LendEDU’s Take

Aven Home Equity Cash is a strong HELOC option for borrowers who want stability. With fixed rates, predictable payments, and structured repayment, it’s easier to manage than more flexible alternatives. It’s also our pick for best HELOC for customer reviews, reflecting consistently positive borrower feedback.

Rates (APR)

6.99% – 15.49% (fixed)

Loan Amounts

$5,000 – $400,000 ($100,000)

Min. Credit Score

640 (but 720+ recommended)

What borrowers like

- Offers lowest rate guarantee

- Approval in as little as 15 minutes

- Excellent customer reviews from thousands of customers

- 100% digital application process

- Increases the credit line for select customers

- Automated appraisals

- High maximum loan-to-value ratio (LTV)

- Three-day funding after signing

- Fixed interest rates

- Check your rate with no credit impact

Things to keep in mind

- Short draw period

- Full HELOC must be drawn at origination

- First-draw fee of 4.90%

- Only available in 32 states

LendEDU’s Take

The Aven Home Equity Visa Card offers flexible, on-demand access to your equity with HELOC-like rates. While convenient, its revolving structure can make repayment less predictable. It’s best for borrowers who want ongoing access to funds rather than a fixed repayment plan.

Rates (APR)

7.99% – 15.49% (variable)

Limit Amounts

Up to $400,000

Annual Fee

$0

What borrowers like

- Easy online process

- Lower rates than typical credit cards

- High credit limits

- No appraisal or origination fees

- You only borrow what you need

- Unlimited 2% cash back

Things to keep in mind

- 2.5% fees on cash and balance transfers

- Risk of overspending due to card convenience

- Credit limit may be reduced if inactive

- Daily and monthly transfer limits

Aven is a fintech lender offering fast, fully digital ways to tap home equity. Its two main products are the Aven HELOC (Aven Home Equity Cash) and the Aven Home Equity Visa Card, both designed for quick approvals, automated appraisals, and a streamlined online process.

While both provide convenient access to equity, the Aven HELOC is the better fit for most borrowers. Its fixed rates and predictable repayment structure make it more suitable for larger or longer-term needs. The Aven card offers flexible, swipeable access at lower-than-typical credit card rates, but it requires more discipline. For most homeowners, the HELOC is the safer, more practical choice.

Aven HELOC review

Rates, terms, and costs

Aven’s Home Equity Cash HELOC lets you access your equity with a fully online process, remote closing, and funding in as little as three business days. Each draw is converted into a fixed-rate plan with predictable monthly payments, giving you more structure than a typical HELOC.

There are no application or appraisal fees, but Aven charges a 4.90% first-draw fee at closing, similar to an origination fee on the initial amount borrowed.

Here’s a snapshot of Aven’s key HELOC terms:

| Terms | Details |

| Rates (APR) | 6.99% – 15.49% fixed |

| HELOC amounts | $5,000 – $400,000 ($100,000) |

| Minimum draw amount | Full HELOC amount |

| Draw period | 5 years |

| Term lengths | 5, 10, 15, or 30 years |

| Origination (first-draw) fee | 4.90% |

| Application fee | $0 |

| Unique features | Automated appraisals; lowest rate guarantee; foreclosure protection program; credit line increases for select customers |

Example: Costs and fees of Aven’s HELOC

You won’t pay many fees with Aven, but its HELOC isn’t entirely fee-free. While Aven doesn’t charge application or appraisal fees, it does levy a 4.90% first-draw fee, which is essentially an origination fee. Aven also assesses a $29 late fee on its home equity card, though it’s unclear if this applies to Aven Home Equity Cash.

However, fees are only one piece of the HELOC affordability puzzle. These fees work in tandem with your interest rate to create your annual percentage rate (APR). Your APR reflects the true premium you pay for your credit line, so locking in the lowest possible APR is imperative.

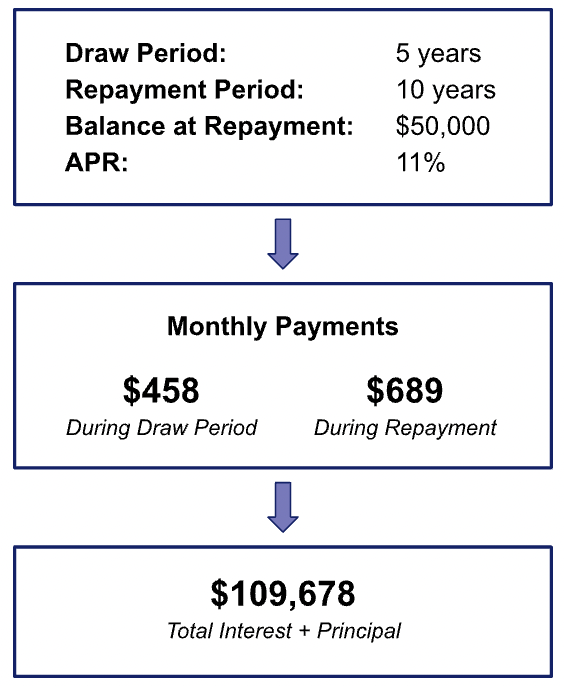

To better illustrate how APR can influence your borrowing cost, let’s say that you withdraw $50,000 from your HELOC at an 11% APR. Here’s how much your HELOC would cost over time:

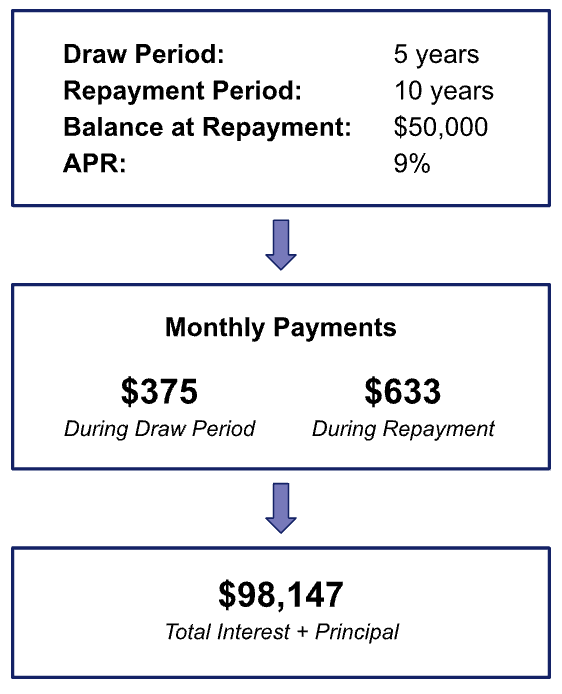

What started as a $50,000 balance ballooned into a six-figure price tag because of your 11% APR. But what if you held out for a better rate and qualified for a 9% APR instead? How might that change your payments and overall borrowing cost?

If we look just at your monthly payments, particularly your payments once your draw period ends, it’s easy to miss how influential your APR really is.

However, we can see your APR’s cumulative impact when we zoom out. Not only are your monthly payments more affordable at the lower rate, but you’ve also saved $11,531 over the life of your HELOC.

Once you understand the basic terms and how your costs can vary based on your APR, it helps to look at how Aven’s process works in practice. Below are the core features that shape the Aven Home Equity Cash experience from application to funding to repayment.

Key features

Aven’s HELOC is built for speed and simplicity, with a fully digital process and flexible borrowing structure:

- Built-in protections and perks: Includes a lowest-rate guarantee, hardship support, and the option to refinance existing second-lien debt.

- 100% online experience: Apply, verify income, complete your appraisal, and close with a remote notary—no in-person steps required.

- Fast approvals and funding: Get prequalified in seconds, close quickly, and access funds in as little as three business days.

- Fixed-rate draws: Each withdrawal converts into a fixed-rate plan with predictable monthly payments.

- Low fees: No application, appraisal, redraw, or prepayment fees (though a 4.90% first-draw fee applies).

- Flexible access to funds: Draw as needed during the five-year draw period, with potential credit line increases over time.

- Streamlined requirements: Automated income verification and minimal insurance documentation in most cases.

Read More What is a home equity line of credit?

Aven HELOC requirements

Qualifying for an Aven HELOC comes down to three main factors: your credit profile, your available equity, and the state you live in. Like most home equity lenders, Aven wants to see that you can manage additional debt and that your home has enough value to support the credit line you’re requesting.

Aven also allows joint applications, which can be helpful if a co-borrower—such as a spouse—has a stronger credit profile.

Below is a closer look at Aven’s eligibility and residency requirements:

| Requirements | Details |

| Eligible properties | Primary residences and investment properties |

| State of residence | Alabama, Alaska, Arizona, Arkansas, California, Colorado, Florida, Iowa, Illinois, Kansas, Kentucky, Louisiana, Maine, Michigan, Minnesota, Mississippi, Nebraska, New Hampshire, New Jersey, New Mexico, North Carolina, North Dakota, Ohio, Oklahoma, Oregon, Pennsylvania, South Dakota, Tennessee, Utah, Virginia, Wisconsin, Wyoming |

| Maximum loan-to-value (LTV) | 89% |

| Maximum debt-to-income | Not disclosed |

| Minimum credit score | 640 |

| Minimum income | Not disclosed |

Aven credit score requirement: 640, but 720+ recommended

Although Aven lists 640 as its minimum credit score, applicants with scores below 720 may have a much lower chance of approval. In practice, borrowers with scores of 720 or higher tend to see stronger approval odds, better rates, and higher credit limits. If your score is below that threshold, you may want to consider alternatives before applying.

LTV up to 89%

Aven’s underwriting also weighs your home’s value and available equity. This is where your loan-to-value ratio (LTV) comes in. LTV measures how much you owe on your home compared to what it’s worth.

Aven allows a combined LTV of up to 89%, meaning your mortgage plus your new HELOC can’t exceed 89% of your home’s value. Lower home values or lower equity levels may result in smaller credit limits or higher rates.

Here’s an example of how LTV affects how much you may be able to borrow:

LTV example

Say, for instance, that you owe $150,000 on a $300,000 home. Here’s how Aven might calculate how much you can borrow with a HELOC in light of its LTV threshold:

But what if Aven determined your home value to be slightly higher? Take a look below to see how much more you could borrow if your home appraised at $325,000 instead:

In our first example, $117,000 was the largest HELOC you could get without surpassing the 89% cap. With the increased property value in our second example, your potential HELOC limit went up by $22,250.

Before you rush to remodel your kitchen, we should mention that virtual appraisals don’t always capture improvements like these. That’s because these appraisals rely on tax data and recent selling prices of nearby homes, not necessarily a physical examination of your property.

Rather than investing in renovations you weren’t otherwise planning, you may see better results—both to your HELOC limit and your long-term financial position—by reducing your mortgage balance instead.

No property-type restrictions

Aven is flexible when it comes to property type. It considers primary residences, second homes, investment properties, new construction, and even homes held in a trust—something not all HELOC lenders allow.

Aven HELOC pros and cons

Pros

- High maximum LTV

- Aven’s 89% LTV threshold makes its HELOC more accessible to more homeowners. It also means you could open a larger HELOC than you’d qualify for elsewhere.

- Fixed rates

- With Aven, your HELOC rate will never change, so you’ll know what to expect month after month.

- Few fees

- Unlike some of its competitors, Aven doesn’t charge application, appraisal, or notary fees. You won’t pay an annual fee, either.

- Customizable repayment options

- Aven offers four different repayment periods, and you can choose the term that best suits your finances.

- Completely virtual application and appraisal

- You’ll forego the time and hassle of scheduling a traditional appraisal with Aven. You could apply and get approved in as little as 15 minutes.

- Unique borrower benefits

- From its lowest rate guarantee to its debt protection program, Aven offers borrowers unique benefits you can’t find with other lenders.

Cons

- Virtual appraisals aren’t always accurate

- While convenient, automated appraisals aren’t as thorough as in-person valuations. Because it can’t catch everything, Aven’s system might undervalue your home.

- Not available everywhere

- Aven only lends in 32 states, rendering many homeowners ineligible for its HELOC.

- Limited draw period

- Aven’s draw period is considerably shorter than what you might get with another lender, which is only five years.

- Full amount is drawn at origination

- Aven requires borrowers to draw their entire HELOC amount initially, meaning you must repay some of the balance within that five-year draw period to redraw funds as needed.

- No introductory rates or rate discounts

- Some HELOC companies offer perks like a reduced rate for your first 12 months or when you sign up for autopay. Aven, however, isn’t one of them.

Aven credit card review

How does the Aven card work?

The Aven Home Equity Visa Card works like a credit card that is secured by your home equity. It functions similarly to a HELOC because you only borrow what you spend, but it also gives you the everyday convenience of paying with a card. This setup allows Aven to offer lower interest rates than typical credit cards and a faster approval process than most home equity products.

Rates and terms

Aven offers variable rates, with a small discount available for enrolling in autopay. It also provides a fixed-rate option through its Aven Simple Loan, allowing borrowers to convert balances into predictable monthly payments.

Here is a summary of the card’s core terms:

| Term | Details |

| APR | 7.99% and 15.49% (variable) |

| Fixed-rate option | Available through Aven Simple Loan for qualifying borrowers |

| Terms | Account renews annually up to 15 years |

| Credit limit | Up to $400,000 |

| Annual fee | $0 |

| Appraisal | Not required; uses automated valuation models |

| Closing costs | None |

| Funding time | As little as 3 days after approval |

| Right of rescission | Available, similar to other home equity products |

Fees

Aven has fewer upfront costs than traditional HELOCs. There are no appraisal fees, origination fees, or closing costs. However, certain transactions have associated fees.

| Fee type | Cost |

| Origination fee | $0 |

| Cash transfer to bank | 2.5% of amount transferred |

| Balance transfer fee | 2.5% of amount transferred |

| Annual fee | $0 |

| Late payment fee | $29 |

Key features

Aven’s Home Equity Visa Card combines credit card flexibility with home equity-backed rates and a fully digital experience:

- Built-in safeguards: Offers foreclosure protection support and flexible repayment options if you face financial hardship.

- Fast, online process: Prequalify in minutes with a soft credit check, then complete the entire application, verification, and closing online.

- Quick access to funds: Get approved for up to $400,000 and access funds in as little as three business days.

- Flexible borrowing options: Use the card for purchases, transfer funds to your bank, or consolidate balances at your card’s APR (2.5% transfer fee applies).

- Rewards on spending: Earn unlimited 2% cash back on all purchases.

- Competitive rate protections: Includes a lowest rate guarantee for qualifying offers.

How do you repay an Aven credit card?

Repayment works similarly to a traditional credit card, with a minimum payment of about 1% of your balance plus interest and fees. While that keeps payments flexible, paying only the minimum can slow your progress and increase interest costs.

To create more structure, Aven offers the Simple Loan option, which lets you convert eligible balances into fixed monthly payments with a set payoff timeline. Otherwise, balances remain revolving, including cash transfers to your bank.

Overall, the card offers flexible repayment, with the option to switch to a more predictable plan for larger balances.

Aven card requirements

Aven’s fully automated system evaluates your eligibility for the Aven card based on your equity, your income, and your credit score. The company doesn’t disclose many of the specific eligibility details for its credit card, but here’s what we’ve found:

| Requirement | Details |

| Properties | Primary residences, secondary homes, investment properties (additional requirements apply for the latter two) |

| State of residence | Available in 45 states |

| Maximum loan-to-value | 89% of primary residences |

| Maximum debt-to-income | Not disclosed |

| Minimum credit score | 640 for primary residences |

| Minimum income | Not disclosed |

| Age and identification | Must be 18 years of age or older and possess acceptable government-issued identification |

You must also provide proof of insurance for credit lines above $100,000. Aven/Coastal Community Bank must also be added as a beneficiary to that insurance policy.

How does your home’s value affect your terms?

Aven allows a maximum combined loan-to-value (CLTV) ratio of 89% on primary residences for its credit card. This means that your loan amount combined with what you owe on your mortgage can’t exceed 89% of your home’s value.

For example, if you have a home worth $500,000, 89% of that is $445,000. If you have a mortgage for $300,000, that’s a potential $145,000 line of credit.

A higher value on the home could mean a higher loan amount or a lower combined loan-to-value (CLTV) ratio. A lower CLTV ratio could mean a better interest rate. But your income and debt levels also play a role in qualifying you for the card and the terms you get.

Aven credit card pros and cons

Aven’s credit card is unique, so it’s essential to weigh the pros and cons to determine if it’s the right fit for you. Here’s a rundown of its strengths and weaknesses.

Pros

- Easy process

- The technology Aven uses speeds the application process along. You may be able to access a large credit line with favorable interest rates within a week.

- Low interest rates

- The APR on the Aven card can be around half of the APR on other credit cards.

- High credit limit

- In many states, you can get a credit line up to $400,000, which offers substantial borrowing power.

- No appraisal required

- Aven’s automated system means you skip the traditional appraisal, speeding up the application process.

- No origination fees

- Traditional HELOCs often come with origination fees. With Aven, you avoid that upfront cost.

- Up to 2% cash back

- By using your Aven credit card, you earn 2% cashback on your spending.

- You only borrow what you need

- Because the credit line is revolving, you only take on debt when you actually spend. This can be more cost-effective than a lump-sum home equity loan.

Cons

- High qualifications for low rates

- For Aven’s most favorable rates, you’ll need a high credit score and substantial home equity.

- Fees for cash and balance transfers

- Aven charges a 2.5% fee on cash transfers to your bank and on balance transfers. These costs are lower than many traditional credit card fees but higher than what you would pay with a standard HELOC, where drawing funds typically does not cost extra.

- Aven can reduce your credit limit

- If you’re not using your account, Aven reserves the right to reduce the credit line you can access on each account anniversary.

- Daily and monthly withdrawal limits

- Users report daily and monthly limits of $15,000 and $30,000, making it difficult to make larger purchases. CashOuts have a higher daily $50,000 withdrawal limit, but they’re still subject to the 2.5% fee.

- Required initial draw for credit lines over $100,000

- If your credit line is over $100,000, you need to draw at least $50,000 in the first 90 days, or your credit limit will be reduced.

Is Aven a good credit card to use?

Aven can be a good fit for homeowners who want flexible access to funds at lower rates than typical credit cards. It works well for expenses like home improvements or consolidating higher-interest debt without taking out a traditional HELOC.

It’s less ideal if you prefer unsecured credit or tend to overspend with easy access to credit. Because your home is used as collateral, disciplined use matters. The 2.5% fee on cash and balance transfers is also worth considering if you plan to move funds frequently.

Aven HELOC credit card vs. Aven HELOC

The card is designed for fast access and flexible, ongoing use, with revolving repayment similar to a credit card. Aven Home Equity Cash is built for structure, with each draw converted into a fixed-rate plan and predictable monthly payments.

| Feature | Aven card | Aven Home Equity Cash |

| Collateral required | Yes ✅ | Yes ✅ |

| Interest rates | Variable | Fixed, with a new fixed rate assigned at each draw |

| Credit line | Up to $400,000 | Based on home value and income, up to 89% combined loan-to-value |

| Cashback rewards | Up to 2% | Not offered |

| Application | Fully automated and online | Online application with full underwriting review |

| Fees | 2.5% on cash transfers and balance transfers | No appraisal, no origination fee, no closing costs |

| Valuation | Automated valuation model | Automated valuation model |

| Repayment | Revolving, similar to a credit card | Fixed-rate repayment for each draw |

| Minimum credit score | 640 | 640 minimum listed; 720 recommended for best approval odds and rates |

Aven Home Equity Cash is usually the better choice if you want predictable payments and long-term stability. The card makes more sense if you want quick, reusable access to your equity.

Aven home equity card vs. traditional credit card

The Aven card works like a credit card, but the biggest difference is that it’s secured by your home. That allows for higher credit limits and access to cash at your card’s rate, but it also adds risk.

Traditional credit cards are unsecured and easier to qualify for, but they typically come with lower limits and fewer options for accessing large amounts of cash at reasonable rates.

| Feature | Aven card | Credit card |

| Collateral? | Yes ✅ | No ✖️ |

| Interest rates | Variable | Often variable and higher |

| Credit line | Up to $250,000 | Often lower |

| Cashback rewards | Up to 2% | Varies by card |

| Application | Automated, online | Often online |

| Fees | Cash-outs and balance transfers | Varies |

| Appraisal? | Automated | No |

| Repayment | Similar to credit card | Monthly minimum |

| Credit score | 640 | Varies |

If you want a high-limit, flexible line backed by your home, the Aven card can fill that gap. If you’d rather avoid putting your home at risk, a traditional credit card is the safer option.

Aven HELOC alternatives

For many homeowners, Aven’s Home Equity Cash may be the clear winner, and for good reason. Still, it’s wise to consider your options before committing to a lender. Here are three of the best HELOC lenders available:

rates

6.99% – 15.49%

8.35% – 16.55% fixed

12-mo intro starting at 6.99%, then 8.50%+ variableⓘ

loan amounts

$5,000 – $400,000 ($100,000)

$15,000 – $750,000

$10,000 – $1 million

repayment terms

5, 10, 15, or 30 years

5, 10, 15, or 30 years

Draw: 10 years / Repayment: 20 years

- Aven vs. Figure: Figure is available in more states. If you live in a state where Aven is not offered, Figure may be the better fit. Read more about how Aven and Figure compare.

- Aven vs. FourLeaf: FourLeaf offers a 10-year draw period, and HELOC limits up to $1 million. Homeowners who want longer access to their line or significantly higher borrowing power may prefer FourLeaf over Aven.

Is Aven legit? Aven.com and HELOC product reviews

Yes. Aven is a legitimate lender with strong customer feedback, including thousands of positive Trustpilot reviews and an A+ rating from the Better Business Bureau (BBB).

Most reviews focus on its home equity card, but they still reflect overall service quality, communication, and support:

| Source | Customer rating | Number of reviews |

| Trustpilot | 4.9/5 | 8,677 |

| Better Business Bureau | 1.08/5 | 12 |

Aven’s low BBB customer rating is based on a small sample size, while its A+ accreditation reflects strong business practices and responsiveness. In contrast, its high Trustpilot rating is backed by a large volume of reviews, making it a more reliable indicator of customer experience.

Customers often highlight Aven’s fast application process, clear communication, and responsive support. Some negative reviews mention occasional communication issues or account freezes, though these appear to be limited.

Overall, Aven’s strong review profile is why we consider its HELOC the best for customer reviews.

How to contact Aven

You may want to download Aven’s app to help manage your Aven card. This app allows you to check your balance, see your transactions, and pay your bills. You can also manage your Aven card online.

If you need to contact customer service, you have several options to get in touch:

- Email: [email protected]

- Website: Send a message via the contact form.

- Schedule a call back: Set up a time that’s convenient for you

- Call: 415-582-6613

How to apply with Aven

Apply for a Home Equity Cash HELOC

Aven’s tech-powered HELOC application process is just as innovative as its product offerings. Here’s how it works:

- Enter your phone number to start the application. Alternatively, you can enter your Aven invite code if you have one.

- Tell Aven how much you need to borrow. You’ll also tell Aven how you plan to use your credit line.

- Provide your contact details and identifying information. This includes your date of birth and the last four digits of your Social Security number. If you’re applying with another person, you’ll also enter their information.

- View your prequalified offers. At this stage, you haven’t consented to a hard credit pull. You’re simply getting Aven’s preliminary approval and choosing the potential HELOC terms that work best for you.

- Verify your income. Aven automatically verifies the majority of its customers’ income when you apply. Some customers may be asked to either link your bank account with Plaid or send in documents like W-2s or 1099s for manual review.

- Submit your application. Now, you’ll give Aven permission to run your credit and present you with a final HELOC offer.

- Schedule your notary session. If approved, Aven will connect you with an online notary to review and sign your documents.

After reading your HELOC agreement, prepare to hang tight through the mandatory three-day waiting period. As soon as this window passes, Aven will fund your HELOC, and you’ll have access to your new credit line.

Apply for the home equity-backed credit card

Applying for an Aven card is much faster and easier than applying for a HELOC. The card also allows you to prequalify, which allows you to check your offer without affecting your credit score.

If you do proceed, you will be subject to a hard credit check later in the process. You will also need to provide proof of income and sign in front of an online notary.

Here’s what the application looks like from start to finish.

- Check your offer. Go to Aven’s homepage and click “Check your offer.” You’ll enter your mobile phone number to get started.

- Enter the max amount and purpose. You’ll give the lender your top value and specify a purpose (debt consolidation, home improvement, etc).

- Confirm identity. You’ll fill in your name, email, address, last four digits of your social security number, date of birth, property address, and joint applicant information.

- Review your offer. Check whether you qualify, and review the terms. You’ll see a credit limit, APR, and cashback percentage. Proceed to the next step if you can accept the terms.

- Income verification. You can verify your income by connecting a bank account or by uploading tax return documents, pay stubs, W-2s, retirement and benefit income.

- Credit check. Aven will do a hard credit check at this stage.

- Digital signing. An online notary will help you sign the required documents via video call.

How we rated Aven in our home equity reviews

We designed LendEDU’s editorial rating system to help readers find companies that offer the best HELOCs. Our system awards higher ratings to companies with affordable solutions, positive customer reviews, and online transparency of benefits and terms.

We compared Aven to several home equity lenders, using hundreds of data points from company websites, public disclosures, customer reviews, and direct communication with company representatives. We weighted, scored, and combined each factor to produce a final editorial rating. This rating is expressed on a scale from 1 to 5, with 5 being the highest possible score. Our take is represented in our rating, recapped below.

Related articles

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.