It’s been two months since President Trump declared a national emergency, and the coronavirus pandemic continues to wreak unimaginable havoc.

During this time, LendEDU has been publishing the findings of our surveys of adult Americans gauging how the virus is impacting finances; the first survey was conducted on March 18, while the second was run on April 1.

We conducted our third survey on May 5, and the findings include steadily mounting expenses and less concern over retirement savings likely due to a stock market surge from March lows.

We also found many Americans are still waiting on their stimulus checks, in addition to unemployment benefits if they have been laid off.

Click here to jump to the full survey results

If you would like to see a specific breakdown of the data other than those provided (ex. state-by-state, gender, age, employment status), or a full survey-to-survey-to-survey comparison, please email me at [email protected].

Observations & Analysis

All data is based on an online survey of 1,000 adult Americans commissioned by LendEDU and conducted by survey platform Pollfish. The survey was conducted on May 5, 2020. For some questions, the answer percentages may not add up to 100% exactly due to rounding.

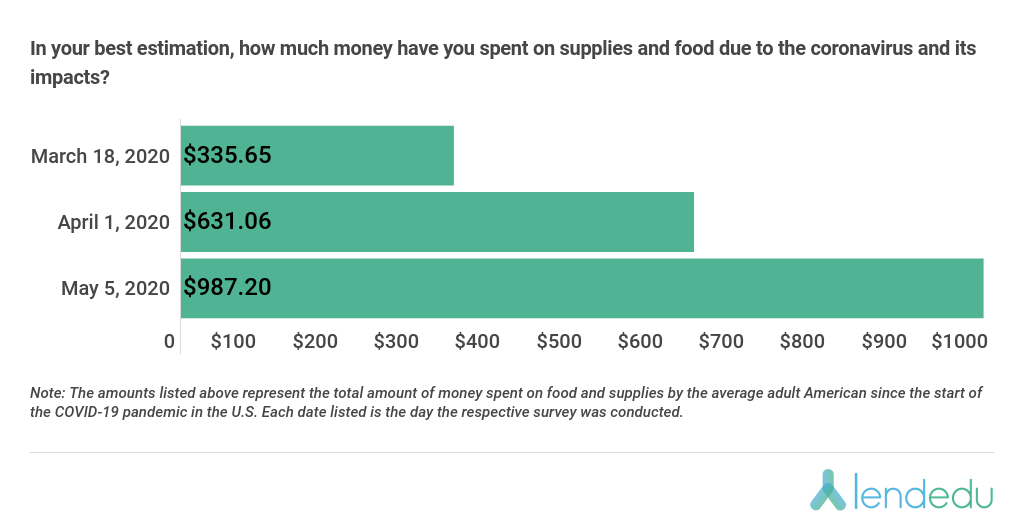

Expenses Continue to Mount, Up 194% From First Survey

Pandemic preparation is not cheap as consumers want to hoard food and supplies in fear of a store running out of product. Additionally, shoppers today are trying to make as few trips as possible to limit their chances of contracting COVID-19.

Not surprisingly, we have seen a steady increase in expenses as the pandemic has continued; since the start of the U.S. outbreak in mid-March, the average American has spent nearly $1,000 on food and supplies.

From our second survey over a month ago, there has been a 56% increase in coronavirus-related expenses like food and supplies. From the first survey in mid-March there has been a 194% increase.

With the economy on a downturn and unemployment rising sharply, budgeting for these expenses becomes increasingly difficult. This is especially true for Americans who have yet to receive stimulus checks or unemployment benefits, and our survey found that a considerable number of folks fall into this category.

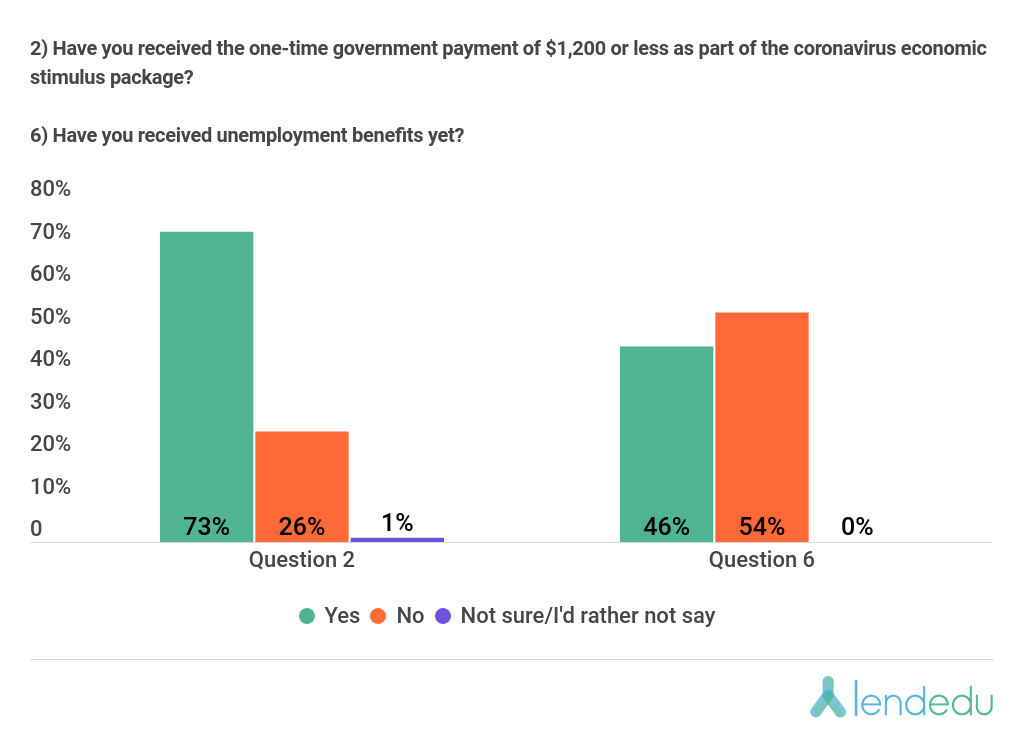

Many Americans Still Waiting on Stimulus Checks, Unemployment Benefits

One of the pillars of the CARES Act is the stimulus check program that has been sending one-time government payments up to $1,200 to tens of millions of qualifying Americans.

The rollout of such a massive program on short notice has had its understandable bumps in the road, and millions of potentially cash-strapped Americans have yet to receive their payments.

In that same vein, a record number of people filing for unemployment benefits has flooded the system for states and caused delays. For example, the unemployment sites for both New York and New Jersey have crashed recently.

Our survey found that 26% of eligible Americans are still waiting on their stimulus checks, while 54% of those that have filed for unemployment benefits have yet to receive them. And for these groups, especially the latter, the financial situation is getting desperate.

While the need for funds isn’t quite as dire for those who have yet to receive a stimulus check, it is still greater than the average American. The truly desperate need for cash is amongst those who have been laid off and still haven’t received unemployment benefits, as 86% of this cohort are worried about running out of money in their accounts.

Additionally, these two groups of respondents that are still waiting for government assistance are also more worried than the normal respondent when it comes to meeting mortgage, student loan, or credit card payments when we segmented the results to questions 15, 17, and 19 respectively.

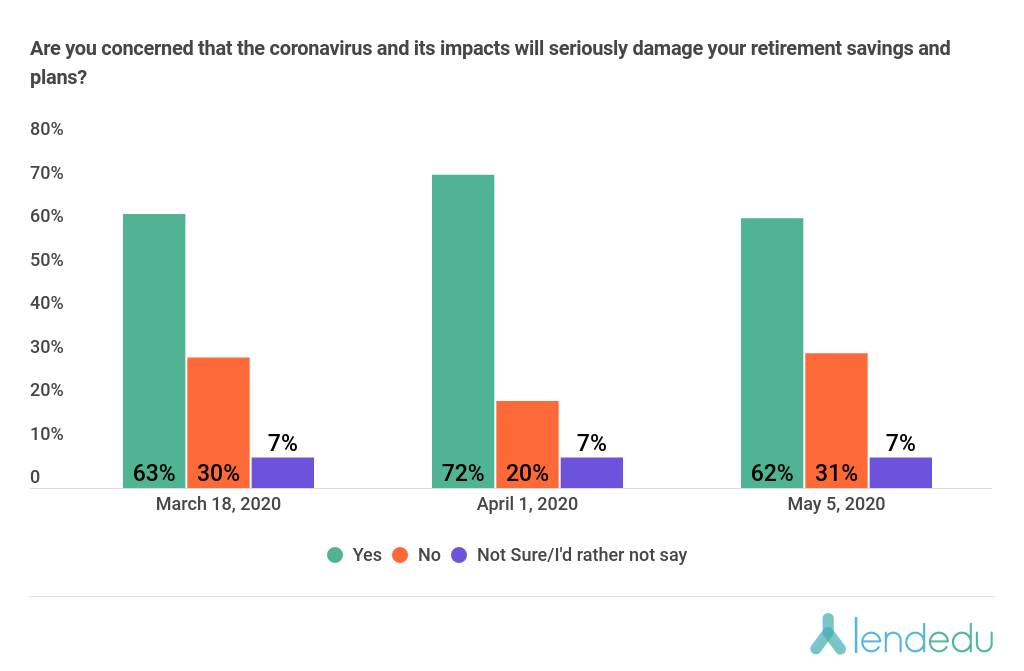

As Stock Market Goes Up, Fears Over Retirement Savings Go Down

Overall, the stock market has tumbled during the coronavirus pandemic. From survey one to survey two, there was an increasing concern amongst poll participants when it came to their retirement nest eggs.

Yet still, the market has actually performed consistently well over the last month with both the S&P 500 and Dow Jones up since early April. Expectedly, this welcomed reversal seems to have quelled some retirement worries.

We also found that amongst respondents that have been actively involved in the stock market through a personal brokerage account since the pandemic hit home in the U.S., more have been making money lately.

On March 18, only 8% of this group had netted a profit and on April 1, it was 10%. But in this most recent survey, the percentage of Americans that have made money since the beginning of the outbreak through more-personal investing jumped to 21%.

The recent market upswing could help explain why fewer respondents from the May 5 survey are worried about making monthly mortgage, student loan, or credit card payments.

With that being said, the recent drops could also be attributed to the number of financial institutions that are relaxing repayment policies for struggling borrowers, in addition to recent student loan changes that have placed all federal student loans in pandemic forbearance until September 30, 2020.

>>Read More: Before Coronavirus Relief Came, 68% of Student Loan Borrowers Were Worried About Making Payments

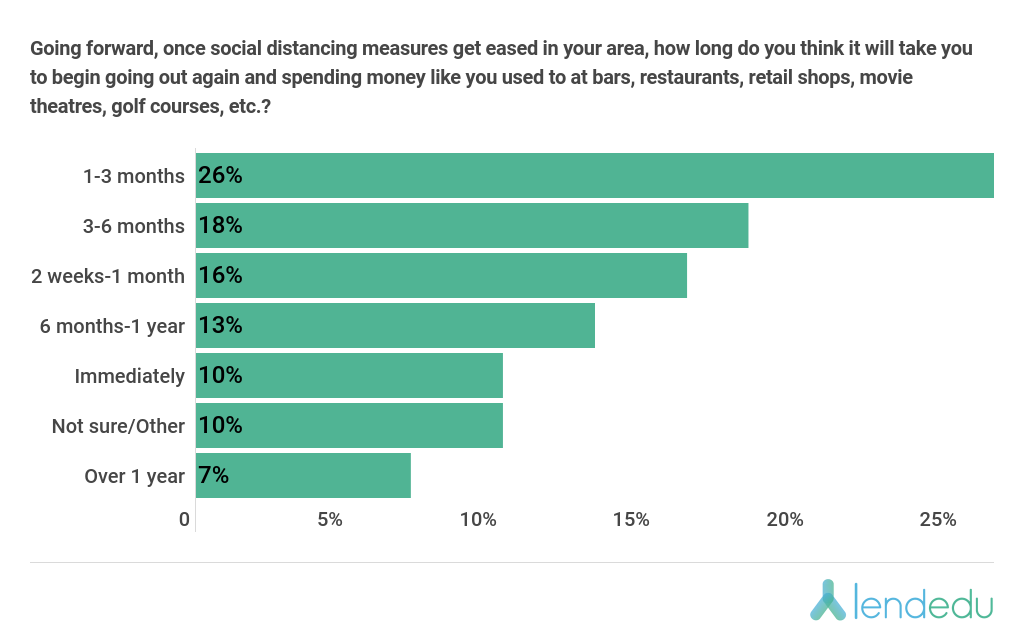

Consumer Economy May Take a While To Reboot Even When Social Distancing is Eased

The cost versus the cure has been a constant debate during the coronavirus pandemic, and each side of the argument has its merits. But sometimes it feels as if the debate centers around this notion that turning the economy back on is as simple as flipping a light switch.

More realistically, the reopening of the economy will be a drawn-out process with multiple phases. Consumers won’t simply flood restaurants, bars, theatres, and malls as soon as social distancing restrictions are lifted. The new normal will take some time to get used to for both business owners and patrons.

With this in mind, could it possibly mean financial ruin for businesses if they open back up, hire staff again, and drive up expenses only to have no revenue because people simply aren’t ready to reemerge en masse?

Take this article, for example, documenting the plans amongst small business owners in Raleigh, North Carolina, where some say they are not ready to pull employees off unemployment if they are unsure the business can sustain them during the initial reopening phases.

We asked our respondents about their plans to reengage with the economy once restrictions are lifted.

The plurality of respondents, 26%, said getting their consumer behavior back to normal will take between one and three months, while 18% said it will take them between three and six months. More respondents said it will take them between six months and one year than those who would get back into the swing immediately. And, 7% think it will take them over a year.

Judging by these results, it will take some time before businesses are operating at full tilt again. Expect this new phase of the debate to pick up steam in the coming weeks.

But ultimately, no matter how long it takes, many American businesses, both big and small, will adapt and bounce back like they always have.

Full Survey Results

All data is based on an online survey of 1,000 adult Americans commissioned by LendEDU and conducted by survey platform Pollfish. The survey was conducted on May 5, 2020. For some questions, the answer percentages may not add up to 100% exactly due to rounding.

If you would like to see a specific breakdown of the data other than those provided (ex. state-by-state, gender, age, employment status), or a full survey-to-survey-to-survey comparison, please email me at [email protected].

The results for identical questions from the first survey that was conducted on March 18, 2020 are in parentheses to the far right, while results from the second survey that was conducted on April 1, 2020 are second to the right. If there is only one set of parentheses for a given question, those are the results from the second survey since the question was not asked for the first survey.

1. Are you eligible to receive the one-time government payment of $1,200 or less as part of the coronavirus economic stimulus package?

- 76% of respondents answered “Yes” (66%)

- 14% of respondents answered “No” (12%)

- 11% of respondents answered “Not sure/I’d rather not say” (22%)

2. (Asked only to those who answered “Yes” to Q1) Have you received the one-time government payment of $1,200 or less as part of the coronavirus economic stimulus package yet?

- 73% of respondents answered “Yes”

- 26% of respondents answered “No”

- 1% of respondents answered “Not sure/I’d rather not say”

3. (Asked only to those who answered “Yes” to Q1) What will be/has been your main use of that one-time payment in the immediate future after you receive/received it?

- 32% of respondents answered “Save it in a savings account or emergency fund.” (30%)

- 2% of respondents answered “Invest it in the market.” (2%)

- 28% of respondents answered “Spend it on food, supplies, and other necessities.” (30%)

- 18% of respondents answered “Use it for a rent or mortgage payment.” (20%)

- 9% of respondents answered “Use it for a student loan, credit card, or other debt payment.” (7%)

- 2% of respondents answered “Use it for a vacation, entertainment, or other non-essential purchase (i.e. video games, Netflix account, etc.).” (1%)

- 7% of respondents answered “Other” (4%)

- 3% of respondents answered “Not sure” (5%)

4. How has the coronavirus and its impacts changed your job status?

- 26% of respondents answered “I still have my same job, nothing has changed.” (24%) (35%)

- 10% of respondents answered “I lost my job.” (12%) (6%)

- 14% of respondents answered “My hours have been partially cut.” (12%) (13%)

- 12% of respondents answered “My hours have been completely cut, but I haven’t lost my job (Furloughed).” (13%) (11%)

- 39% of respondents answered “None of the above/Already unemployed before it.” (38%) (36%)

5. (Asked only to those who answered “I lost my job” to Q4) Have you filed an unemployment claim since losing your job to receive unemployment benefits?

- 52% of respondents answered “Yes”

- 45% of respondents answered “No”

- 3% of respondents answered “I’d rather not say.”

6. (Asked only to those who answered “I lost my job” to Q4 & “Yes” to Q5) Have you received unemployment benefits yet?

- 46% of respondents answered “Yes”

- 54% of respondents answered “No”

- 0% of respondents answered “Not sure/I’d rather not say”

7. (Asked only to those who answered Q4 indicating that they still have a job in some capacity) Are you worried about your job security because of the coronavirus and its impacts?

- 52% of respondents answered “Yes” (55%) (57%)

- 41% of respondents answered “No” (38%) (36%)

- 7% of respondents answered “Not sure/I’d rather not say” (8%) (7%)

8. (Asked only to those who answered Q4 indicating that they still have a job in some capacity or just lost their job due to coronavirus) Before coronavirus and its impacts began seriously changing the U.S., were you living paycheck to paycheck?

- 56% of respondents answered “Yes” (63%) (64%)

- 41% of respondents answered “No” (34%) (32%)

- 3% of respondents answered “I’d rather not say” (4%) (4%)

9. Due to the coronavirus and its impacts, will you/have you already used money from a savings account or emergency fund to cover your expenses?

- 45% of respondents answered “Yes” (51%) (44%)

- 50% of respondents answered “No” (42%) (47%)

- 6% of respondents answered “Not sure/I’d rather not say” (7%) (9%)

10. Are you concerned about running out of money in your accounts due to the coronavirus and its impacts?

- 55% of respondents answered “Yes” (63%)

- 40% of respondents answered “No” (32%)

- 5% of respondents answered “Not sure/I’d rather not say” (5%)

11. In your best estimation, how much money have you spent on supplies and food due to the coronavirus and its impacts?

- The average amount of money spent on supplies and food due to the coronavirus and its impacts was $987.20, which is up 56% from the second survey when the average amount was $631.06 and 194% from the first survey when the average amount was $335.65.

12. Are you currently investing or saving for retirement through something like a 401(k), Roth IRA, or high-yield savings account?

- 33% of respondents answered “Yes” (35%) (38%)

- 62% of respondents answered “No” (59%) (57%)

- 6% of respondents answered “I’d rather not say” (6%) (5%)

13. (Asked only to those who answered “Yes” to Q12) Are you concerned that the Coronavirus and its impacts will seriously damage your retirement savings and plans?

- 62% of respondents answered “Yes” (72%) (63%)

- 31% of respondents answered “No” (20%) (30%)

- 7% of respondents answered “Not sure/I’d rather not say” (7%) (7%)

14. Do you currently have a mortgage?

- 32% of respondents answered “Yes” (32%) (35%)

- 66% of respondents answered “No” (65%) (63%)

- 2% of respondents answered “I’d rather not say” (3%) (2%)

15. (Asked only to those answered “Yes” to Q14) Are you worried about meeting your monthly mortgage payments due to the coronavirus and its impacts?

- 50% of respondents answered “Yes” (60%) (57%)

- 47% of respondents answered “No” (36%) (36%)

- 3% of respondents answered “Not sure/I’d rather not say” (4%) (7%)

16. Do you currently have outstanding student loan debt?

- 20% of respondents answered “Yes” (21%) (23%)

- 78% of respondents answered “No” (77%) (75%)

- 3% of respondents answered “I’d rather not say” (2%) (2%)

17. (Asked only to those who answered “Yes” to Q16) Are you worried about meeting your monthly student loan payments due to the coronavirus and its impacts?

- 55% of respondents answered “Yes” (60%) (63%)

- 41% of respondents answered “No” (36%) (32%)

- 4% of respondents answered “Not sure/I’d rather not say” (4%) (5%)

18. Do you currently have open credit card accounts?

- 60% of respondents answered “Yes” (63%) (63%)

- 37% of respondents answered “No” (34%) (35%)

- 3% of respondents answered “I’d rather not say” (3%) (2%)

19. (Asked only to those who answered “Yes” to Q18) Are you worried about meeting your monthly credit card payments due to the coronavirus and its impacts?

- 44% of respondents answered “Yes” (53%) (54%)

- 54% of respondents answered “No” (44%) (42%)

- 2% of respondents answered “Not sure/I’d rather not say” (4%) (4%)

20. (Asked only to those who answered “Yes” to Q18) Due to the coronavirus and its impacts, will you/have you been taking on more credit card debt than desired to cover your expenses?

- 33% of respondents answered “Yes” (39%) (42%)

- 62% of respondents answered “No” (55%) (53%)

- 5% of respondents answered “Not sure/I’d rather not say” (6%) (6%)

21. Were you actively invested in the stock market through a personal brokerage account when the coronavirus and its impacts began seriously changing the U.S. and is that account(s) still open?

- 26% of respondents answered “Yes” (28%) (27%)

- 70% of respondents answered “No” (68%) (70%)

- 5% of respondents answered “I’d rather not say” (3%) (4%)

22. (Asked only to those who answered “Yes” to Q21) Have you lost or made money in the stock market through your personal brokerage account since that point?

- 69% of respondents answered “Lost money” (81%) (79%)

- 21% of respondents answered “Made money” (10%) (8%)

- 10% of respondents answered “Not sure/I’d rather not say” (9%) (12%)

23. (Asked only to those who answered “Yes” to Q21) Going forward, what do you think will be your predominant stock market play as the coronavirus continues to have an impact?

- 23% of respondents answered “Buying more stock” (21%) (21%)

- 12% of respondents answered “Selling more stock” (10%) (13%)

- 55% of respondents answered “Holding steady” (55%) (52%)

- 10% of respondents answered “Not sure/I’d rather not say” (15%) (13%)

24. Going forward, once social distancing measures get eased in your area, how long do you think it will take you to begin going out again and spending money like you used to at bars, restaurants, retail shops, movie theatres, golf courses, etc.?

- 10% of respondents answered “Immediately”

- 16% of respondents answered “2 weeks – 1 month”

- 26% of respondents answered “1 – 3 months”

- 18% of respondents answered “3 – 6 months”

- 13% of respondents answered “6 months – 1 year”

- 7% of respondents answered “Over 1 year”

- 10% of respondents answered “Not sure/Other”

How to Manage Your Finances During the Coronavirus Pandemic

The COVID-19 pandemic has tightened budgets and shrunk bank accounts for so many American consumers.

Below, LendEDU lists out a few personal finance tips that may help you during this tough financial time.

Apply for Additional Financing

With many Americans out of work due to the pandemic, it has become difficult to meet regular expenses without significantly reducing savings or emergency accounts. Because of this, utilizing credit is not the worst idea if managed properly.

If you are a homeowner, you could tap into your home’s equity by taking out either a home equity loan or home equity line of credit (HELOC). Or more traditional financing options include a credit card or personal loan, which are available even for consumers with bad credit.

Stop Federal Student Loan Payments

Right now, all federal student loans have been placed in pandemic forbearance, which means no payments are required until October while all federal student loan interest rates are frozen at 0%.

If you are experiencing financial hardship, now would be a good time to take advantage of pandemic forbearance and instead use that money to meet other expenses. Unfortunately, the pandemic forbearance does not apply to private student loans.

Take on a Side-Hustle

The gig-economy is still strong in 2020, and there are plenty of opportunities out there to make some extra cash to cover costs. If you are struggling with finances or even out of work, look into some of these side-hustle ideas to strengthen your financial position.

Methodology

All data found within this report is based on a survey commissioned by LendEDU and conducted online by survey platform Pollfish. In total, 1,000 adult Americans ages 18 and up were surveyed. The appropriate respondents were found via Pollfish’s age-filtering feature. This survey was conducted on May 5, 2020. All respondents were asked to answer all questions truthfully and to the best of their abilities.

See more of LendEDU’s Research

About our contributors

-

Written by Mike Brown

Written by Mike BrownMike Brown uses data from surveys and publicly available resources to identify emerging personal finance trends and tell unique stories.