A home equity line of credit (HELOC) is a revolving credit line secured by your home equity. Equity is the difference between what your home is worth and what you owe on the mortgage. You sign a HELOC note when you take cash out of a home equity line of credit.

What is a HELOC note? Like any other promissory note, it creates a legal agreement obligating a borrower to repay a debt to a lender.

Signing off on a HELOC promissory note conveys responsibilities to you as the borrower and extends rights to the lender. Both are important if you’re considering a home equity line of credit.

Advertisement

While many HELOC lenders advertise minimum credit scores around 640, approvals typically go to borrowers with scores closer to 720 or higher. If your credit is lower and you need fast funding, home equity agreements or other alternatives may be easier to qualify for.

Why is a HELOC note important?

Like other promissory notes, a HELOC note details the specifics of the loan. A HELOC note is legally binding, meaning once you and the lender sign, you’re both obligated to uphold the terms of the document.

Critical information in a HELOC promissory note includes the following:

- Line of credit amount

- Draw period terms

- Repayment requirements

- Interest and fees

Those are all important to know as a borrower. You want to be aware of how much credit you can access and when you’ll need to start paying it back.

A HELOC note can also specify what recourse the lender has if you default on repayment. For example, it might state that a lender can place a lien on the property that secures the line of credit. Liens prevent you from selling or refinancing the property until the debt associated with the lien is paid.

Who creates a HELOC promissory note?

The lender creates a HELOC note, which you sign at closing, along with other required documents. You should have an opportunity to review the note before signing it.

Lenders reserve the right to change a HELOC promissory note after the document is signed but only in certain circumstances. For instance, if you or the lender find typos, the lender can update the note to correct them.

However, the lender can’t change the terms of the agreement itself without getting your consent in writing. Even if your lender sells your mortgage to another lender, the new lender must uphold the terms in the original note.

What does a HELOC note look like?

HELOC notes may look different, depending on where you’re getting a home equity line of credit. You may see this document for the first time at closing once the terms of the HELOC are final.

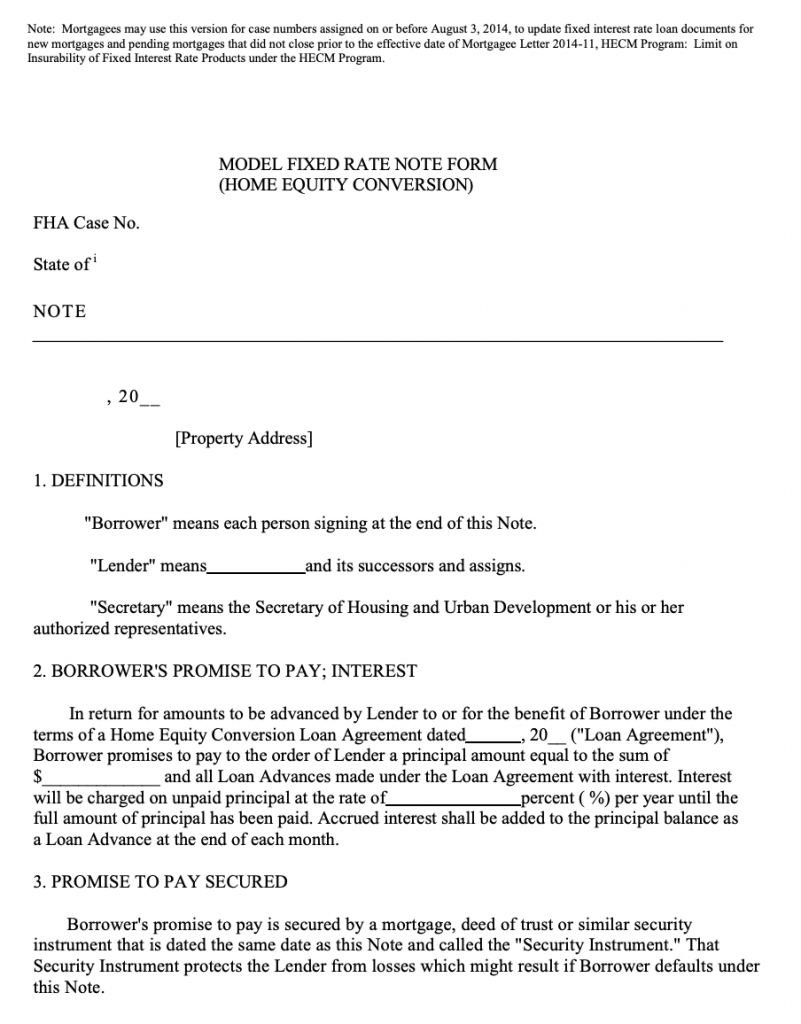

We found an example of a model note the U.S. Department of Housing and Urban Development (HUD) uses when it backs home equity conversion mortgages:

Your form might look different, but the one you sign should look like a contract. A spot may be at the top for the date and property address. You should also see words such as “Promissory Note” or “Home Equity Note” at the top of the document.

The example note above specifies:

- Borrower’s promise to pay

- Interest rate on the loan

- Which property secures the line of credit

- Manner of payment the lender requires

- Borrower’s right to prepay

- When payment is due in full

- Waivers and when notice is required

- Borrower obligations

The form leaves room for the borrower and the lender to sign, making the agreement fully binding. Your HELOC note might look different depending on the lender, but the structure and elements included should be the same.

Important sections of a HELOC note

A HELOC note includes several pieces of important information for lenders and borrowers. That information is typically grouped into sections to make it easier to find. Understanding these sections can be helpful as you read through your HELOC agreement.

| Section | What it is |

| Definitions | Explains important terms |

| Loan amount & interest | Details about your specific loan |

| Repayment terms | How much you can expect to pay and when payments are due |

| Prepayment options | Guidelines for early repayment |

| Other restrictions | Additional terms and conditions |

Definitions

Your HELOC note may include a section that explains terms used throughout the document. The “definitions” section might be at the beginning or end of the note.

For example, you might see the following terms listed:

- “Borrower,” the person getting the HELOC.

- “Property,” the property that secures the line of credit.

Loan amount and interest

A HELOC note should also include details about the line of credit the lender is extending and the interest rate you’ll pay. The maximum line of credit depends on the lender and how much equity you have. Bank of the West, for example, offers eligible borrowers HELOCs of up to $2 million.

Most HELOC rates are variable. Your note should explain when that rate can adjust, as well as periodic and lifetime rate caps. Periodic rate caps determine how much your rate can increase from one adjustment period to the next. Lifetime rate caps specify how much your rate can rise over the life of the loan.

There may be additional wording if you have a variable rate during the draw period and a fixed rate in repayment. For example, Regions Bank offers an introductory APR of 0.99% for variable-rate HELOCs and then converts it to a fixed rate.

Repayment terms

The “repayment terms” section explains when payment is due on a HELOC and how much you can expect to pay. In a typical HELOC agreement, you have an initial draw period of five to 10 years in which you can access your credit line. Once that ends, you enter the repayment period, which could last 20 years.

During the draw period, you may only be required to make interest payments, but your lender might allow you to pay toward the principal. Once the repayment period begins, you’ll pay both principal and interest.

Prepayment options

You may pay off your HELOC balance before the draw period ends. Prepayment could save you on interest charges but cost you fees if the lender charges a prepayment penalty.

Your HELOC note should include a section detailing the guidelines for prepayment, including whether a penalty applies. You can also find information about what happens if you miss payments and when payment is due in full.

For example, the lender may assess a late fee if you miss a payment. Missing multiple payments could lead to default. At that point, the lender might be able to take the next steps to collect what you owe, which could include foreclosure actions.

Other restrictions

This section can include restrictions or other terms and conditions that affect your rights and responsibilities.

For example, you might see language specifying:

- When the lender has the right to resell your HELOC note.

- Payment due in full should you decide to sell the home.

- Restrictions on third-party information disclosures.

A thorough review of this section is essential to avoid any unpleasant surprises.

For example, if you buy another home that becomes your principal residence and decide to rent out the house that has the HELOC, the note might give your lender permission to request full payment due.

What to look out for in a HELOC note

The HELOC note might be short, but it carries significant legal weight.

As you read through your HELOC note, keep an eye out for the following:

- Typos, spelling mistakes, or other errors in your personal information.

- Errors in the property information, such as a transposed number in the address.

- Legal terms you don’t recognize or understand.

- Loan details that differ from what you expected (i.e., surprise fees or a higher rate).

If you need clarification on any loan terms, it’s best to ask the lender before you sign. Once you sign the HELOC note, it becomes legally binding, which could make resolving misunderstandings more difficult.

About our contributors

-

Written by Rebecca Lake, CEPF®

Written by Rebecca Lake, CEPF®Rebecca Lake is a certified educator in personal finance (CEPF®) and freelance writer specializing in finance.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.