Our take: The IRS doesn’t list specific income or debt requirements for the Offer in Compromise (OIC) program. You can apply on your own using an online form, but it can take some time. Getting help from a tax relief company or a free government service might be worth it.

The IRS’s Offer in Compromise (OIC) can be a game-changer if you can’t afford to repay your tax debt. Applying for the program and determining whether you qualify can be challenging, though.

There isn’t a single solution for OICs because the best approach depends on your situation and how much time you have for paperwork. Whether you want to apply yourself or get help, our guide can help.

Table of Contents

What is an Offer in Compromise (OIC)?

An OIC lets you settle your debt for less than the full amount, either with a single payment or through monthly installments.

For example, if you owe $40,000 in taxes but can’t pay the full amount, you might offer a lump sum of $10,000 through an OIC. If the IRS accepts it, your debt is settled.

Qualification requirements

So, how do you get an OIC approved? It depends. You won’t find a set list of income requirements or minimum debt amounts.

These are the only eligibility requirements you’ll find from the IRS:

- You’re up to date on all required tax returns

- You have an assessed tax debt (meaning the IRS has issued a tax bill)

- You’re making required estimated tax payments for the current year

That’s it. There’s no published minimum income threshold or required debt amount.

What you have to show is that you can’t afford to pay the entire amount you owe. Here’s what the IRS looks at to make that determination.

Income

Your income is a major factor in your offer. However, the IRS does not require you to earn less than a specific amount. Instead, it looks at how your income compares to your family size, where you live, and your necessary expenses.

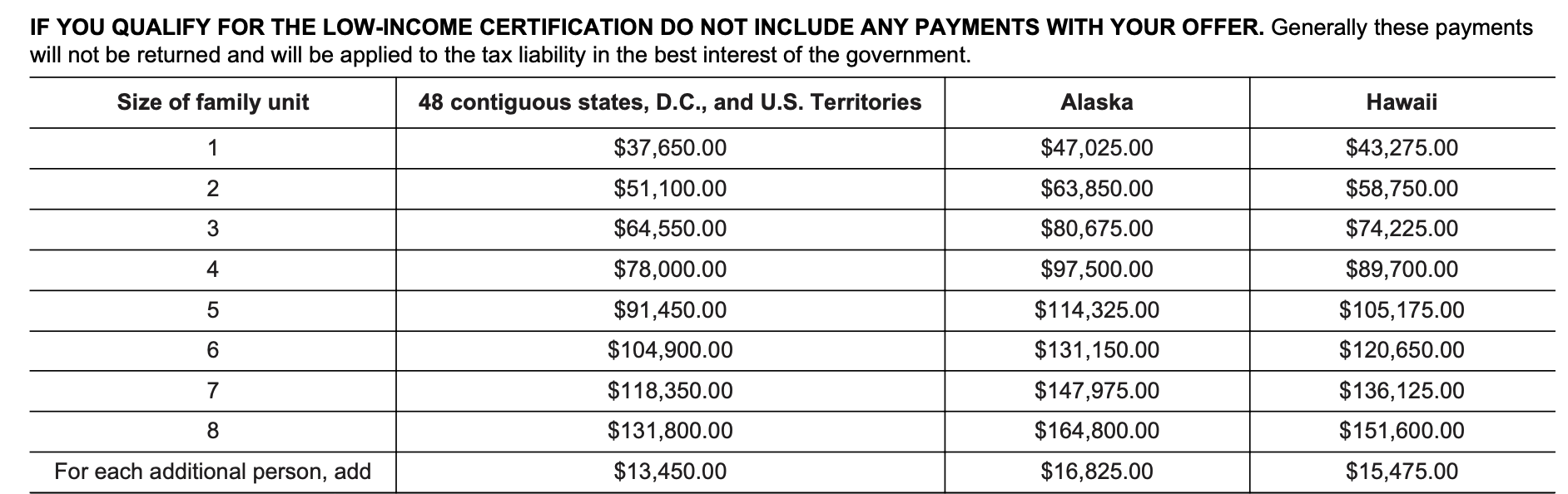

You can see how your income compares to your expenses by looking at the IRS’s low-income certification guidelines. You do not need to qualify as low income to apply for an OIC, but the chart can help you understand where you stand.

If you qualify as low-income, the IRS waives the $205 application fee, and you don’t have to include a payment.

Assets

You need to show that you don’t have enough assets to pay off your full debt. If you do have enough, you must prove that using those assets would cause you “economic hardship.” Assets can include savings, investments, checking accounts, and real estate.

For example, if you owe $35,000 and don’t have cash on hand but have $150,000 in an investment account, your offer probably won’t be accepted because you have enough assets to pay the full amount.

Economic hardship

You might qualify for an OIC if you can show you’re “unable to pay reasonable basic living expenses.” For example, imagine you have a family of five and your monthly income is $9,000.

Your monthly expenses for housing, transportation, groceries, tuition, and utilities total $12,000. To make up the difference, you use your savings each month.

Even though you have a savings account with a solid balance, you need it to pay your necessary expenses and can’t afford an extra payment toward tax debt.

Spending

The IRS also considers how your necessary expenses compare with your income. If your spending is within the national standards for your family size, the IRS won’t question it. If it’s higher, you need to explain why.

The IRS has a pre-qualifier tool to help you figure out your offer amount. However, we noticed it can be glitchy, especially during tax season.

To increase your chance of being approved, start by using the pre-qualifier tool to ensure you’re eligible. From there, make sure you follow the steps thoroughly and have all the required supporting documentation. Consider hiring a professional who understands the process and requirements.

How to get your Offer in Compromise approved

There’s no way to guarantee your offer will be approved, but you can take steps to improve your chances. Here are some tips to help you prepare.

Consider hiring a professional

The OIC application process is similar to filing your taxes—everyone can file their own, but that doesn’t mean everyone wants to or is good at it. Detail-oriented applicants who are good at following multi-step directions will probably excel with a DIY approach. But if you’re not comfortable with long forms or calculations, you might want to get professional help.

TaxRise is our top choice for Offer in Compromise support. The company walks you through the process and completes the application for you. Plus, you get a 100% satisfaction guarantee and free help if you need to appeal the decision.

You can also get free help from the Taxpayer Advocate Service (TAS) or, if you qualify, from a local Low Income Taxpayer Clinic.

In most cases, I recommend hiring a professional for OIC support. The process requires very specific information about your income, expenses, and ability to pay. A professional can ensure that you meet the qualifications, walk you through the various steps, and assist with creating a realistic offer. A good tax professional can also help you find other solutions for paying your tax liability if the OIC is not approved.

Get specific about expenses

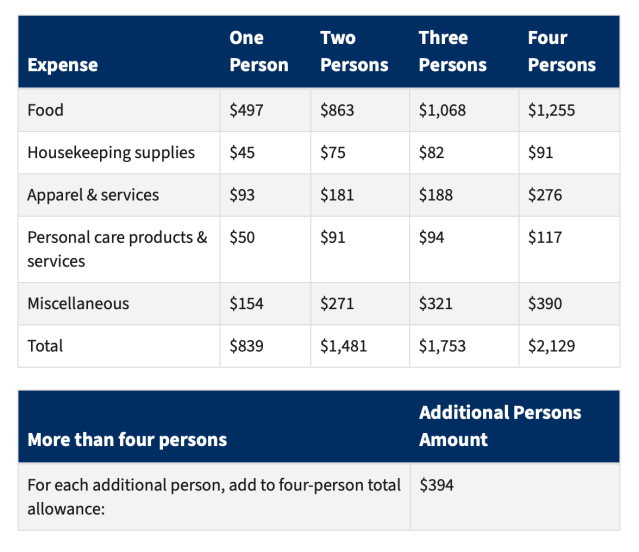

Figuring out your expenses takes a bit more effort, but it’s important. The IRS checks how much is left after paying your necessary expenses.

For example, if your gross monthly income is $5,000, you might estimate your expenses at $3,000. But after reviewing each expense, you find you actually spent $4,800. That means you have $1,200 less left over than you thought, which can help your offer get approved.

Here are some common expenses you can include.

- Food

- Clothing

- Housekeeping supplies

- Personal care products

- Health insurance

- Life insurance

- Minimum credit card payments

- Car payments

- Student loans

Create a realistic offer

If you submit an offer that is realistic—not too high or too low—you have a better chance of getting approved for an OIC. The IRS form gives you step-by-step instructions for the calculation, and you need to complete every section.

To figure out your offer, you’ll use a two-step process using numbers from earlier sections to get the right amount. Here’s how it works.

| 1. Remaining monthly income x 12 = future remaining income 2. Available equity in assets + future remaining income = Offer in Compromise amount |

For example, let’s say your remaining monthly income after expenses is $500, so your future remaining income is $6,000 ($500 x 12 = $6,000). You also have $10,000 available in assets, so your offer amount is $16,000 ($6,000 + $10,000 = $16,000).

Triple-check the application

Check that everything is accurate and then check it again. After that, check it again. You want to make sure that your calculations are correct and you’ve provided all the necessary information. It’s a long form with a lot of details. Mistakes on the form further delay the process.

Accept or appeal the offer

After you receive a response to your offer, decide whether to accept or appeal it. You only have 30 days to appeal, so try to decide as soon as possible. Follow the directions on your form to file an appeal. In most cases, you can also ask for reconsideration if your offer is returned without a decision.

How long does the process take?

The IRS may take up to 24 months to finish reviewing your Offer in Compromise, but you’ll usually get a response much sooner.

Within a few weeks or months, you will get a letter or phone call from the IRS. They may confirm receipt of your offer, request more details, or explain their decision.

Common mistakes to avoid

Many people make these common Offer in Compromise mistakes, but you can avoid them. Here’s what to watch for.

You calculate the offer wrong

The good news is that the IRS will recalculate it and update your offer. If it’s more than what you offered, the IRS will contact you and give you a chance to increase it.

You send a combined payment

When you submit your Offer in Compromise, send two separate checks: one for the application fee and one for the initial payment. Paying online can help you avoid this mistake.

You expect your payment back

You will not get your initial payment back, even if the IRS rejects your offer. The payment goes toward your tax debt and is nonrefundable.

Best tax relief companies for Offers in Compromises

If you need help with your Offer in Compromise, consider starting with one of these top tax relief companies.

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

|

Best Offer in Compromise Support |

|

|

|

Best Lowest-Price Guarantee |

|

|

|

Best Initial Investigation |

|

Article sources

At LendEDU, our writers and editors rely on primary sources, such as government data and websites, industry reports and whitepapers, and interviews with experts and company representatives. We also reference reputable company websites and research from established publishers. This approach allows us to produce content that is accurate, unbiased, and supported by reliable evidence. Read more about our editorial standards.

- IRS, National Standards: Food, Clothing, and Other Items

- IRS, Form 656 Booklet: Offer in Compromise

- IRS, Offer in Compromise: Frequently Asked Questions

- IRS, Form 656

- IRS, Form 433-A (OIC)

- Taxpayer Advocate Service, Can TAS Help Me with My Tax Issue?

- Taxpayer Advocate Service, Low Income Taxpayer Clinics (LITC)

- IRS, Form 911

- Taxpayer Advocate Service, Economic Hardship

About our contributors

-

Written by Taylor Milam-Samuel

Written by Taylor Milam-SamuelTaylor Milam-Samuel is a personal finance writer and credentialed educator who is passionate about helping people take control of their finances and create a life they love. When she's not researching financial terms and conditions, she can be found in the classroom teaching.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Chloe Moore, CFP®

Reviewed by Chloe Moore, CFP®Chloe Moore, CFP®, is the founder of Financial Staples, a virtual, fee-only financial planning firm based in Atlanta, Georgia, and serving clients nationwide. Her firm is dedicated to assisting tech employees in their 30s and 40s who are entrepreneurial-minded, philanthropic, and purpose-driven.