If you owe money for delinquent taxes, you have options to address and manage this debt. The IRS has a 10-year window to collect unpaid taxes, giving you ample time to explore solutions and create a plan to resolve your tax liabilities.

Keep reading because we’ll discuss how long the IRS has to collect tax debt, the rules it must follow, and the steps you can take to manage and even eliminate your tax debt. Our goal is to provide you with clear, actionable information to help you navigate and resolve your tax issues.

Table of Contents

Does IRS tax debt ever go away?

IRS tax debt can go away, but it typically takes 10 years before the Internal Revenue Service will stop pursuing your debt.

Every tax liability has a Collection Statute Expiration Date, or CSED. This CSED date is the government’s statute of limitations on your debt or the maximum period that the IRS has to try to collect the debt.

Each tax liability has its own CSED, calculated from the tax assessment date. The clock starts ticking on the day the IRS calculates your tax debt, regardless of whether you filed a tax return. The CSED for that tax liability is 10 years from the assessment date.

This 10-year rule applies to tax debts that arise from:

- Returns you voluntarily file with the IRS

- Amendments to returns you voluntarily file

- Substitute returns you file after failing to file a return with the IRS

- Audits and penalties

If you file your taxes using false or fraudulent information, and the correction of this information results in an increased tax liability, a new CSED would begin on the date the IRS makes the correction.

But the 10-year rule is more of a general guideline. This time frame can be suspended or extended, depending on the circumstances.

Can tax debt collection be paused or extended?

Certain situations can result in the suspension or extension of your Collection Statute Expiration Date (CSED), during which the IRS cannot collect your tax debt. However, in some cases, the IRS may also extend the CSED, giving it more than the standard 10 years to collect the debt.

During a suspension, the IRS pauses collection efforts. If the specific situation ends, such as not following through with a payment plan, the IRS can resume collection activity. The remaining time on the original 10-year CSED will continue ticking.

Here are instances when tax debt collection might be paused or extended.

| Action | Initial suspension | Extension |

| File for bankruptcy | During settlement | 6 months after conclusion |

| Apply for installment agreement | During application review | 30 days if you withdraw or application is rejected |

| Submit Offer in Compromise (OIC) | During application review | 30 days if application is rejected |

| File for innocent spouse relief | For 90 days and then during court ruling | 60 days, regardless of ruling |

| Live outside the U.S. | While living abroad, if 6 months or more | Extended upon return for at least 6 months |

| Enter a combat zone | While in combat zone, plus 180 days | N/A |

| Serve in the military | During service, plus 270 days | N/A |

File for bankruptcy

Filing for bankruptcy can provide relief from tax debt and result in suspensions and extensions:

- Suspension: From the date you petition for bankruptcy until the court settles the filing, your CSED is suspended.

- Extension: The IRS will add six months to your CSED from the conclusion of your bankruptcy.

Apply for an installment agreement

If your tax debt seems insurmountable, you may get on an installment plan with the IRS:

- Suspension: The IRS will suspend your CSED while reviewing your application, accepting or rejecting it. The suspension continues if you appeal a rejection.

- Extension: If you withdraw from consideration or the IRS rejects your application, the IRS will extend your CSED by 30 days.

Submit an Offer in Compromise

You can file for an Offer in Compromise (OIC) if you owe significant back taxes and can’t pay the total amount:

- Suspension: The IRS suspends your CSED while reviewing your application. If it rejects your application and you appeal, the suspension continues.

- Extension: If the IRS rejects your OIC, it adds 30 days to your CSED

File for innocent spouse relief

You may avoid paying additional taxes if your spouse filed a joint return with errors:

- Suspension: If approved, your CSED is suspended until you file a waiver or after the 90 days to petition the tax court. The suspension remains until the court decides.

- Extension: The CSED is extended by 60 days, regardless of the decision.

Live outside the United States

Living abroad for six months or more affects IRS tax debt collection:

- Suspension: The IRS suspends tax debt collection during your time abroad.

- Extension: Upon returning to the U.S., the IRS extends your CSED by at least six months.

Enter a combat zone or serve in the military

Entering a combat zone or serving in the military can also result in suspending tax debt collection. No extensions are associated with these scenarios.

- Entering a combat zone: The IRS suspends your CSED for your entire duration in the combat zone, plus 180 days.

- Serving in the military: Military members have their CSED suspended during service, plus 270 days.

How do I find my tax balance and expiration date?

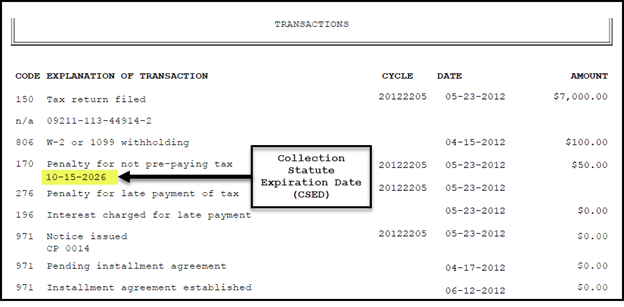

If you have a tax liability, knowing how much you owe and how long the IRS can attempt to collect it is important. You can find both of these pieces of information in your account transcript from the IRS.

A tax account transcript contains information such as your filing status and taxable income. Still, you can also use this document to review past transactions, which will detail any amount owed and the date the money is due (the CSED).

Here’s what a sample tax transcript looks like:

Source: Fictional IRS account transcript from the IRS

Not sure how to get your account transcript? The IRS offers multiple ways to get your hands on this important document.

By phone

The first option is to call the IRS and request information on the tax debt as well as the original date of assessment. From that date, you can calculate the original CSED, assuming there haven’t been any suspensions or extensions. Taxpayers can call the IRS at 800-829-1040.

If you are working with a third party—such as a tax preparer or other professional—they can call the Practitioner Priority Service (PPS) on your behalf to request a transcript. This report will outline each of your tax liabilities as well as when the debt was first assessed.

Online

Phone lines at the IRS are often backed up, so service can be limited. For this reason, requesting a tax transcript online may be the fastest and easiest way to find your total tax liability and the statute of limitations on that debt. To complete this request, you must create an account if you don’t have one already and verify your identity.

By mail

You can request that a tax account transcript be sent to you by mail. This is not as fast as getting one online, but it may be easier for some taxpayers. Request a transcript by mail by calling the IRS at 800-908-9946 or by submitting an online form.

What do I do if my IRS debt won’t go away soon?

| Option | Best for |

| Offer in Compromise | When you can’t repay your IRS debt |

| Installment agreement | Obtaining more manageable payments over a set amount of time to repay your debt |

| Penalty or interest abatement | If you are responsibly making payments and could use a little more relief |

| Third-party help | When you are overwhelmed and confused by the tax relief process |

If you owe money to the IRS for delinquent taxes, you might be unsure of what to do or how to handle your debt. Don’t wait for the IRS to chase you down for payment.

The IRS can create headaches in the form of tax liens and levies in pursuit of your back taxes, and you’ll accrue penalties and interest charges.

Instead of ignoring an IRS tax debt, consider your options for tax relief. These could include requesting one of the following.

Offer in Compromise

If paying your tax debt would result in financial hardship, you may be eligible for an Offer in Compromise (OIC). This enables you to settle your debt with the IRS for less than you owe, considering factors such as your income, expenses, and asset equity.

The IRS accepts about one in three OIC applications. If approved, you’ll either:

- Make a lump-sum payment of 20% of the total amount offered, then pay the remaining balance in five or fewer payments.

- Agree to periodic payments over a set number of months agreed to with the IRS.

It costs $205 to file for an OIC.

Installment agreement

Setting up an installment agreement plan with the IRS allows you to spread your payments over a manageable period of time and suspends collection activity and possible levies in the interim.

Depending on your debt, short- and long-term payment plans are available. Setup fees for the installment plan and interest on the balance still apply.

Penalty or interest abatement

If you have already established a payment plan for your current debt, you may be able to get some or all of your penalty and interest charges waived.

These added fees can be reduced or removed for certain taxpayers who qualify for first-time penalty abatement and even in cases where the taxpayer believes they received incorrect verbal advice from an IRS administrator.

Third-party help

You may also consider hiring a third-party tax relief company to work on your behalf. These firms offer professional guidance throughout the tax debt process and help taxpayers apply for an Offer in Compromise or seek penalty abatement.

If you think this option might make sense for you, check out our list of the best tax relief companies.

About our contributors

-

Written by Timothy Moore, CFEI®

Written by Timothy Moore, CFEI®Timothy Moore is a Certified Financial Education Instructor (CFEI®) specializing in bank accounts, student loans, taxes, and insurance. His passion is helping readers navigate life on a tight budget.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Gail Urban, CFP®

Reviewed by Gail Urban, CFP®Gail Urban, CFP®, AAMS®, has been a licensed financial advisor since 2009, specializing in helping individuals. Before personal financial advising, she worked as a business financial manager in several industries for about 25 years.