Deciding whether to finance a car through a dealer or a bank depends on your needs and comfort level. Dealer financing offers convenience, especially if you need a car right away or prefer not to shop for a loan yourself.

However, bank financing might save you money, with lower interest rates and less dealer involvement. We’ll explain the pros and cons of each option to help you choose the best fit for your situation.

Table of Contents

Car dealer financing vs. bank financing at a glance

With dealer-arranged financing, the dealer works with lenders on your behalf to find a loan. In contrast, bank financing involves you applying with lenders. Here are some of the primary differences between the two, which we’ll cover in more depth below:

| Dealer financing | Bank financing |

| ✅ The dealer can shop your credit application to multiple lenders | ✅ Your interest rate won’t include compensation for a dealer |

| ❗ The dealer may offer a higher interest rate than the lender’s quote | ❗ Shopping around on your own can take extra time |

| ✅ The dealer can provide the lender with all the financial details | ✅ You can work with lenders and get approval at your leisure |

| ❗ You may be stuck at the dealership for hours waiting to finalize the loan | ❗ Your loan terms may change if the final numbers don’t match up with your estimates |

Car dealer financing

How it works

Once you choose your vehicle and negotiate the price, you’ll fill out a credit application at the dealership, and the dealer will submit it to multiple lenders on your behalf.

This process is also called indirect financing because you’re not working with the lenders; the dealership is. Lenders that approve your application will give the dealer a quote, called the buy rate. However, your interest rate may be higher.

Because dealers work with a variety of lenders, you may be able to obtain a loan even if you have fair or poor credit. However, you may need to provide proof of income, proof of residence, references, and other documents.

Pros and cons

It helps to consider the pros and cons before you decide which type of financing is best for you.

Pros

-

Convenient

If you don’t have time to research and compare auto loans on your own or the process feels daunting, opting for dealer-arranged financing is simple and easy.

-

Flexibility

Some bank lenders require you to buy from a dealer in their network, limiting your flexibility when searching for a car. With dealer financing, you can focus on getting the right car rather than the right dealer.

-

Promotional financing

If you’re buying a new car and have great credit, you may qualify for promotional financing through the manufacturer. Manufacturer lending divisions don’t offer direct loans.

Cons

-

Potentially higher rate

The dealer may charge a higher rate than you could get on your own, taking the difference as compensation.

-

Less control over the process

You don’t get to choose which lenders the dealer sends your credit application to, and the dealer may not even show you all the offers it receives.

-

The process can be time-consuming

Even if you have all the necessary paperwork, it could take hours for the dealer to finalize a loan with a lender. Even after you get the keys, the lender could have lingering requirements.

Depending on the bank or credit union and dealership, lenders might apply special rates at times to attract loans. It’s important to shop outside the dealership where you plan to purchase your vehicle to find possible attractive rates and terms.

The goal is to plan ahead. In doing so, you may be able to save on the interest rate and fees. Automobiles are considered a depreciating asset, meaning they lose value over time. If you have a loan with a high interest rate and you have a long-term plan to pay it off, you could pay over a third more for the vehicle with interest charges. Planning ahead to shop for the best loan and terms possible could save you thousands in interest over the life of the loan.

Eric Kirste, CFP®

Bank financing

How it works

With bank financing, you’ll apply with an auto lender, which could be a bank, credit union, or online lender, before visiting the dealership.

You’ll start by getting preapproved with multiple lenders to determine your eligibility and compare quotes. As with indirect financing, these direct loans are available to borrowers across the credit spectrum, but you may need to do extra work to find lenders willing to work with fair or poor credit.

You can expect the lender to need details about the car you’re looking to buy, but you can just state a desired loan amount if you don’t have the specifics yet. Once you’re preapproved, you can find a vehicle within your preapproved budget and negotiate a price with the dealer.

After you reach a deal at the dealership, the dealer will finalize the loan with the lender. At this point, you may need to provide the purchase agreement, along with proof of income, proof of residence, and other documentation. Review the final loan agreement before signing it to complete the process.

Be sure to consider credit unions. They’ve become an aggressive source for auto loans in recent years, according to clients and my own personal experience

Eric Kirste, CFP®

Pros and cons

Here’s a rundown of the benefits and downsides of bank financing.

Pros

-

Potentially lower interest rate

With a direct auto loan, your interest rate won’t include compensation for a dealer because you’re doing all the legwork.

-

More flexibility with your time

With many direct lenders offering an online experience, you can do it when it’s convenient for you. What’s more, you don’t need to worry about getting stuck at the dealership for hours.

-

Can help you stick to your budget

With your financing arranged, you don’t need to worry about a dealer trying to convince you to buy a more expensive vehicle or add on service and maintenance contracts you don’t need.

Cons

-

Can be time-consuming

It takes time to shop around and compare direct loan options on your own, especially if you’re new to the process, or your credit is less than stellar, meaning you have a limited selection of lenders.

-

A lower rate isn’t guaranteed

Depending on which lenders you and the dealer consider, you could get a better rate through the dealer. This is particularly true if you qualify for promotional financing on a new car through the manufacturer.

-

Potential delays

Some lenders won’t offer preapproval unless you have specifics on the model you want. If you want to visit dealerships first and then apply for a direct loan, the vehicle could be gone by the time you get preapproved.

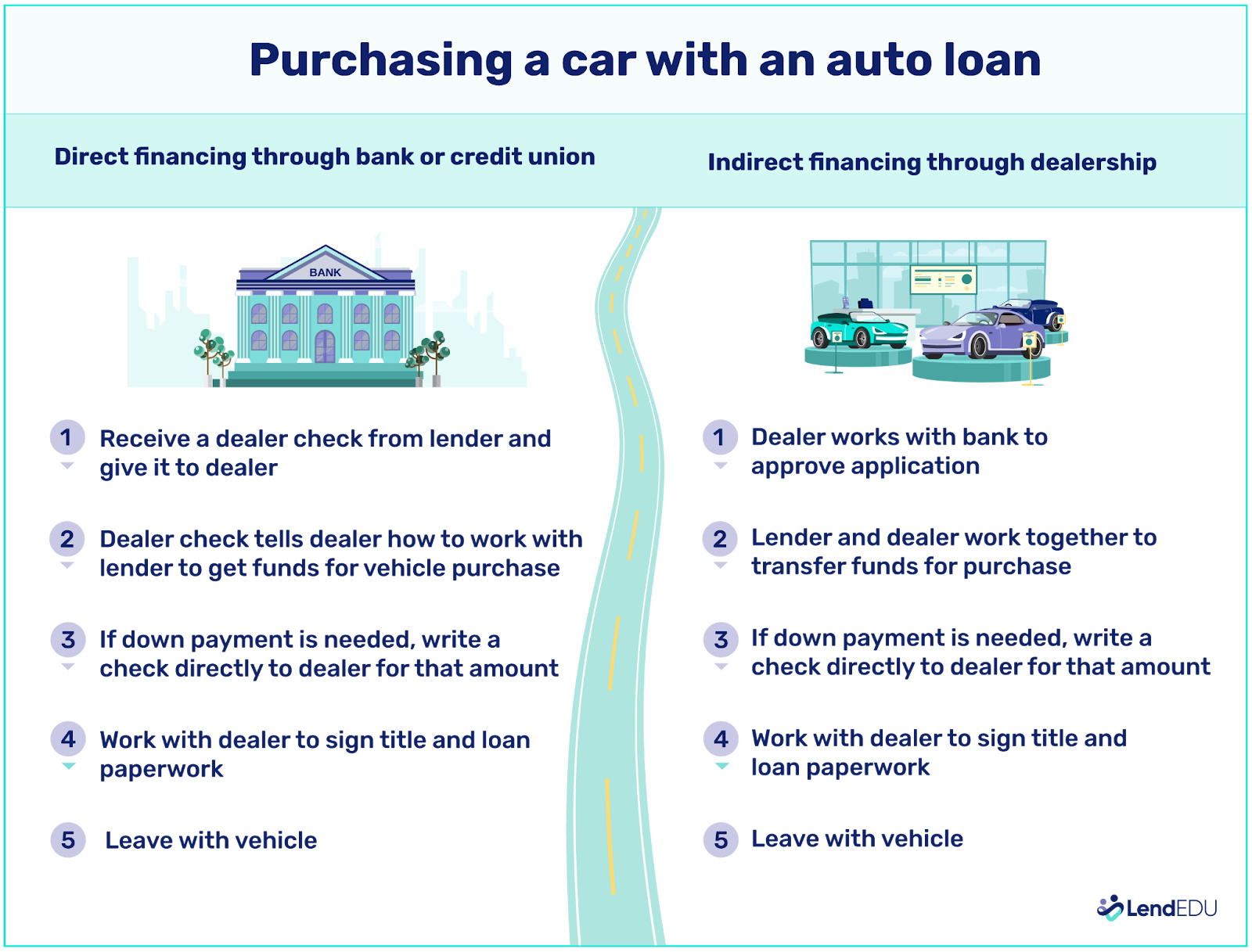

How does the purchase process work with car dealer financing vs. bank financing?

Your decision to apply for a direct loan or an indirect loan will influence your car-buying process. Here’s a quick summary of what to expect with both:

Bank financing

Once you’ve negotiated a price with the dealer, you’ll give the dealer a check or other documentation from the lender to finalize the loan and get payment for the vehicle. If you plan to make a down payment, you’ll provide that separately according to the dealer’s accepted payment methods.

That may include cash, a cashier’s check, a wire transfer, or sometimes a credit card. You’ll continue working with the dealer and the lender to provide any other necessary documentation and to complete the loan paperwork.

Dealer financing

Because dealer financing doesn’t require anything upfront, you’ll start the financing process after coming to an agreement on the sale price.

You’ll fill out an application, which the dealer will use to work with banks and other lenders. If the dealer comes back with an offer that you’re willing to accept, you’ll sign the loan documents and vehicle agreement. You may also need to provide additional documentation to complete the loan approval—but some lenders may reach out to obtain that later if you don’t have it on hand.

If you plan to make a down payment, you’ll do that using cash, a cashier’s check, a wire transfer, or a credit card in some cases.

Which financing method is right for you?

| Dealer financing might be better if… | Bank financing might be better if… |

| 🚗 You need a new car and don’t have time to shop around for an auto loan | 🏦 You want to avoid a higher interest rate that includes dealer compensation |

| 🚗 You’re uncomfortable shopping for a car loan on your own | 🏦 You don’t mind doing extra legwork |

| 🚗 You don’t want to limit yourself to select dealers | 🏦 You want to minimize the amount of time you spend at the dealership |

| 🚗 You can qualify for promotional financing on a new car | 🏦 You’re comfortable with shopping around on your own |

Several factors can influence your decision to get financing through a dealer or on your own.

- Convenience: With dealer-arranged financing, you don’t need to do any of the work involved with shopping around for a good deal. If you need a new car right away, dealer financing may be the only move.

- Interest savings: You can often get a lower interest rate with bank financing. The main exception is if you’re buying a new car and can qualify for promotional financing through the dealer.

- Flexibility: If you don’t mind working with select dealers in a lender’s network, bank financing may be more beneficial. But if you prefer the flexibility to work with any dealer, dealer financing might be better.

- Experience: If you feel comfortable shopping for an auto loan on your own, it can be worth the extra work. But if obtaining an auto loan on your own feels daunting, having the dealer take care of it might feel less stressful.

Before buying a car, consider these factors, along with your situation, needs, and preferences, to determine which loan type is right for you.

Check out our resource on the best auto loans:

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

Best for comparison shopping |

|

|

Best for no vehicle restrictions |

|

|

|

Best for lifetime financing |

|

|

Best for bad credit |

|

About our contributors

-

Written by Ben Luthi

Written by Ben LuthiBen Luthi is a Salt Lake City-based freelance writer who specializes in a variety of personal finance and travel topics. He worked in banking, auto financing, insurance, and financial planning before becoming a full-time writer.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Eric Kirste, CFP®

Reviewed by Eric Kirste, CFP®Eric Kirste, CFP®, CIMA®, AIF®, is a founding principal wealth manager for Savvy Wealth. Eric brings more than two decades of wealth management experience working with clients, families, and their businesses, and serving in different leadership capacities.