USAA, a member-owned financial institution serving military families, has delivered $411 million in relief to federal workers in just 35 days of the current government shutdown.

More than 120,000 federal employees have taken advantage of special zero-interest loans (totaling $384 million) just to cover basic expenses while their paychecks remain frozen, as well as loan and credit payment extensions and waived overdraft fees.

The government shutdown ended on November 12, 2025. It lasted 36 days, the longest in U.S. history.

This staggering figure tells a story about what happens when safety nets fail. But it’s not just about the shutdown. Recent changes to the Supplemental Nutrition Assistance Program (SNAP) suggest we’re dismantling the very systems designed to catch people when they fall, and the timing couldn’t be worse.

Table of Contents

The shutdown’s immediate toll

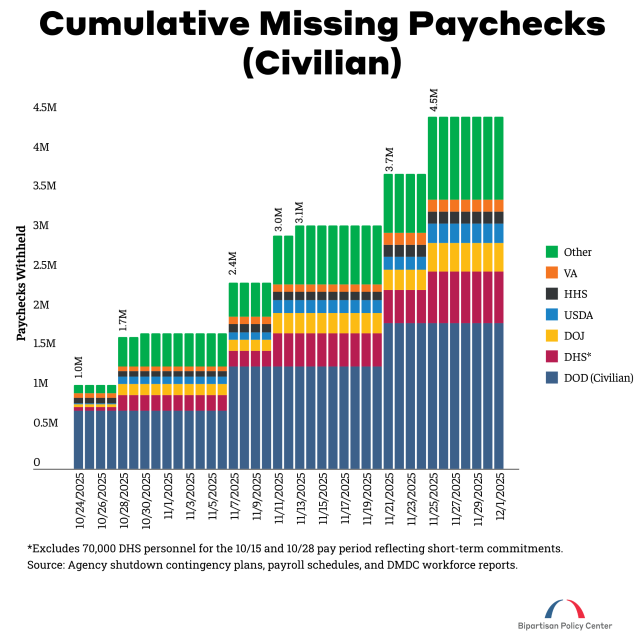

Since October 1, approximately 1.4 million federal workers have missed paychecks. They received their last partial paychecks on October 10 and then missed their first full paycheck on October 24. While Congress has guaranteed back pay once agencies reopen, that doesn’t help families facing bills today.

Banks and credit unions have stepped in where the government left off. USAA’s loans, which offer up to $6,000 per worker, are designed as paycheck replacements. The loans are interest-free and fee-free, giving workers 90 days to repay once issued.

Navy Federal Credit Union offers a similar program, and during the 2018 to 2019 shutdown that lasted 35 days, it issued $53 million in loans to 32,000 members. This time around, enrollment has been “significantly higher,” according to an assistant vice president at the lender. Redwood Credit Union has issued roughly $160,000 to 60 recipients.

Human cost of the shutdown

The human cost behind these numbers is significant. One San Antonio woman whose husband works for the Department of Defense told CBS News her family took out a $3,200 loan to cover bills. One of their five children has special needs and underwent spinal fusion surgery earlier this year. Medical bills from the procedure are now coming due at exactly the wrong time.

Another family in San Diego is using their loan to cover therapy sessions for their son with autism and their daughter’s braces. The mother is delaying her own necessary dental work until the shutdown ends.

A preview of what’s to come?

The shutdown reveals what happens when financial support disappears suddenly. But while banks have offered a temporary solution for federal workers, upcoming changes to SNAP, the nation’s largest nutrition assistance program, suggest millions more Americans could face similar crises without emergency backup.

The One Big Beautiful Bill Act (OBBBA), signed into law earlier this year, fundamentally restructures SNAP in ways that will severely limit its ability to respond to economic downturns.

And unlike zero-interest loans from sympathetic banks, there’s no easy replacement for food assistance that helps 42 million Americans afford groceries.

SNAP funding changes (even after the shutdown ends)

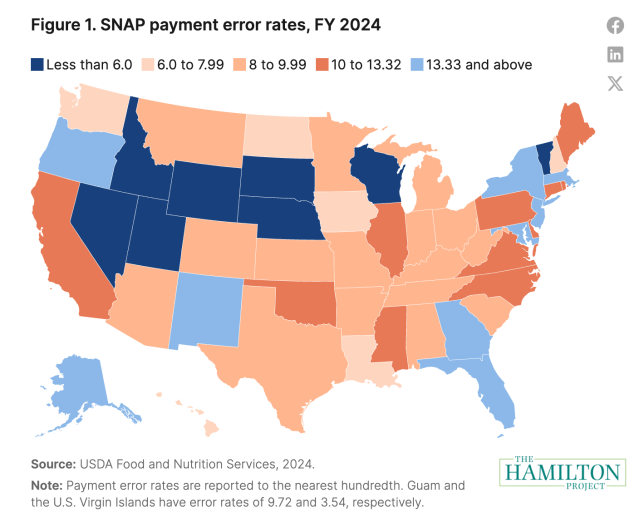

For more than 50 years, SNAP benefits have been fully funded by the federal government. Starting in October 2027, that changes. Under OBBBA, states will pay a portion of SNAP benefits based on their payment error rates, a measure of how accurately they determine eligibility.

States with error rates below 6% pay nothing. As error rates climb, so does the state’s share, reaching 15% of benefits for states with error rates above 13.32%.

Only eight states had error rates below 6% in fiscal year 2024, and nine states and Washington, D.C., exceeded 13.32%. Error rates fluctuate frequently; 47 states have spanned at least two different cost-sharing tiers since 2017.

The Congressional Budget Office estimates this cost shift will cause some states to drop out of SNAP entirely.

The current shutdown offers a preview of how fragile SNAP funding has become. On November 1, the U.S. Department of Agriculture (USDA) froze SNAP benefits for the first time in the program’s 60-year history, citing the government shutdown. Federal judges ordered the administration to use $4.6 billion in contingency funds, but that money only covers half of November’s benefits for 42 million recipients.

Agriculture Secretary Brooke Rollins said it will take several weeks to distribute even these partial payments, and officials have warned it could take months in some cases.

The recession problem

The 2027 changes to SNAP become particularly problematic during economic downturns, exactly when the program is needed most.

SNAP has historically functioned as an automatic stabilizer, expanding naturally as the economy contracts. When people lose jobs or income, they become eligible for SNAP and can quickly receive benefits to buy groceries. Because recipients spend these benefits immediately in their local communities, SNAP doesn’t just help families; it stimulates the broader economy.

During recessions, every additional dollar spent on SNAP benefits generates between $1.40 and $1.79 in total economic activity, according to USDA estimates. During the Great Recession specifically, every $10,000 in new SNAP benefits created one additional job in rural counties.

But the new cost-sharing structure threatens this automatic response. During recessions, SNAP enrollment increases as more families need assistance. At the same time, error rates tend to rise when states must process an influx of new applicants with larger caseloads. Meanwhile, state tax revenues decline during downturns.

What it means

The result: States will owe more money for SNAP precisely when they have less money to spend and face constitutional requirements to balance their budgets. Unlike the federal government, states can’t borrow to cover increased costs during recessions.

This creates a perverse incentive for states to cut SNAP benefits or end participation entirely during the exact moments when residents need help most.

Stricter work requirements

OBBBA also expands SNAP work requirements to adults aged 55 to 64 and parents whose youngest child is between 14 and 17. The law also eliminates exemptions for veterans, people experiencing homelessness, and former foster youth.

These time-limited work requirements mandate that participants work or participate in approved activities for at least 80 hours per month. Failure to comply means only three months of SNAP benefits in a three-year period.

Fewer waivers

The law also restricts states’ ability to waive these rules when jobs are scarce. Previously, states could request waivers for areas where unemployment was 20% higher than the national average. Under OBBBA, waivers are only available for areas with unemployment rates of 10% or higher.

During the entire Great Recession, the national unemployment rate hit 10% for just one month. About 40% of Americans lived in counties where unemployment never reached 10% during that deep recession.

The Congressional Budget Office estimates these changes will reduce SNAP participation by 2.4 million people monthly over the next decade.

2 sides of the same crisis

The government shutdown and SNAP restructuring may seem like separate issues, but they tell the same story about eroding support systems.

The shutdown shows what happens when 1.4 million workers suddenly lose income through no fault of their own. Private lenders have issued emergency loans, but that’s a Band-Aid, not a solution.

The SNAP changes show what happens when we dismantle systems designed to catch people during economic crises. By shifting costs to states and restricting when they can waive work requirements, we’re dismantling SNAP’s role as an automatic stabilizer when economic uncertainty makes that role crucial.

Banks issuing emergency loans underscores how quickly financial disruptions can affect individual Americans, while SNAP restructuring shows what can happen when there is no comparable safety net from the private sector.

Bottom line

Both moments reveal the same truth: When safety nets weaken, ordinary people bear the cost. Whether it’s missed paychecks or missed meals, we’ve built a system that relies on temporary fixes rather than long-term stability.

Recommended readings

- Are SNAP Benefits Ending? How the Government Shutdown Affects SNAP EBT and 42 Million Americans

- What Happens in a Government Shutdown? Who’s Affected?

- Gen Z Credit Scores Drop to 676, Lowest of Any Generation in 2025

Article sources

At LendEDU, our writers and editors rely on primary sources, such as government data and websites, industry reports and whitepapers, and interviews with experts and company representatives. We also reference reputable company websites and research from established publishers. This approach allows us to produce content that is accurate, unbiased, and supported by reliable evidence. Read more about our editorial standards.

- CBS News, As They Miss Paychecks, Furloughed Federal Workers Are Taking Out Bank Loans to Help Pay the Bills

- USAA, USAA Has Delivered Over $411M in Shutdown Relief, Continues to Serve Impacted Members

- New York Times, White House Says It Will Make Some SNAP Payments After Trump Threatened to Defy Court

- Brookings Institution, SNAP Cuts in the One Big Beautiful Bill Act Will Significantly Impair Recession Response

- Congressional Budget Office, Estimated Effects of Public Law 119-21 on Participation and Benefits Under the Supplemental Nutrition Assistance Program

- USDA, Supplemental Nutrition Assistance Program Quality Control Review Handbook

- ABC News, Trump Administration Will Partially Fund SNAP, But It Could Take Months

About our contributors

-

Written by Ben Luthi

Written by Ben LuthiBen Luthi is a Salt Lake City-based freelance writer who specializes in a variety of personal finance and travel topics. He worked in banking, auto financing, insurance, and financial planning before becoming a full-time writer.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.