Auto Loans

- Easy online application

- Allows cosigners

- Large lender network

- Prequalify without affecting your credit

- Lack of fee transparency

| Rates (APR) | 4.67% – 17.99% |

| Loan amounts | $2,500 – $100,000 |

| Repayment terms | 24 – 84 months |

| Min. credit score | 600 |

Refinance Auto Loans

- Competitive refinancing rates

- 3 refinance options

- 100% online process

| Rates (APR) | 4.67% – 17.99% |

| Loan amounts | $2,500 – $100,000 |

| Repayment terms | 24 – 84 months |

| Min. credit score | 600 |

Autopay is an online marketplace specializing in auto loans and auto loan refinancing. As an online platform, Autopay allows consumers to compare loan offers from various financial institutions, making it easy to find competitive rates.

While Autopay is not a direct lender, it serves as a “virtual financial office” to simplify the loan process. Autopay earns our designation as the best auto loan for bad credit, offering accessible refinancing solutions for consumers with less-than-perfect credit scores.

Autopay at a glance

Autopay offers a wide range of loan options, making it a versatile choice for consumers looking to refinance or purchase a vehicle. Here’s a snapshot:

| Term | Details |

| Rates (APR) | 4.67% – 17.99% |

| Loan amounts | $2,500 – $100,000 |

| Repayment terms | 24 – 84 months |

| Min. credit score | 600 |

These features make Autopay appealing to a broad range of borrowers. It offers flexibility with loan amounts from as low as $2,500, which can be ideal for older or less expensive vehicles, up to $100,000 for higher-value cars.

With repayment terms extending up to 84 months, borrowers have the option to select more manageable monthly payments, even with less favorable credit.

Am I eligible for Autopay?

Autopay’s eligibility criteria are accessible for many consumers, which is why it earns our top spot for best auto loan for bad credit. Here’s why:

- Minimum credit score: Autopay requires a credit score of just 600, making it accessible for borrowers with lower credit scores who might not qualify for loans with other lenders.

- Minimum annual income: With a minimum annual income requirement of $24,000, Autopay remains within reach for many working individuals or households with modest incomes, allowing borrowers to access refinancing options even if their finances are limited.

- Nationwide availability: Autopay offers loans in all 50 states, giving borrowers across the U.S. access to its platform without geographic limitations.

Why it’s best for bad credit

Autopay allows borrowers with bad credit to access refinancing options that can improve their financial situation. Borrowers with poor or fair credit often face higher interest rates, but Autopay offers the opportunity to compare multiple lenders, helping borrowers find more competitive rates despite their credit history.

By refinancing through Autopay, borrowers may lower their monthly payments or secure better loan terms, which can make their auto loan more manageable even with a lower credit score.

Why refinance your auto loan with Autopay?

Refinancing through Autopay offers significant savings potential, especially for borrowers looking to lower their monthly payments or secure better interest rates. According to Autopay, customers who refinance may cut their interest rates in half, leading to an average savings of $100 per month. This can add up to substantial financial relief over the life of the loan.

Autopay provides several refinancing options to fit unique borrower needs:

- Traditional refinancing: To save on overall interest, you can reduce your interest rates, lower your monthly payments, and even shorten the loan term.

- Cash back refinancing: With this option, access up to $12,000 in cash, which you can use to pay off high-interest debt or make large purchases.

- Lease buyout refinancing: Ideal for those nearing the end of a lease, this option allows borrowers to pay off their lease early, avoid mileage penalties, and keep their car.

To start the refinancing process, Autopay requires basic information, including the loan payoff amount, remaining term, and current APR. You can also indicate your credit status—excellent, average, or rebuilding—to find tailored offers from a range of lenders.

Even borrowers with less-than-perfect credit can find competitive options through Autopay’s marketplace, though vehicle make and model restrictions may vary by lender.

By offering multiple refinancing options and access to various lenders, Autopay makes it easier for borrowers to find a loan that fits their financial goals, even if their credit isn’t ideal.

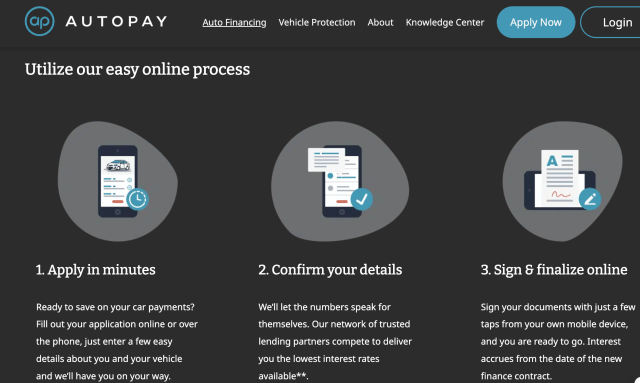

How to get an auto loan or refinance through Autopay

Follow these simple steps to prequalify and apply for an auto loan through Autopay:

1. Prequalify for a loan

- Go to the Autopay website and click “Get started” to begin the prequalification process. Autopay will perform a soft credit inquiry, which won’t affect your credit score.

- Provide information, such as the type of loan you’re interested in (refinancing or purchasing), whether you’re buying from a dealer or a private seller, vehicle information, and a few personal details to see available loan options.

This process typically takes just a few minutes, and you’ll be able to compare rates from multiple lenders.

2. Review loan offers

Once prequalified, you can see a list of loan offers with different interest rates and terms based on your financial profile. Interest rates may vary depending on the lender, so take your time reviewing the details.

3. Select a loan offer

- After comparing the offers, choose the loan that best suits your needs.

- Keep in mind that no hard credit pull will be performed until you select a specific offer.

4. Complete the loan application

Once you’ve chosen a loan, complete the application by providing the necessary documentation:

- Driver’s license

- Proof of income (such as tax returns or pay stubs)

- Proof of insurance

- Proof of residence

5. Submit documentation for processing

Upload your documents through Autopay’s platform. The platform will verify your information and submit your application to the lender for final approval.

There’s no application fee, and loan offers are valid for 30 days, so you have flexibility to decide.

6. Wait for final approval

After submitting your application, the lender will conduct a hard credit inquiry to finalize the loan.

Decision times can vary, but many applicants receive a quick response.

Once you’ve completed these steps, you can finalize your loan and get the funds for your auto purchase or refinancing.

Pros and cons

Before you proceed with Autopay, consider the risks and benefits.

Pros

-

All-online process

This is convenient if you don’t want to have to work with a dealership or go in person to a bank or lending institution.

-

Large network of lenders

Borrowers with a range of credit scores can easily shop around and find the best rates and terms.

-

Cosigners allowed

This feature helps those with lower credit scores get approved.

-

Prequalification available

You can see what rates you might qualify for without affecting your credit.

-

Competitive rates

Creditworthy borrowers may qualify for some of the lowest rates available.

-

3 options for refinancing

In addition to traditional refinancing, you can refinance to get cash back or buy out your lease.

Cons

-

Lack of transparency in fees

A primary customer comment is that Autopay may advertise low interest rates, but after factoring in fees, several customers said they ended up paying more than before refinancing.

Is Autopay a reputable company?

| Source | Rating | Number of reviews |

| Trustpilot | 2.9/5 | 577 |

| Better Business Bureau (BBB) | 4.59/5 | 1,034 |

| 4.7/5 | 9,733 |

Autopay’s reputation varies across review platforms, with positive and critical feedback from users. Many customers appreciate the responsive customer service and seamless loan process, often citing agents who guided them through every step and helped them save money on their auto loans.

But several reviews raise concerns about transparency and pressure tactics. A few users report feeling rushed into signing without enough time to review the paperwork or uncovering hidden fees only after receiving the documents. Others mention that Autopay doesn’t always secure the best available rates, particularly when compared to those directly from lenders.

One fee that some consumers feel Autopay isn’t fully transparent about is the documentation (doc) fee. Before finalizing a loan through Autopay, it’s important to review the fine print and ensure all fees, including the doc fee, are accounted for in the overall cost of your new loan or auto refinancing agreement.

We noticed comments about multiple credit inquiries after using Autopay’s platform. Some customers noted that their application was shared with various lenders without their knowledge, leading to a spike in credit checks. Overall, while many borrowers have had positive experiences with Autopay, it’s important to review all terms and compare rates before committing.

Does Autopay have a customer service team?

Yes, Autopay’s customer service team is available to assist borrowers with any questions or concerns.

You can call 844-276-3272 during the following hours:

- Monday – Friday: 7 a.m. – 7 p.m. Mountain time

- Saturday: 9 a.m. – 5 p.m. Mountain time

Autopay’s offices are closed on Sunday.

You can email [email protected], or send mail to: Autopay, 8055 E. Tufts Ave., Denver, CO 80237.

The Autopay website also offers a contact form, allowing you to ask a specific question and wait for a response via email.

Autopay alternatives

Depending on your needs, Autopay might not be the best fit for you.

- If you’re looking for an auto loan, consider MyAutoLoan for another way to comparison shop.

- RateGenius is an excellent comparison shopping option for refinancing.

- If you have good credit, LightStream is a solid lender for auto loans and refinancing with competitive terms.

Here are several top-rated companies to consider:

| Company | Best for… | Product | Rating (0-5) |

|---|---|---|---|

|

|

Best for comparison shopping | Refinance |

|

|

Best for comparison shopping | Auto loans |

|

|

|

Best for flexible terms | Refinance |

|

|

Best for no vehicle restrictions | Auto loans & refinance |

|

|

|

Best for lifetime financing | Auto loans & refinance |

|

|

Best refinancing for bad credit | Refinance |

|

How we rated Autopay

We designed LendEDU’s editorial rating system to help readers find companies that offer the best auto loans and refinancing. Our system awards higher ratings to companies with affordable solutions, positive customer reviews, and online transparency of benefits and terms.

We compared Autopay to several auto loan lenders, using hundreds of data points from company websites, public disclosures, customer reviews, and direct communication with company representatives. We weighted, scored, and combined each factor to produce a final editorial rating. This rating is expressed on a scale from 1 to 5, with 5 being the highest possible score. Our take is represented in our rating, recapped below.

| Product | Our rating |

| Autopay auto loans | 4.1/5 |

| Autopay auto loan refinance | 4.2/5 |

About our contributors

-

Written by Jeff Gitlen, CEPF®

Written by Jeff Gitlen, CEPF®Jeff Gitlen, CEPF®, is the director of growth at LendEDU. He graduated from the Alfred Lerner College of Business and Economics at the University of Delaware.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.