Find old 401(k) accounts

- Uses technology to find old 401(k) accounts

- Helps roll over IRAs

- Shows hidden fees within retirement accounts

- Offers 401(k) loans

- Excellent Trustpilot ratings

- Monthly subscription free

- Additional fees for other services

- Offers advice from “money coaches,” not Certified Financial Planners®

- Some users report difficulty with customer service

| Available services | Find old 401(k) accounts, Account rollovers, See 401(k) fees, 401(k) loans |

| Costs | Start at $4.99/month |

| Best for | Busy professionals, employees who have switched jobs numerous times |

If you’ve changed jobs recently and are confused about what to do with your 401(k), there’s a company that can help. Beagle IRA is a fintech company that acts as your financial concierge. Not only does it help you track down old 401(k)s, but it can roll over your old accounts into an IRA.

Although people can search for their old 401(k)s themselves, seriously, who has the time for that? That’s why so many people let Beagle do that research for them. Here is more information about what Beagle is, how it works, and the pros and cons of using the service.

What is Beagle?

Beagle is a 100% online platform that uses technology to track down your old retirement accounts. Its research technology scours databases and websites to find long-forgotten 401(k)s. If you find it surprising that people forget about 401(k)s, it’s more common than you might think.

According to data from Capitalize, there are nearly 32 million 401(k) accounts that workers have either left behind at old jobs or forgotten about. This usually happens when you switch jobs or get laid off. And when those things happen, the to-do list is usually so long that rolling over a 401(k) gets put on the back burner.

If you’re not sure whether you’ve left a 401(k) behind at an old job, Beagle can find out for you. It also provides guidance on transferring your 401(k) into a new workplace plan or rolling it over into an IRA. Beagle offers its own IRA if you don’t have one; it’s a qualified broker. Beagle also offers 401(k) loans.

What Beagle helps you do

Beagle can do the following:

- Conduct research to find your old 401(k) accounts.

- Show you the hidden fees you’re paying in your retirement accounts. The Department of Justice says the fees in 401(k) accounts can reduce investment growth and, by extension, your retirement income, so it’s a helpful service.

- Roll over your 401(k) to an account at your new employer or into one of Beagle’s IRAs.

- 0% 401(k) loans. You can borrow up to half of your retirement balance with a maximum of $50,000. Even though Beagle’s 401(k) loans carry 0% net interest, fees are associated with setting one up.

How Beagle works

It’s straightforward to use Beagle. Here’s how it works in a few steps.

Step 1: Create an account

For Beagle to search for old 401(k)s, you’ll need to provide your personal information, including your Social Security number, phone number, and work history.

Step 2: Review your fee report

Beagle shows you the cost of your 401(k) fees so you can see how they affect your overall financial plan.

Step 3: Roll over your account

If you choose to, you can roll over your old 401(k) accounts into a Beagle IRA in just one click. Unlike some competitors, Beagle uses e-signatures and makes phone calls on your behalf.

Step 4: Take out a 401(k) loan (if you choose)

Beagle stands out from competitors for offering 0% net-interest 401(k) loans. However, the biggest downside of any 401(k) loan is that the money you borrow is temporarily removed from the market, so it can’t grow or compound while the loan is outstanding.

Traditional 401(k) loans typically charge interest (often prime plus 1%), but you pay that interest back into your own retirement account. Because of this, a 0% loan doesn’t necessarily make borrowing cheaper. Your real cost is the lost investment growth while the funds are out of your account.

Beagle IRA fees and pricing

Beagle earns money through monthly subscription plans. Each plan includes a three-day free trial and provides tools to locate old 401(k) accounts. Higher-tier plans add concierge support and financial coaching.

| Plan | Monthly price | What you get |

|---|---|---|

| Starter | $4.99* | Shows three accounts from the initial search and includes a manual search to help locate additional accounts. |

| Standard | $6.99 | Includes everything in the Starter plan plus concierge help to access old 401(k) accounts and assistance with rollovers or consolidation. |

| Premium | $14.99 | Includes everything in the Standard plan plus a session with a financial coach to review your finances and identify savings opportunities. |

401(k) loan fees

If you use Beagle’s 401(k) loan feature, additional fees apply:

| Fee type | Cost |

|---|---|

| Loan setup fee | $99 |

| Monthly maintenance fee | $2 |

Beagle advertises a satisfaction guarantee, and you can cancel your subscription at any time by emailing [email protected].

Is Beagle legit?

Yes, Beagle is a legitimate company that was founded in 2020. The thousands who left reviews on Trustpilot are overwhelmingly positive about their experience.

| Source | Customer rating | Number of reviews |

|---|---|---|

| Trustpilot | 4.8/5 | 2,705 |

| Better Business Bureau | 1.0/5 (B rating, not accredited) | 20 |

According to the Better Business Bureau, Beagle Financial Services has received 51 customer complaints in the last three years, with 32 complaints closed in the last 12 months at the time of our review. The company is not BBB accredited.

In many complaints, Beagle responded publicly, issued refunds, or attempted to resolve the issue. However, the complaints indicate that some users experienced confusion about pricing, account results, or the account-linking process.

As with most consumer services, BBB complaints represent individual customer experiences and may not reflect the experience of every user.

Pros and cons

Beagle offers tools to help locate old retirement accounts and roll them into an IRA, but the service also comes with subscription costs and mixed customer feedback.

Pros

-

Uses technology to find old 401(k) accounts

Beagle searches retirement account databases and records associated with past employers to help users locate forgotten or inactive 401(k) accounts.

-

Helps with IRA rollover

The platform provides concierge assistance to help move funds from an old 401(k) into a new or existing IRA.

-

Shows hidden fees within retirement accounts

Beagle analyzes retirement plans to identify administrative and investment fees that could reduce long-term retirement growth.

-

Offers 401(k) loans

Eligible users may be able to borrow against their retirement balance through Beagle’s loan service without triggering taxes or early withdrawal penalties.

-

Excellent Trustpilot ratings

Beagle has a high Trustpilot rating based on thousands of customer reviews, with many users reporting success in locating old retirement accounts.

Cons

-

Monthly subscription free

Beagle charges a monthly subscription fee to access its account search tools and concierge services.

-

Additional fees for other services

Certain services, such as Beagle’s 401(k) loan feature, include extra costs, including a $99 setup fee and a $2 monthly maintenance charge.

-

Offers advice from “money coaches,” not Certified Financial Planners®

The premium plan includes financial coaching, but the advisors are not licensed CFPs®.

-

Some users report difficulty with customer service

A number of customer reviews and BBB complaints mention

delays in responses or difficulty resolving billing issues.

Who is Beagle best for?

Beagle is best for busy professionals who have changed jobs numerous times over the past few years. It’s especially good for people who know they have old 401(k) accounts but, due to their current jobs and other responsibilities, do not have the time to research and find them on their own.

Beagle is not ideal for people who need specific retirement or investment advice. It only includes a money coach with the highest-level subscription. It’s also not worth it for people who know where their 401(k) retirement accounts are. Using the service only for a loan or financial advice is not worth the recurring subscription fee.

How to get started

Here’s how to use Beagle.

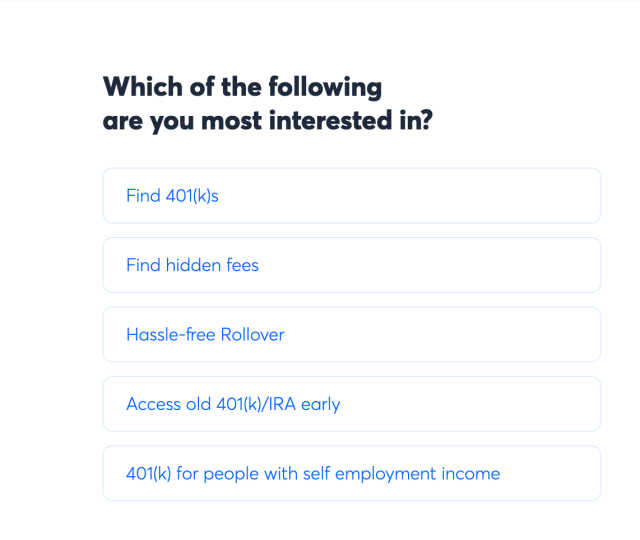

- Navigate to the MeetBeagle website, and click the blue Get Started button.

- Answer the question on the next page, which asks about the products or services you need. For example, you can choose “Find 401(k)s” or “Hassle-free Rollover”.

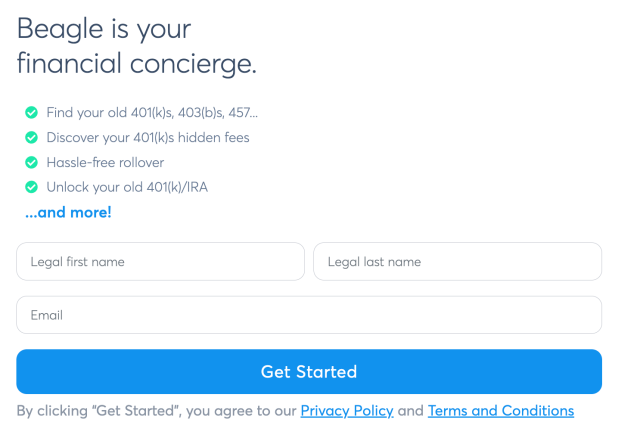

- Enter your first and last name and email, and click the blue Get Started button. That will create your Beagle account, allowing you to log in and choose a subscription.

Other ways to find old 401(k)s

If you want to find your old 401(k), you can do it on your own, but it will take some time.

- You can contact your old employers and speak to the HR department. They can point you in the right direction by telling you how to locate your old 401(k) plan.

- You can also search the Department of Labor’s abandoned plan database and the National Registry of Unclaimed Retirement Benefits. These are databases that keep records of unclaimed retirement plans with remaining balances.

- Beagle also has competitors like Capitalize. Capitalize also helps customers with 401(k) rollovers and finding old accounts but doesn’t offer 401(k) loans. If you use a brokerage firm, many will also help you roll over an old 401(k) if you open an IRA there.

Article sources

At LendEDU, our writers and editors rely on primary sources, such as government data and websites, industry reports and whitepapers, and interviews with experts and company representatives. We also reference reputable company websites and research from established publishers. This approach allows us to produce content that is accurate, unbiased, and supported by reliable evidence. Read more about our editorial standards.

- Capitalize, The True Cost of Forgotten 401(k) Accounts (2025)

- Department of Justice, A Look at 401(k) Plan Fees

- Department of Labor, Abandoned Plan Search

Related articles

About our contributors

-

Written by Catherine Collins

Written by Catherine CollinsCatherine Collins is a personal finance writer and author with more than 10 years of experience writing for top personal finance publications. As a mother to boy/girl twins, she is passionate about helping women and children learn about money and entrepreneurship. Cat is also the co-host of the Five Year You podcast.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.