Tax debt is what you owe the IRS if you don’t pay in full when you file your return. The IRS and state government both expect you to make a plan to pay your debt promptly. If you don’t pay, the balance will continue to grow due to interest and penalties. You can also face wage garnishment and liens.

But tax debt forgiveness can help if you can’t afford to pay the debt or don’t think you should have to. When you qualify for tax debt forgiveness programs, the IRS forgives some or all of your balance. States have different tax laws and processes for collecting what you owe. Some states offer tax debt forgiveness, but not all of them.

The exact amount of forgiveness depends on the program and your circumstances. Some of the most popular options include Offers in Compromise, Currently Not Collectible status, and innocent spouse relief. We’ll cover the main four forgiveness options available to taxpayers in 2025 here.

Table of Contents

- 1. Offer in Compromise (OIC)

- 2. Currently Not Collectible (CNC) status

- 3. Innocent spouse relief

- 4. State tax debt forgiveness

- FAQ

- What do the forms look like?

- What are the pros and cons?

- How long does it take to get approved?

- Is forgiveness taxable income?

- Do I need a tax attorney?

- What happens if I default?

- Can I negotiate directly?

- Is there tax debt forgiveness for businesses?

- Does applying affect my credit score?

- Can interest and penalties be forgiven too?

1. Offer in Compromise

Type: Federal

Taxpayers can attempt to make an Offer in Compromise when they can’t afford to pay their entire tax bill. Instead, they work with the IRS to make an offer—a fraction of what they owe—and if the IRS accepts, the tax debt is considered settled.

Don’t get too excited about paying pennies on the dollar with the IRS. Statistically speaking, fewer than half of applications for an Offer in Compromise get accepted.

How to apply

The application process includes multiple steps, but it’s a straightforward process. Here’s how to apply.

- Confirm that you qualify: Use the IRS’s Offer in Compromise pre-qualifier tool to understand whether you qualify. While there’s no set-in-stone rule about who qualifies, you must demonstrate genuine financial hardship, which usually includes minimal income with significant monthly expenses.

- Determine what you can afford: When you apply, determine how much you’re willing and able to pay. The IRS will review your income and assets and determine whether the amount you offer is satisfactory based on your documented financial hardship.

- Complete the application: As part of the application process, you’ll fill out Form 656, which includes Form 433-A. Businesses will fill out Form 433-B.

- Pay the fee: The IRS charges a $205 application fee. But if you meet low-income certification guidelines, you won’t need to pay.

2. Currently Not Collectible (CNC) status

Type: Federal

If you can’t afford to pay your taxes, you can apply for Currently Not Collectible (CNC) status. If approved, the IRS can’t require you to pay your tax debt—for now.

The IRS will continue to monitor your financial situation. If, at any point, the organization determines that your situation has changed, you may be required to start paying your debt. Your tax debt will continue to accrue interest and late payment penalties while you have CNC status.

The IRS has a 10-year statute of limitations to collect tax debts. If you remain within CNC status for 10 years, the 10-year-old tax debt will disappear.

How to apply

You must complete the application process to apply for CNC status. If you have questions, contact the Taxpayer Advocate Service for free assistance. Here’s how to file.

- Complete the forms: You must file multiple application forms, including Form 433-A or Form 433-B and Form 433-F.

- Submit proof: Demonstrate financial hardship by providing information about your income, assets, and necessary monthly expenses.

- File tax returns: Make sure your tax returns are current, even if you can’t afford to pay. The IRS will continue to monitor your financial situation while you have CNC status.

Whether you get approved for an Offer in Compromise or Currently Not Collectible status depends on your financial condition—it is not an either-or. The IRS will not put someone in CNC if it determines the debtor has the means to make payments.

3. Innocent spouse relief

Type: Federal

The IRS may also offer tax relief if you filed jointly with a spouse and didn’t know your former spouse made errors with the tax return. Eligibility for innocent spouse relief is tough; you need to prove you truly had no knowledge of the errors.

How to apply

You must complete the IRS application when you request innocent spouse relief. Like other types of tax debt forgiveness, innocent spouse relief is a long process that takes time. Here’s how to get started.

- Complete the form: If you believe you qualify for relief, file Form 8857.

- File your taxes: Once you file the form, you must continue to file tax returns and pay your taxes. Stay up to date on current taxes to avoid additional penalties and interest.

- Wait for the decision: The IRS will contact your spouse or former spouse for additional information. It can take up to six months to get a decision letter. Once you receive it, you can appeal the decision if you disagree.

4. State tax debt forgiveness

Type: State

Because each state sets its own tax laws, your path to state tax debt forgiveness will depend on where you live. Rather than work with the IRS, you’ll try to establish a payment with your state comptroller.

Every state offers some form of tax debt forgiveness, but some are more generous than others. You can typically apply for an Offer in Compromise or defer payments due to financial hardship.

Here are helpful tax debt forgiveness links for your state, if applicable.

| State | Does the state offer forgiveness? | Income tax resource |

| Alabama | Yes | Alabama tax relief |

| Alaska | No state income tax | No state income taxes |

| Arizona | Yes | Arizona taxes |

| Arkansas | Yes | Arkansas tax relief |

| California | Yes | California tax relief |

| Colorado | Yes | Colorado tax relief |

| Connecticut | Yes | Connecticut taxes |

| Delaware | Yes | Delaware taxes |

| Florida | No state income tax | No state income taxes |

| Georgia | Yes | Georgia tax relief |

| Hawaii | Yes | Hawaii tax relief |

| Idaho | Yes | Idaho taxes |

| Illinois | Yes | Illinois taxes |

| Indiana | Yes | Indiana taxes |

| Iowa | Yes | Iowa tax relief |

| Kansas | Yes | Kansas tax relief |

| Kentucky | Yes | Kentucky tax relief |

| Louisiana | Yes | Louisiana tax relief |

| Maine | Yes | Maine tax relief |

| Maryland | Yes | Maryland taxes |

| Massachusetts | Yes | Massachusetts tax relief |

| Michigan | Yes | Michigan tax relief |

| Minnesota | Yes | Minnesota tax relief |

| Mississippi | Yes | Mississippi taxes |

| Missouri | Yes | Missouri tax relief |

| Montana | No | Montana taxes |

| Nebraska | Yes | Nebraska taxes |

| Nevada | No state income tax | No state income tax |

| New Hampshire | No state income tax | No state income tax on wages and salary |

| New Jersey | Yes | New Jersey taxes |

| New Mexico | Yes | New Mexico taxes |

| New York | Yes | New York tax relief |

| North Carolina | Yes | North Carolina tax relief |

| North Dakota | Yes | North Dakota taxes |

| Ohio | Yes | Ohio tax relief |

| Oklahoma | Yes | Oklahoma taxes |

| Oregon | Yes | Oregon tax relief |

| Pennsylvania | Yes | Pennsylvania tax relief |

| Rhode Island | Yes | Rhode Island taxes |

| South Carolina | Yes | South Carolina taxes |

| South Dakota | No state income tax | No state income tax |

| Tennessee | No state income tax | No state income tax |

| Texas | No state income tax | No state income tax |

| Utah | Yes | Utah tax relief |

| Vermont | Yes | Vermont taxes |

| Virginia | Yes | Virginia tax relief |

| Washington | No state income tax | No state income tax |

| Washington, D.C. | Yes | Washington, D.C. taxes |

| West Virginia | Yes | West Virginia tax relief |

| Wisconsin | Yes | Wisconsin tax relief |

| Wyoming | No state income tax | No state income tax |

FAQ

What do tax debt forgiveness forms look like?

CNC requests and OIC applications have the same application forms, but the innocent spouse relief form is separate. You can fill out the application yourself, but you might be better off working with a tax relief company. The forms are long and complicated—and you’ll need to know what other paperwork to gather.

As an example, let’s look at the Offer in Compromise process. For an Offer in Compromise, you’ll fill out Form 656 booklet, which contains Form 433-A (for individuals) and Form 433-B (for businesses). Before you can apply, you must file all tax returns you’re legally required to file.

The form is lengthy and requires detailed information, including:

- Personal and household information

- Employment information

- Personal asset information

- Self-employment information

- Business asset information

- Business income and expense information

- Monthly household income and expense information

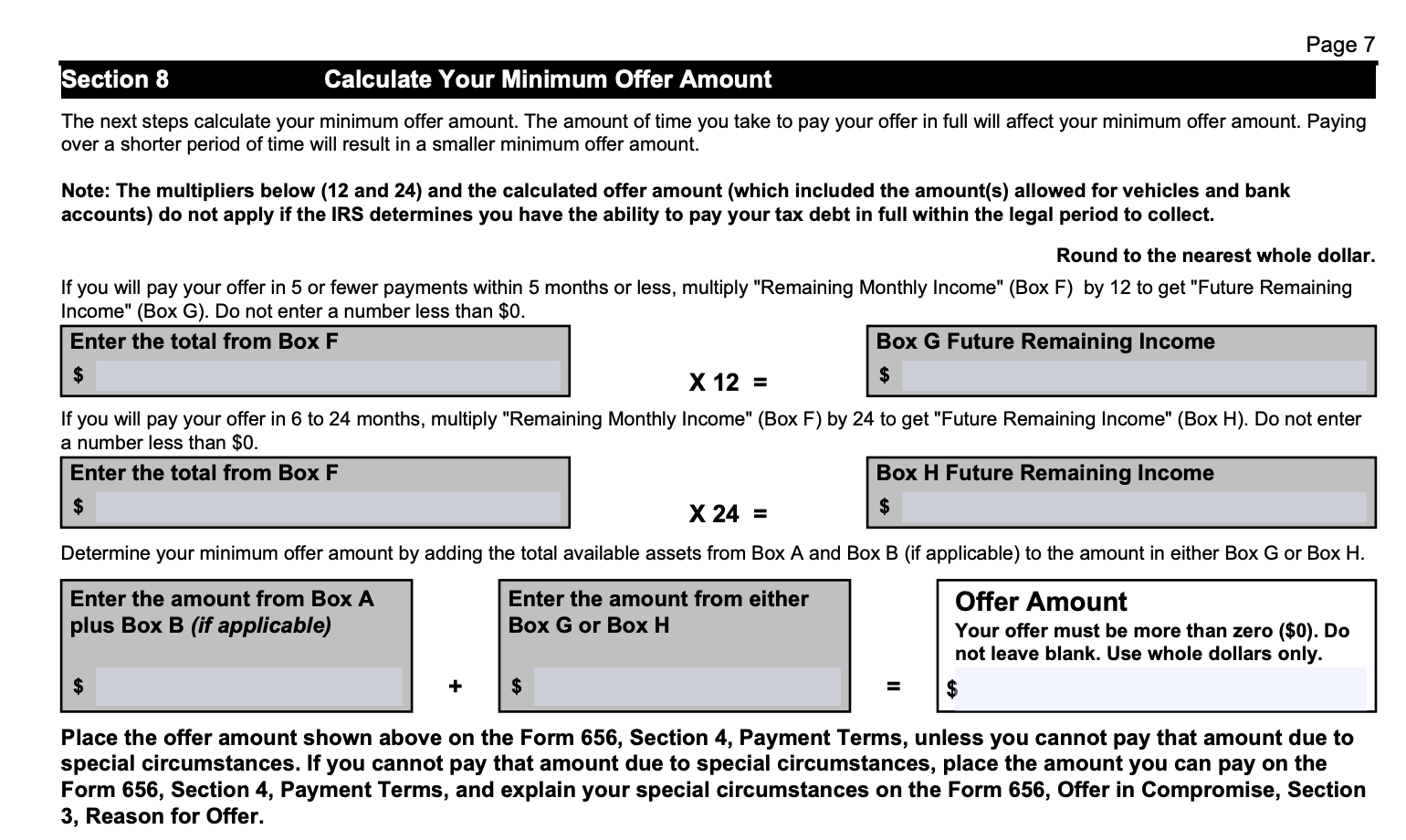

You’ll calculate your minimum offer amount while filling out this form. Here’s what it looks like:

Tax debt forgiveness applications and forms can be handled on your own as the taxpayer, but getting a tax professional likely reduces errors.

What are the pros and cons of tax debt forgiveness?

When you can’t afford to pay your tax debt, it’s hard to imagine any cons to seeking out debt forgiveness. But here are several pros and cons to weigh.

Pros

-

Get immediate relief

You can settle for a lower amount you can manage (Offer in Compromise) or buy time until you can pay your debt (CNC).

-

Avoid other debt

Alternatives to tax debt forgiveness could entail taking on high-interest debt that’s worse than the penalties and interest you’ll owe the IRS.

-

Avoid wage garnishments and asset liens

If you fail to pay the IRS what you owe and don’t establish relief through one of its programs, the IRS can start to garnish your wages and place liens on your property.

Cons

-

Not guaranteed

You can apply for tax debt forgiveness, but you’re not guaranteed approval. In some cases, you might pay application fees for nothing.

-

Significant work

The application process is complex and full of paperwork. You may need to hire a tax professional to help you through it.

-

Impact on credit and finances

CNC status can lead to a drop in your credit score, and you’ll likely have to pay the debt eventually—just with interest and penalties accrued.

-

Taxability

Debt forgiveness—including tax debt forgiveness—may be considered taxable income for federal income tax purposes.

How long does it take to get approved for a tax debt forgiveness program?

How long it takes to get approved for a tax debt forgiveness program depends on which you apply for. It might take the IRS six months to a year to approve an OIC.

CNC applications are variable, and states have their own processes—with their own timelines—when seeking state tax forgiveness.

Is tax debt forgiveness considered taxable income?

Forgiven debt through an Offer in Compromise is not considered a taxable event. You won’t need to pay taxes on the amount your current tax debt is reduced by.

Do I need a tax attorney to apply for a tax debt forgiveness program?

You don’t legally need a tax attorney to apply for a tax debt forgiveness program, but it can certainly help. The programs are complicated, and the forms can get confusing. Working with a professional might improve your chances of qualifying.

What happens if I default on a tax forgiveness agreement?

If you default on a tax forgiveness agreement (Offer in Compromise), the IRS can attempt to collect the entire amount you originally owed (minus anything you’ve paid). It will also reinstate penalties and interest and can place a lien on the account. In short, whatever you do, don’t default on a tax forgiveness agreement.

Can I negotiate directly with the IRS or state taxation agency?

An Offer in Compromise is your way to negotiate with the IRS and your state’s taxation agency if your state offers it. Most applications for Offers in Compromise are rejected, so be strategic about when you apply and how much you offer to pay.

Are there special debt forgiveness programs for businesses?

The IRS and several states offer debt forgiveness programs for businesses and self-employed individuals. For instance, businesses can apply for an Offer in Compromise through the IRS.

Does applying for a tax debt forgiveness program affect my credit score?

Applying for tax debt forgiveness does not affect your credit score, but getting approved might. Offers in Compromise don’t affect your credit, but currently not collectible status can lower your score—if you owe the IRS more than $10,000 and the organization files a Notice of Federal Tax Lien.

Can interest and penalties be forgiven along with the principal debt?

When you negotiate an Offer in Compromise, you agree to a dollar amount you’ll pay to consider yourself debt-free, including interest and penalties. However, if you get CNC status with the IRS, late penalties and interest will continue to accrue.

About our contributors

-

Written by Taylor Milam-Samuel

Written by Taylor Milam-SamuelTaylor Milam-Samuel is a personal finance writer and credentialed educator who is passionate about helping people take control of their finances and create a life they love. When she's not researching financial terms and conditions, she can be found in the classroom teaching.