Need ongoing access to fast cash? Home equity lines of credit (HELOCs) let you convert your equity into a revolving credit line. HELOCs often come with higher limits than credit cards, making it all the more important to secure the best rate possible.

The lower your rate, the less expensive your borrowing cost. We’ve selected these as the three best online HELOCs for Idaho homeowners. They offer competitive rates, quick applications, and innovative features. We also researched several competitive local lenders to help you compare. Keep reading for our recommendations.

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

|

Best overall |

|

|

|

Best credit union |

|

|

|

Best marketplace |

|

Reviews of the best online HELOCs in Idaho

An online HELOC enables you to apply for and manage your credit line right from your device. Many provide near-instant decisions, and a few even offer virtual appraisals. For a tech-driven HELOC couched in convenience, look no further than these three lenders:

Figure

Why we picked it

Figure stands out for its seamless online application process and efficient use of blockchain technology to streamline HELOC transactions. Its transparent approach and competitive rates make it a strong contender for those looking for a quick and efficient HELOC option in Idaho.

- Fixed interest rates

- No in-person appraisal is needed

- Option to redraw up to 100% of funds

- Funding can be available in as few as 5 days

- Check your rate without affecting your credit score

Loan details

| Rates (APR) | 6.55% – 15.54% |

| Loan amounts | $20,000 – $750,000 |

| Draw period | 5 years |

| Repayment term | 5, 10, 15, or 30 years |

| Funding time | As few as 5 days |

| Properties | Primary home, second home, or investment property |

| Credit score | 640 |

FourLeaf

Why we picked it

We like FourLeaf Federal Credit Union for its member-centric approach and competitive HELOC rates. As a credit union, it may provide better terms and customer service than many traditional banks, which can benefit homeowners in Idaho seeking reliable financial services.

- Borrow $10,000 – $1 million

- No application, origination, or appraisal fees

- Convert part of your HELOC to a fixed-rate option

- 12-month fixed introductory rate for qualified borrowers

- $0 closing costs

Loan details

| Rates (APR) | 6.99% for 12 months, then variable |

| Loan amounts | $10,000 – $1 million |

| Draw period | 10 years |

| Repayment term | 5, 10, or 20 years |

| Funding time | 36 to 70 days, on average |

| Properties | Primary homes, second homes, or condos |

| Credit score | 670 |

LendingTree

Why we picked it

LendingTree is the best marketplace for HELOCs in Maine due to its extensive network of lenders. This platform enables homeowners to compare multiple offers, empowering borrowers to find the best rates and terms tailored to their specific needs. This makes financing home projects or managing debt easier in the diverse Maine real estate landscape.

- Access to multiple lenders

- Comprehensive comparison tools

- Competitive rates

- Customizable loan options

Loan details

| Rates (APR) | Starts at 6.99% |

| Loan amounts | $10,000 – $2 million |

| Draw period | 2 – 20 years |

| Repayment term | 5 – 30 years |

| Funding time | Varies by lender |

| Properties | Varies by lender |

| Credit score | Varies, 620 advisable |

Local HELOCs in Idaho

Cutting-edge technology is no replacement for a human touch. If you prefer a greater degree of interaction or want to support a local business, these Idaho credit unions may be just what you’re looking for:

| Company | Rates (APR) | Location |

| Clarity Credit Union | 9.25% – 18.00% | Boise Metropolitan Area |

| Lewis Clark Credit Union | 7.50% – 18.00% | Clearwater and Nez Perce Counties |

| Westmark Credit Union | 10.00% – 18.00% | Southern Idaho |

As you evaluate these Idaho-based lenders, it may be helpful to weigh them based on the following criteria:

- Membership eligibility: First, make sure you qualify for credit union membership. For many credit unions, membership is often based on where you live or work or whether you’re related to a member.

- Interest rates: Many HELOCs come with variable rates, meaning they could (and likely will) increase or decrease over time. Be sure you understand how this can affect your monthly payments if you’re considering a variable-rate HELOC.

- Funding speed: Getting a HELOC can take anywhere from a few days to a few weeks. Ask potential lenders how long it typically takes to open a HELOC with them. Use that to guide your decision, particularly if you need your HELOC for a time-sensitive purchase.

While you’re at it, have your lender clarify which HELOC fees you’re responsible for and whether it pays any on your behalf.

Westmark Credit Union, for example, takes care of appraisal and title insurance costs on HELOCs less than $75,000. The tradeoff is that you must reimburse Westmark if you pay off your HELOC within three years.

What’s the difference between online and local HELOCs in Idaho?

The primary difference between online and local HELOCs is how much you’ll rely on technology to manage your HELOC and communicate with your lender.

With an online HELOC, your experience will be fully digital. Local HELOC lenders generally blend technology with tradition. Here’s a quick look at what you can expect from each option:

| Online | Local | |

| Support options | Phone, chat, email | In-person, phone, chat, email |

| After-hours support? | Often | Sometimes |

| Service area | Multi-state | Regional |

| Physical locations? | ✖️ | ✔️ |

Both types of HELOC offer advantages and disadvantages, but in some cases, one will make more sense than the other. The table below can help you decide which is best for you.

| If you… | Consider… |

| Prefer self-service account management | Online HELOC |

| Aren’t comfortable using apps or web tools | Local HELOC |

| Need 24/7 account access | Online HELOC |

| Want to visit a physical location | Local HELOC |

| Travel often | Online HELOC |

| Have a relationship with a local lender you’re happy with | Local HELOC |

Beyond these scenarios, consider how much you can borrow with your HELOC and at what rates. Even if you’re set on a particular type of HELOC right now, being flexible could result in a higher credit line or lower rate.

How do Idaho HELOC rates compare to other states?

You, your friend in Utah, and your sister-in-law from Oregon may all qualify for different HELOC rates. But this isn’t because of where you live. HELOC rates aren’t location-specific, so rate variability often comes down to borrowers’ credit scores.

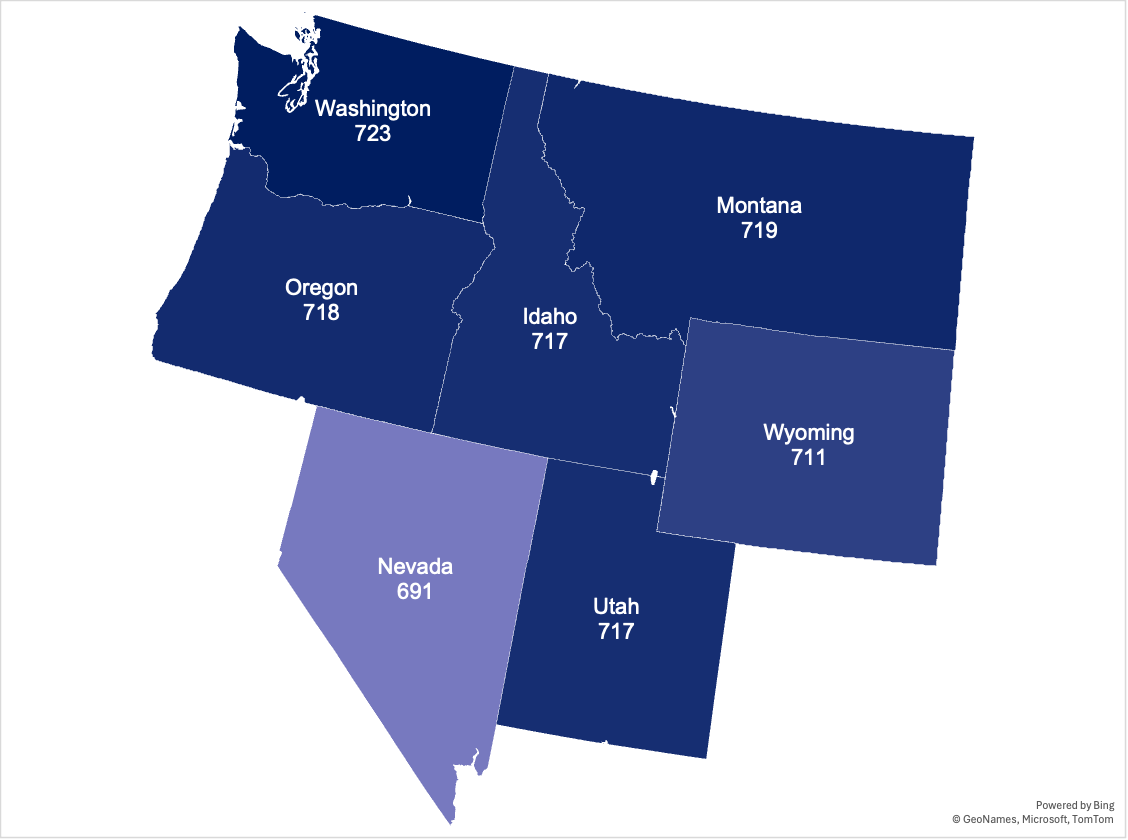

To be fair, credit scores can fluctuate by state thanks to differences in cost of living and earning potential. These are the average VantageScores in Idaho and its neighboring states as of April 2024:

Notice that, with the exception of Nevada, little variation exists between these state averages. We can assume, then, you won’t see much variation in average HELOC rates by state either.

How to get the best HELOC rates in Idaho

The state you live in doesn’t have much impact on your HELOC rate, but these three factors do:

- The prime rate

- Your credit score

- Your lender

Think of the prime rate as a benchmark. It changes based on the broader economy, and when it changes, lenders adjust their interest rates too.

You don’t have any control over the prime rate, but you can influence your credit score. To give yourself the best chance at a low HELOC rate, try these credit-boosting tips:

- Keep your credit card balances at no more than 30% of your credit limit.

- Catch up on any past-due accounts.

- Avoid opening new accounts before applying for a HELOC.

No matter your credit score, it’s not uncommon to qualify for different rates from different lenders. One lender might offer a 7% rate, and another may quote a 9% HELOC rate for no reason other than how each one calculates rates and risk.

That’s why we recommend prequalifying with multiple lenders before you apply for a HELOC.

Compare the rates, HELOC limits, and borrower benefits each lender offers, and then choose the right lender for you. It’s more work on the front end, but it’s a step you shouldn’t skip if you want the best rate possible on your HELOC.

Are there any Idaho-specific requirements or regulations?

While you research HELOCs, ask lenders about any borrower requirements, such as carrying homeowners insurance. Idaho law doesn’t have many homeowner regulations, but your lender may have its own stipulations.

As you talk to lenders, take note of each one’s transparency and customer service quality. Idaho doesn’t offer many special consumer protections, so you’ll need to vet lenders carefully.

If you change your mind about a lender, the federal right of rescission (or three-day rule) lets you cancel your HELOC within three days of signing.

Idahoans now have financial recourse if they fall behind on their property taxes. Beginning July 1, 2024, if your county repossesses and sells your home, you could be entitled to a share of the proceeds.

Your HELOC lender may step in and pay back taxes on your behalf, but this will likely increase your HELOC balance. If you anticipate late property-related payments, work out a plan with your county and your lender as soon as possible.

FAQ

What credit score do you need for an Idaho HELOC?

Each lender will have specific criteria, but most lenders in Idaho require a minimum credit score of 620 to qualify for a HELOC. However, a higher credit score (700 or above) can help you secure better rates and terms.

What are the typical fees for an Idaho HELOC?

Typical fees for an Idaho HELOC may include:

- Application fee: $100 – $500 (sometimes waived)

- Origination fee: 0% – 2% of the loan amount

- Annual fee: $50 – $75

- Closing costs: $500 – $2,000

- Appraisal fee: $300 – $600

Some lenders may waive or reduce these fees as part of promotional offers, so be sure to inquire about fee structures when comparing HELOC options.

Are there any special programs or incentives for Idaho HELOCs?

Yes, some lenders offer special programs or incentives for Idaho residents. These can include lower introductory rates, reduced fees, or discounts for certain groups such as veterans, teachers, or first responders. Credit unions may also offer member-specific benefits. It’s important to ask lenders about any special programs or incentives that may apply to you.

What happens if I move to another state with a HELOC in Idaho?

If you move to another state while you have a HELOC in Idaho, your HELOC remains tied to your Idaho property. You’re still responsible for making payments according to the terms of your HELOC agreement.

If you sell your Idaho home, you will typically need to pay off the remaining balance of your HELOC from the proceeds of the sale. Always check the specific terms and conditions of your HELOC agreement. Some lenders may have additional requirements or stipulations for relocation.

How we chose the best HELOCs in Idaho

Since 2018, LendEDU has evaluated home equity companies to help readers find the best home equity loans and HELOCs. Our latest analysis reviewed 850 data points from 34 lenders and financial institutions, with 25 data points collected from each. This information is gathered from company websites, online applications, public disclosures, customer reviews, and direct communication with company representatives.

These star ratings help us determine which companies are best for different situations. We don’t believe two companies can be the best for the same purpose, so we only show each best-for designation once.

Recap of online Idaho HELOC rates and lenders

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

|

Best overall |

|

|

|

Best credit union |

|

|

|

Best marketplace |

|

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.