It’s easier than you might think to fall behind on taxes.

Maybe an unexpected expense drained your savings, paperwork got lost, or tax laws changed, and you didn’t realize how much you owed.

Whatever the reason, a tax bill can quickly become a bigger problem—especially when penalties and interest start adding up.

If your balance reaches $50,000 or more, the IRS may start serious collection efforts, like placing a lien on your property, garnishing wages, or levying your bank account.

Sounds intimidating, but pause and take a deep breath here. Taking action now can make a big difference, and we’ll help you understand your choices and how to move forward.

Table of Contents

The IRS collection process for balances above $50,000

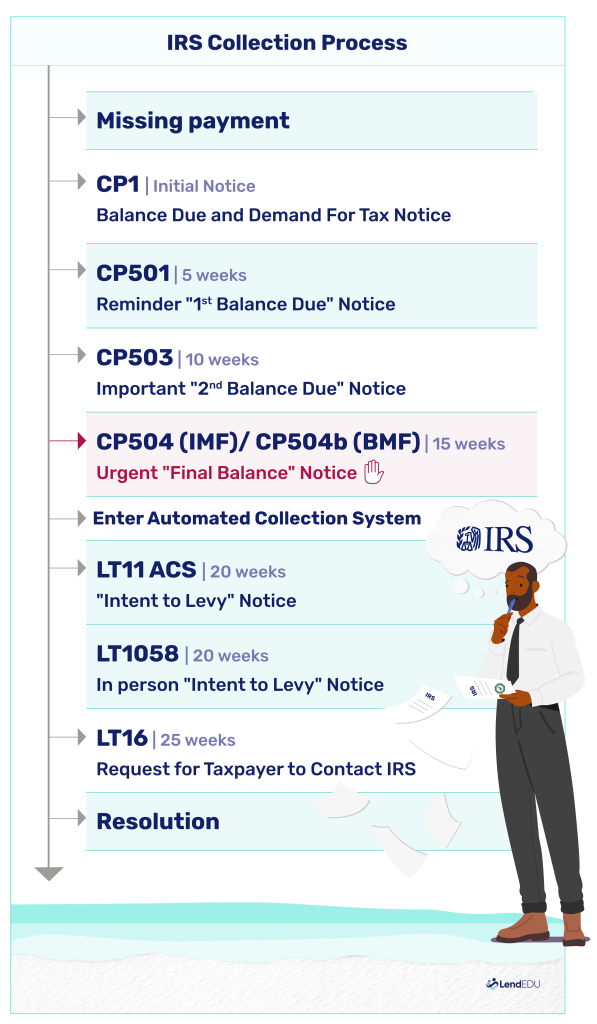

If you owe taxes and don’t pay in full when you file, the IRS follows a step-by-step process to collect what’s due. Here’s what to expect if collections hit you, no matter how much you owe:

- You get a bill from the IRS. The IRS sends a CP14 Notice, which is your first official bill. It explains how much you owe, including interest and penalties, and requests payment in full.

- If you don’t pay, the reminders start. Next, you’ll receive a CP501 Notice, which is a follow-up reminder. If that’s ignored, the IRS sends a stronger warning in CP503 Notice. The next notice is CP504, which means the IRS is preparing to take action.

- The IRS may file a tax lien. If your balance remains unpaid, the IRS can place a federal tax lien on your property. This is a public record that can make it harder to sell assets or get approved for loans.

- The IRS can levy your wages or bank account. If the debt still isn’t addressed, the IRS can seize funds directly from your paycheck, bank account, or other assets through a tax levy.

- The collection process continues until the debt is resolved. The IRS will keep pursuing collection until your tax debt is paid in full, settled, or no longer legally collectible. You can stop collection efforts by setting up a payment plan, applying for an Offer in Compromise (OIC), or qualifying for Currently Not Collectible status. But don’t put it off—the sooner you act, the more options you’ll have.

What’s different about owing $50,000 or more in back taxes

When dealing with IRS tax debt, the amount you owe has a direct impact on your repayment options:

- Owing $25,000 or less: You can qualify for a streamlined installment agreement. $25,000 is also an important threshold when it comes to tax liens; if you owe $25,000 or less, you can ask to have federal tax liens withdrawn after making three consecutive payments through a Direct Debit Installment Agreement.

- Owing between $25,001 and $50,000: You’re still eligible for a streamlined installment agreement, but the IRS requires you to either pay your debt down to $25,000 first or agree to make payments through direct debit or payroll deduction.

- Owing more than $50,000: It’s still possible to qualify for an installment agreement, but you’ll need to submit a Collection Information Statement (Form 433-A), which details your income, expenses, and assets.

If the size of the debt is unmanageable, you could apply for an OIC. Formerly known as the Fresh Start program, an OIC allows you to settle your tax debt for less than you actually owe.

If your tax bill comes as a surprise, it can strain your cash flow and potentially lead to increased debt unless you arrange a payment plan with the IRS—a step I highly recommend. Insufficient tax withholding throughout the year not only results in a tax liability but also incurs penalties for late or insufficient payments. These penalties represent missed opportunities, as the funds could have been more effectively allocated toward savings or investments.

What happens if you owe the IRS $50,000 or more?

Owing the IRS a large tax debt isn’t just about having a balance—it comes with immediate financial consequences.

From added costs to collection actions, the longer the debt goes unpaid, the more complicated things get. Here’s a closer look at what can happen when you owe $50,000 or more.

Interest

Unfortunately, you don’t just have to worry about paying your original tax balance; penalties and daily compounding interest make it grow fast.

Interest compounds every day, meaning each day’s interest is added to your total balance, and the next day, interest is charged on that slightly higher amount. Over time, this snowballs, making even a moderate tax debt much larger.

Penalties

On top of that, late payment penalties can reach up to 25% of your unpaid tax, adding even more to what you owe. The larger your balance, the faster these extra costs add up, making it harder to pay off over time.

Liens

Owing a large tax debt can impact your credit and overall financial life, especially if the IRS files a federal tax lien.

While tax liens no longer appear on credit reports, they are public records, meaning lenders can still find them when reviewing loan applications. This can make it harder to qualify for a mortgage, refinance, or other types of financing.

If a tax lien prevents you from purchasing or refinancing a home, you can apply for a lien subordination—this doesn’t remove the lien. Still, it lets other creditors take priority, which could improve your chances of loan approval.

The good news is that you can have the lien removed easily enough. The most straightforward way to remove a tax lien is to pay your full balance, at which point the IRS will typically release the lien within 30 days. Or, if you’re on a payment plan and meet the eligibility requirements—making on-time payments and having no default history—the IRS may withdraw the lien, removing it from public records.

Wage garnishment

When tax debt goes unpaid for too long, the IRS can and will take action to collect; if you continue to ignore notices and warning letters, the agency could start garnishing your wages.

Wage garnishment means the IRS takes money directly from your paycheck before it ever reaches your bank account. This continues until the debt is paid or a payment agreement is made.

If garnishing wages isn’t enough, the IRS can also seize assets, including bank accounts, property, or even business assets. These actions don’t happen overnight, but it can be hard to stop once the process starts.

Asset seizure

Asset or property seizure is one of the most severe actions the IRS can take, but it’s relatively rare and typically occurs only after other collection methods (e.g., wage garnishments or bank levies) have been exhausted. If you’re working with the IRS—making payments, setting up an installment agreement, or pursuing another formal resolution—it’s much less likely to resort to seizing your home or car.

However, the IRS has the legal authority to seize property if you ignore multiple notices and fail to arrange a payment plan. To avoid this worst-case scenario, stay in communication with the IRS or consult a tax professional at the earliest sign of trouble.

Tax refund offsets

If you owe the IRS money, you won’t get a tax refund—it’ll go toward your debt instead. This is called a tax refund offset, and it happens automatically when you have an outstanding balance with the IRS. Instead of issuing your refund, the IRS applies it to your unpaid taxes to reduce what you owe.

If you filed a joint return but the tax debt belongs only to your spouse, you may be able to get your portion of the refund back by completing an Injured Spouse Allocation (Form 8379). This allows the IRS to separate your share of the refund from the debt owed by your spouse

IRS payment plans for $50,000 or more

There are several ways to manage or reduce tax debt, but navigating these options—and getting approved—can be complicated once balances are higher.

This is a situation where we recommend exploring tax relief. Tax relief companies can work directly with the IRS on your behalf to resolve your tax debt. If you owe $50,000, or more, professional help could ensure you’re choosing the best option and improve your chances of relief approval.

One of the best tax relief companies we’ve come across for handling high balances is Anthem Tax Services. Unlike some firms, Anthem employs licensed tax professionals who can represent you before the IRS to negotiate payment plans, penalty reductions, and settlement options like Offers in Compromise.

But whether you work with a tax relief company or handle it yourself, understanding the various IRS relief programs is the first step toward getting help. Let’s take a closer look at these options below.

Installment agreements above $50,000

Best for: When you can’t pay your full balance at once but can make monthly payments over time.

Next steps: To request an installment agreement over $50,000, you’ll need to submit a Collection Information Statement, typically Form 433-A, along with Form 9465 to formally apply.

An IRS installment agreement lets you pay your tax debt in manageable monthly payments instead of a lump sum.

If you owe $50,000 or less, you may qualify for a streamlined installment agreement, which doesn’t require extensive paperwork. For larger balances, you can still get a payment plan with the IRS, but the agency will likely require detailed financial disclosures before your application is approved.

Offer in Compromise above $50,000

Best for: Taxpayers who can’t afford to pay their full tax debt and may qualify to settle for less than they owe.

Next steps: Apply for an Offer in Compromise by submitting the Form 656 Booklet, which includes Form 433-A (OIC) or Form 433-B (OIC) for businesses.

An OIC allows you to negotiate with the IRS to reduce your total tax debt if paying in full would create financial hardship. The IRS considers income, expenses, assets, and ability to pay when deciding whether to accept an offer.

If approved, you’ll settle your debt for a lower amount than what you owe, either through a lump sum or monthly payments. Not everyone qualifies, and the application process can be complex, but for those who do qualify, it can provide significant relief.

Currently Not Collectible (CNC) status above $50,000

Best for: Taxpayers who can’t afford to pay anything toward their tax debt without causing financial hardship.

Next steps: Submit Form 433-A or Form 433-F, depending on your employment status, to request CNC status.

If you genuinely can’t pay any amount toward your tax debt—whether you owe the IRS $25,000, $50,000, or more—you may qualify for CNC status. This can give you breathing room to stabilize your finances without the immediate threat of levies or garnishments.

However, being granted CNC status usually requires a thorough review of your financial situation, including income, expenses, and assets. You’ll need to prove to the IRS that paying any amount toward your tax debt would cause undue financial hardship. While in CNC, interest and penalties will still accrue, so it’s best to explore longer-term solutions—such as an installment agreement or Offer in Compromise—as your finances improve.

CNC status isn’t permanent either—the IRS will review your financial situation periodically, and if it improves, collection efforts may resume.

Penalty abatement above $50,000

Best for: Taxpayers who owe IRS penalties due to reasonable cause or first-time mistakes and want to reduce extra charges.

Next steps: Use Form 843 to request abatement for penalties due to reasonable cause. For First-Time Abatement, call the IRS or send a written request.

The IRS may remove or reduce penalties through penalty abatement, which can lower what you owe. There are a few ways to qualify:

- First-Time Penalty Abatement: Available if you have a clean compliance history, it’s your first penalty, and the penalty is either Failure to File, Failure to Pay, or Failure to Deposit.

- Reasonable Cause Relief: If circumstances beyond your control (e.g., illness, natural disaster) caused the issue.

- Statutory Exceptions: For penalties applied in error.

If a penalty is reduced or removed, the IRS will automatically adjust the related interest, lowering the total amount owed.

If your tax situation is relatively simple, you can avoid underpaying by researching and updating your W-4 at the start of the year to align with any new tax changes. For those who are unsure about making these adjustments, free tax preparation services are available through the Volunteer Income Tax Assistance (VITA) program, which can be found in local communities and searched online at IRS Free Tax Prep.

Owing the IRS certainly isn’t ideal, but it’s something you can get through—and with the right approach, you can keep it from happening again.

Setting aside money for taxes throughout the year can make a huge difference, even if it’s a little at a time. Be sure to check your IRS account regularly so you’re never caught off guard by a balance or deadline.

If paying your tax debt in full isn’t an option, don’t wait to explore solutions—installment agreements, an Offer in Compromise, and other programs can help. And if the IRS sends you a notice, open it immediately and deal with it—things are much easier to handle when you take action early.

No matter how big your tax debt feels, there’s always a way forward. The key is to take it one step at a time. Here’s a recap of the next steps you need to take.

Step-by-step action plan for $50,000 balances

Tackling a large tax debt can feel daunting, but it helps if you break the process down into manageable steps:.

- Step 1: Assess your situation: Check your IRS notices and log into your IRS online account to see exactly how much you owe, including interest and penalties.

- Step 2: Consult a tax professional: A tax pro can help you understand your options and figure out the best way to handle your debt. If you can’t afford one, turn to your local Low Income Taxpayer Clinic for help.

- Step 3: Choose your resolution path: Decide whether you’ll set up a payment plan, apply for penalty relief, explore an Offer in Compromise, or request uncollectable status to help resolve your tax debt.

- Step 4: Submit your application: If you’re setting up an installment agreement or requesting relief, fill out the required form, gather the necessary documents, and file them with the IRS.

- Step 5: Stay compliant: Once you’re on a repayment plan (or have settled your debt), keep up with future tax filings and payments to avoid new issues.

For individuals with more complex tax situations—such as self-employed professionals, contract workers, or real estate investors, complicated investments such as stock options—I strongly recommend consulting a Certified Public Accountant (CPA). Since CPAs’ client lists fill up quickly, it’s best to start your search as soon as possible to ensure you receive expert guidance in a timely manner.

Generally, the IRS has 10 years from when your tax was assessed to collect on a balance due. This 10-year window, known as the Collection Statute Expiration Date (CSED), can be extended under certain circumstances—such as if you file for bankruptcy, leave the country for an extended period, or enter into an OiC.

So, the bottom line is: Don’t wait. Take control of your tax balance today and give yourself some financial peace of mind.

About our contributors

-

Written by Christi Gorbett

Written by Christi GorbettChristi Gorbett is a finance writer with a master’s degree in English and years of experience. She specializes in creating financial content that simplifies complex topics, making them easier for a wide audience to understand.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.