If you’re using a student loan to pay for college, it’s often considered a term loan that’s fully repaid in equal payments over time. As with any amortized term loan, the payment is designed to first cover interest, with the remainder applied to the loan balance.

This article will guide you through the amortization process and its impact on your loan balance. It will also explore options, including re-amortization and refinancing. Understanding these ideas allows you to manage your student loan debt more effectively and make informed financial decisions.

Table of Contents

What is student loan amortization?

Student loans are term loans (aka installment loans) repaid in equal amounts over a set period, known as the repayment term. The payments for these types of loans are calculated using amortization.

Amortization determines the fixed monthly payment needed to pay off a loan within a set time frame. In an amortized loan, each payment is divided into two parts: interest and principal.

It’s essential to understand how these two payment components work.

- Interest: The interest portion of your payment is the cost of borrowing money. Interest is calculated based on the loan’s interest rate and the remaining principal balance. You’ll repay any accrued interest in full each month—it isn’t added to your loan balance.

- Principal: The principal is the original student loan funds you borrowed. As you pay down the principal, the interest portion of each payment decreases, and more goes toward the principal.

As we noted, in the early stages of a term loan, a larger portion of each student loan payment goes toward interest. Over time, more of the payment is applied to the principal balance. This happens because you’re charged less interest as the balance decreases.

Assuming the interest rate is fixed, the monthly payment amount remains constant throughout the loan’s life. However, the allocation between interest and principal changes with each payment.

Are all student loans amortized?

Yes, all student loans are amortized because the goal is to repay the principal balance in full within a set term. Amortization is the tool used to accomplish this because it structures the repayment into equal installments that cover interest and principal.

However, not all student loans will carry the same payment throughout the loan’s life. While most student loans have a fixed rate and a payment that never changes, some have variable rates.

You might choose a fixed-rate versus a variable-rate loan for the following reasons:

- Fixed-rate student loans: Borrowers might choose a fixed rate for predictable monthly payments and stability in budgeting. Fixed rates protect against interest rate increases over time.

- Variable-rate student loans: Borrowers might select a variable rate for potentially lower initial interest rates compared to fixed rates. This can be helpful if you expect student loan interest rates to be reduced or stay the same.

Variable-rate loans adjust the interest rate periodically based on market conditions. When the rate changes, the allocation of each payment between interest and principal also changes.

Because amortization aims to ensure your loan is repaid in full by the end of the term, the amount that goes towards the principal balance won’t change if your interest rate changes. Instead, your monthly payment will increase or decrease to reflect the new interest charges.

This variability can affect your budgeting and the overall cost of the loan, making it essential to choose the right type of loan for your financial situation.

How does student loan amortization affect your balance?

Student loan amortization significantly impacts how your loan balance decreases over time. Amortization is the process of spreading out a student loan (or other installment loan) into a series of fixed payments over time.

Each payment consists of a principal portion and an interest portion. Early in the student loan’s term, a larger portion of the payment goes toward interest. As the loan progresses over time, more of the monthly student loan payment is applied to the principal balance.

Student loan amortization example

Let’s assume you have a student loan with a $20,000 balance, a fixed rate of 6%, and a 10-year repayment term. We’ll use an amortization schedule to break down the monthly payments and see how they change over time.

Details about your loan at your first and last monthly payments are shown in the following table:

| First monthly payment | Last monthly payment | |

| Monthly payment amount | $222.04 | $222.04 |

| Interest portion | $100.00 | $1.10 |

| Principal portion | $122.04 | $220.94 |

| Ending outstanding loan balance | $19,877.96 | $0 |

As you can see in the above table, the monthly payment never changes because you have a fixed interest rate. However, the amount of the payment that goes toward the principal reduces over time. After you make your last payment, you’ve paid the loan in full.

To further illustrate this concept, the following chart shows the total student loan payment and the amount allocated to interest and principal at each payment period. The payment always stays the same, you pay less interest each month.

By recognizing how your student loan payments are divided between interest and principal, you can decide whether to make additional payments to repay your loan faster (further reducing your interest costs) and consider refinancing options.

How to understand your amortization schedule

An amortization schedule is a detailed table that shows how each loan payment is applied to both the principal and interest over the life of the loan. This schedule helps you track your loan balance, understand how payments reduce your debt, and manage your financial planning effectively.

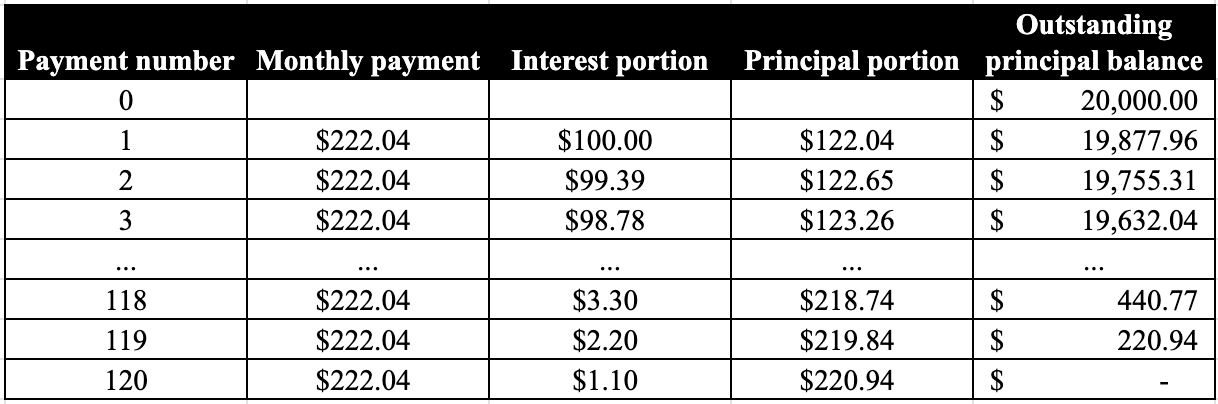

When you receive an amortization schedule from your lender, it typically includes columns for the payment number (or date), total monthly payment amount, interest portion, principal portion, and the remaining principal balance.

Here is an example based on a $20,000 loan with a 6% fixed interest rate over a 10-year term:

You can read your amortization schedule by understanding the following columns:

- Payment number: This column lists the sequence of payments from the first to the last.

- Monthly payment: This column shows the fixed total amount you will pay each month.

- Interest portion: This indicates the part of your payment applied to interest—you’ll pay all accrued interest each month.

- Principal portion: This shows the portion of your monthly student loan payment that goes toward the principal balance.

- Outstanding principal balance: This column tracks the remaining balance of your loan after each payment.

Reviewing your amortization schedule can help you see how each payment will affect your loan balance.

Can student loans be re-amortized?

In general, loans are re-amortized when there’s a need to create a new repayment schedule for a loan without refinancing. You might see this happen when there’s a large charge to the loan balance. Some—but not all—student loan lenders allow re-amortization.

Re-amortization aims to reset the monthly payments and amortization so they align with the new balance. For instance, if you make a large extra payment on your student loan, you’ll repay the loan faster than expected because the amortization is based on a larger principal balance.

Repaying your loan faster can lower your overall interest costs. However, if you need a lower payment, loan re-amortization can be a way to lower your monthly payment and repay the loan in the original time frame without needing to refinance.

Re-amortization might also be used if you missed payments and the lender agrees to add them and any accrued interest to the balance of your loan. In this case, the goal is to ensure your loan is repaid in full at the end of the original term.

If your lender won’t re-amortize your student loan, other options include the following:

- Loan consolidation: This is a way to combine multiple federal student loans into a new single federal loan repayment term and recalculate payments. It effectively re-amortizes the loan by spreading the balance over a new period.

- Loan refinancing: This involves getting a new private student loan with different terms, such as a lower interest rate or a different repayment period. This results in a new amortization schedule, recalculating the payments based on the new loan terms.

- Income-driven repayment plans: These federal student loan plans set your payments based on your income and family size. While not traditional re-amortization, they alter the repayment schedule and payment amounts, extending the loan term and changing the amortization process.

You should choose the best method for your financial situation. Even if your lender won’t re-amortize your student loan, you might consider several other options.

About our contributors

-

Written by Megan Hanna, CFE, MBA, DBA

Written by Megan Hanna, CFE, MBA, DBADr. Megan Hanna is a finance writer with more than 20 years of experience in finance, accounting, and banking. She spent 13 years in commercial banking in roles of increasing responsibility related to lending. She also teaches college classes about finance and accounting.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.