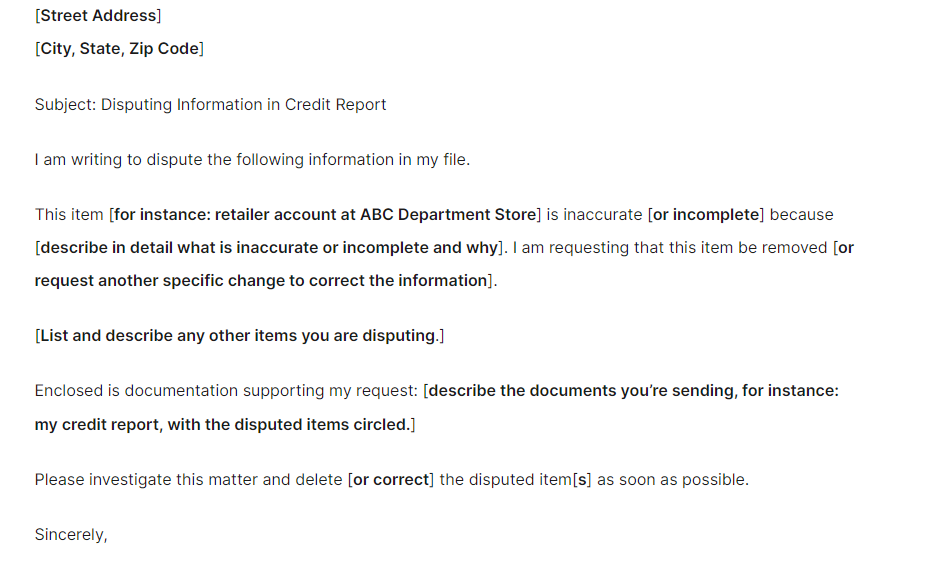

If a reported default appears on your credit report but is inaccurate, you can dispute it and have it removed.

But first, you have to spot the inaccuracy. To do that, review your credit reports from all three major credit bureaus—Equifax, Experian, and TransUnion—to catch a potential inaccurate default. You can view your reports for free by going to AnnualCreditReport com.

If you see a default listed and your loan is current, you can dispute it with the respective bureau online, by mail, or by phone. The Federal Trade Commission has sample dispute letters you can use on its website.

Source: FTC.gov

Here is how to contact the credit bureaus:

| Credit bureau | Contact information |

| Equifax | Online: Equifax online dispute page Mail: P.O. Box 740256, Atlanta, GA 30374-0256 Phone: 1-888-378-4329 |

| Experian | Online: Experian online dispute page Mail: P.O. Box 4500Allen, TX 75013 Phone: 1-866-200-6020 |

| TransUnion | Online: TransUnion online dispute page Mail: TransUnion Consumer Solutions, P.O. Box 2000 Chester, PA 19016-2000 Phone: 1-800-916-8800 |

Before you submit a dispute, gather documents that support your claim, like billing statements. You may also be asked to provide.

- Your Social Security number

- The address of all the places you’ve lived in the past two years

- Date of birth

- Government-issued ID

- Utility bill

After you’ve submitted a dispute, the credit bureaus generally have up to 30 days to investigate your claim. However, they can extend their investigation by 15 more days if you receive a copy of your credit report from AnnualCreditReport.com before filing the dispute.

After the credit bureau finishes its investigation, it has five days to notify you of the outcome. If your claim is successful, the inaccurate student loan default will be removed from your credit report.

It typically takes a month for credit agencies to update your report. Your credit score could improve once the default is removed.

How long does student loan default stay on your credit report?

A student loan default generally remains on your credit reports for up to seven years. However, if you rehabilitate your federal student loan, the Department of Education will ask the credit bureaus to remove it from your credit file.

Even if a private lender offers its version of loan rehabilitation, the law doesn’t require it to remove the default from your credit report.

If you’re concerned about defaulting on federal student loans, consider enrolling in an income-driven repayment (IDR) plan to potentially lower your monthly payments, or temporarily pause your monthly payments through forbearance or deferment. For private student loans, contact your lenders to discuss possible options.

If you’re struggling to make loan payments, it is critical to sit down and take a deep look at your finances. Look for ways to trim out excess expenses and divert those savings to your loans.

Eric Kirste, CFP®

About our contributors

-

Written by Jerry Brown, CFEI®

Written by Jerry Brown, CFEI®Jerry Brown is a freelance personal finance writer and Certified Financial Education Instructor℠ (CFEI®) who lives in New Orleans. He covers a range of personal finance topics, including credit, personal loans, and student loans.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Eric Kirste, CFP®

Reviewed by Eric Kirste, CFP®Eric Kirste, CFP®, CIMA®, AIF®, is a founding principal wealth manager for Savvy Wealth. Eric brings more than two decades of wealth management experience working with clients, families, and their businesses, and serving in different leadership capacities.