Gold IRAs and Roth IRAs are popular investment vehicles. Depending on your goals and resources, either or both choices may make sense. But when you’re navigating IRS contribution limits or working with limited funds, knowing which type of IRA to prioritize is key.

That decision is easier to make with all-in-one guides like ours. Read on to see how each IRA can affect your finances and what to consider as you weigh your options.

Table of Contents

What’s the difference between a gold IRA vs. Roth IRA?

The primary differences between gold IRAs and Roth IRAs are what comprises each investment account. Depending on what type of gold IRA you choose, the tax treatment could be different, as could your ability to contribute. For example, Roth IRAs and gold Roth IRAs have a modified adjusted gross income (MAGI) limitation, which could reduce the amount or preclude you from contributing to the account.

Take a quick look at how they compare.

| Factor | Gold IRA | Roth IRA |

| Composition | Precious metals | Traditional investments |

| Custodial reqs? | ✔️ | ✖️ |

| Standard contribution limit* | $7,000 | $7,000 |

| Catch-up contribution limit | $1,000 | $1,000 |

| Contributions made… | Pre- or post-tax | Post-tax |

Despite what the name suggests, you can purchase any of the following precious metals through your gold IRA:

- Gold

- Silver

- Palladium

- Platinum

Because gold IRAs consist of physical coins and bullion, these investments come with custodial requirements that Roth IRAs don’t.

Custodial requirements are one of many gold IRA rules and regulations. Precious metals must also meet purity standards to qualify as IRA-eligible.

Per the IRS, you can’t buy or sell your gold IRA holdings without going through your custodian. You also can’t store your precious metals at home. (Even if you could, we wouldn’t recommend it.) Curious about how this looks in practice? Here’s a rundown of how gold IRAs work:

- Open and fund your gold IRA with one of the best gold IRA companies. This company then becomes your IRA custodian.

- Place your first precious metals order with your custodian. Your custodian will facilitate the transaction and go over storage options.

- Select an IRS-approved depository to house your metals. Once you choose a depository and finalize your order, your custodian will coordinate shipping and delivery.

When you open your gold IRA, you can designate it as a traditional IRA or Roth IRA. Each option has distinct tax implications, summarized below:

- Traditional IRA: Contribute with pre-tax dollars, and pay regular income taxes once you start taking distributions.

- Roth IRA: Contribute with after-tax dollars to avoid paying taxes on your distributions.

Why opt for a conventional Roth IRA if your gold IRA offers the same tax benefits? A standard Roth IRA allows for more hands-on account management than a gold IRA.

You can always work with an adviser at your bank or brokerage, but you’re not required to if you prefer to choose your investments on your own.

Furthermore, conventional Roth IRAs hold intangible assets that don’t require storage in controlled environments to retain their value, including:

- Stocks

- Bonds

- Exchange-traded funds (ETFs)

- Target-date funds (TDFs)

- Mutual funds

The similarities and differences between gold and Roth IRAs give way to significant advantages—or disadvantages, depending on your perspective.

Pros and cons of a gold IRA

Like other investments, gold IRAs come with several benefits and a few drawbacks:

Pros

-

Precious metals can add stability to your portfolio.

You’ll often hear gold and other metals described as safe-haven assets. Their value is more likely to remain consistent amidst economic or political crises, which could reduce the impact of market volatility.

-

Enjoy the tax benefits of traditional or Roth gold IRAs.

Gold IRAs are tax-advantaged accounts, just like regular IRAs. Gold IRAs give you greater flexibility at the outset because you can choose whether to treat the account as a traditional or a Roth IRA.

-

You won’t forget to invest your funds.

Believe it or not, many people contribute to standard IRAs without ever picking investments. As a result, their money grows slowly, if it grows at all. However, that’s not a concern with gold IRAs. You’ll have custodial guidance along the way.

Cons

-

Gold IRAs often come with higher fees.

Between transaction fees, storage costs, and shipping charges, gold IRA fees can add up. Roth IRAs aren’t fee-free, but they’re generally less expensive.

-

Gold doesn’t pay dividends.

Precious metals may be less risky than other investments, but they won’t do much to increase your cash flow. If you want to profit from your holdings without selling, a gold IRA may not be the way to go.

Pros and cons of a Roth IRA

Roth IRAs aren’t without their positives and negatives:

Pros

-

The stock market often outperforms gold.

In 2023, the S&P 500 saw a total return of 26.29%, while returns on gold were around 13%. Gold might be a safe-haven investment, but if historical data tells us anything, stocks may offer greater rewards.

-

Roth IRAs are easier to reallocate.

Roth IRAs let you adjust your holdings with a few button clicks or a call to your brokerage. Because these transactions don’t involve physical assets, reallocating a conventional Roth IRA is often faster and simpler than a gold IRA.

-

Your investments grow tax-free.

Long-term tax avoidance is arguably the most significant advantage of a Roth IRA. No matter how much your earnings or tax rate increase, you won’t pay income taxes on the growth of your Roth IRA distributions after age 59½ if the account has been open and funded for at least five years.

Cons

-

No upfront tax break.

To get tax-free qualified distributions, you must sacrifice short-term tax savings. Because Roth IRA contributions aren’t tax-deductible, these investment accounts don’t immediately benefit your bottom line.

-

You can’t buy precious metals.

Purchasing gold or silver bullion isn’t possible with a regular Roth IRA. You can invest in gold ETFs or buy stock in mining companies, but your Roth IRA’s precious metals possibilities end there.

-

Your income could reduce the amount you contribute to the Roth IRA.

It could also prevent you from contributing to one. Income thresholds for 2024 are $161,000 for single individuals and $230,000 for those married and filing jointly. You must earn below those amounts to make direct contributions to your account. (Couples earning more than $230,000 but less than $240,000 may make partial contributions.)

Is a gold IRA or Roth IRA right for me?

Financial benefits and drawbacks are subjective. After all, one investor’s land mine is another’s gold mine. Whether a gold IRA or Roth IRA is best for you hinges on your individual goals, resources, and risk tolerance.

Still, in a few scenarios, one IRA stands out over the other:

| If you… | Consider a… |

| Are nearing retirement age | Gold IRA |

| Have a higher risk tolerance | Roth IRA |

| Can afford a large minimum investment | Gold IRA |

| Want to save on fees | Roth IRA |

| Earn income below the threshold to make direct contributions to a Roth IRA | Roth IRA |

Because precious metals offer risk mitigation and more predictable value retention than other asset classes, a gold IRA may be wise for conservative investors or those nearing retirement.

However, a Roth IRA may be the wiser choice if you have a longer time horizon and are below the income threshold.

When deciding whether a gold IRA is a good investment for seniors, your time horizon is only one factor to consider. You should also weigh your current portfolio’s performance and anticipated distributions.

That’s in part because Roth IRAs do their best work when they have time to grow. Compound interest is a powerful force you want to unleash on your investments as soon as you can.

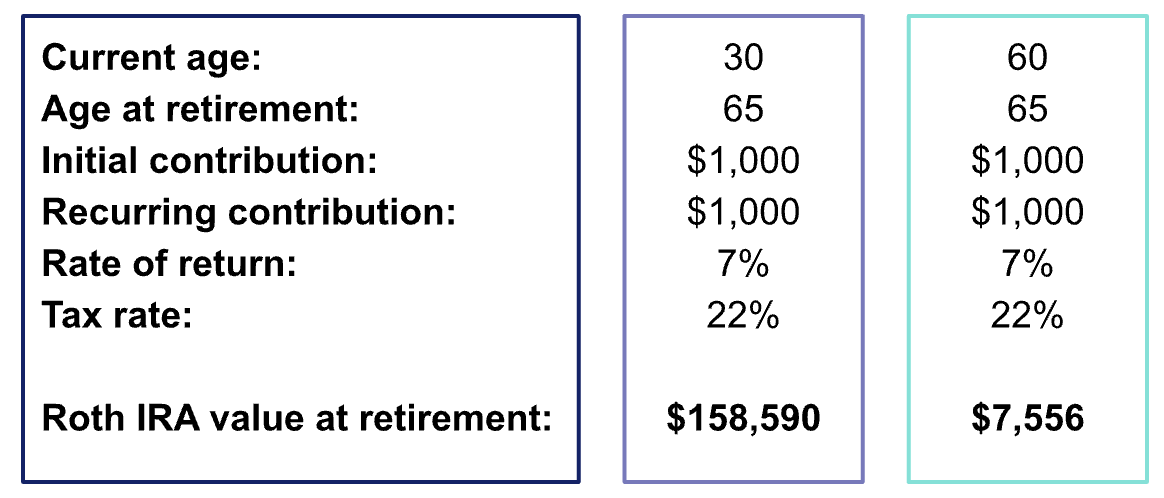

To better illustrate what we mean, say you open a Roth IRA with an initial $1,000 investment. You contribute an additional $1,000 every year until you retire. Here’s how compound interest can affect your finances over different time horizons:

For someone counting down the shifts until their post-work years begin, the stability of a gold IRA may be more appealing than the possible returns on a Roth IRA. However, someone who’s just starting out could potentially gain much more.

Furthermore, as your salary increases throughout your career, your tax rate will increase, and your MAGI could be too high to contribute to a Roth IRA. However, it’s wise to contribute to a Roth IRA when you can; the tax savings you’ll see during retirement far outpace the short-term tax burden.

In addition to their propensity for exponential growth, Roth IRAs have a much lower barrier to entry. Gold IRAs often require hefty initial investments—sometimes requiring an initial rollover or transfer in the $10,000 to $25,000 range. On the other hand, you could open a Roth IRA with as little as $1.

Traditional pre-tax IRA contributions that are not tax-deductible create a cost basis in the account. These contributions should not be taxed upon a qualified withdrawal, and the onus to keep track of the non-deductible contributions is on the account owner (and their CPA if they have one) by filing form 8606.

Erin Kinkade, CFP®

The initial requirements of many gold IRA providers are in the form of rollovers or transfers from a retirement account. The same annual contribution limits that apply to traditional IRAs apply to gold IRAs.

If you have a low risk tolerance, can absorb the fees, have other diversified assets, and your income is too high to contribute to a Roth IRA, I might recommend a gold IRA. In more cases, I would recommend contributing to a Roth IRA if you’re under the income threshold, don’t need an immediate tax deduction, have a higher risk tolerance by being comfortable investing in the market (in any asset allocation), and are projected to be in a higher tax bracket during retirement when withdrawals are needed or required.

Erin Kinkade, CFP®

Should I have both a gold IRA and a Roth IRA?

Open multiple IRAs could work to your advantage, particularly if your gold IRA functions as a traditional IRA. Here’s why:

- Your gold IRA could reduce your present-day tax liability.

- Your Roth IRA would give you a tax break on the back end.

- You stand to benefit from the potential higher return from stocks, bonds, and mutual funds.

- The relative stability of your precious metals holdings could balance your portfolio’s overall risk.

Remember, you’ll still be working within IRS contribution limits, which don’t change whether you have two or 10 IRAs.

For example, imagine you’re 51 years old during the 2024 tax year and can contribute $8,000. You might divide that $8,000 evenly between your IRAs. You could also split it 60/40, 70/30, or even 95/5. However you slice it, your combined contributions can’t exceed $8,000.

You could argue for maintaining multiple IRAs, but juggling competing IRAs also adds a layer of complexity (and an extra set of account fees) you may not want to deal with. Before you decide, compare gold IRAs and 401(k)s to see whether this duo is a better fit for you.

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.