One of the largest purchases people commonly make is a vehicle. While it’s great to buy a car with cash if you have the funds, this isn’t always possible. An auto loan can be a way to fund the purchase, but you’ll be paying it back for years, so it’s essential to understand how it works.

In this article, we’ll share important terms to know when evaluating an auto loan and walk you through how your payments are calculated and change over time. You’ll also learn how to get a loan, how to repay it, and what can happen if you have trouble paying it back.

How auto loans work: Terms to know

To understand how auto loans work, start by familiarizing yourself with several terms used in conversations about auto loans. Some of the most common loan terms you need to know are:

- Loan amount: This is the money you borrowed to purchase the car. You’ll pay back the entire loan amount (the original principal balance) over the loan’s term (the amount of time you have to pay back the loan).

- Principal: Your original loan amount is also your original principal balance. Each month you make a payment, you’ll repay some of the principal. At the end of the month, your outstanding principal balance is the amount you owe after deducting all the principal payments you’ve made.

- Down payment: This is the amount of money (if any) you must put toward purchasing your car. Depending on your credit and your auto lender’s requirements, you might not need to make a down payment on a vehicle purchase.

- Interest rate: The interest rate is used to calculate how much interest you owe at each payment period. Two methods exist to calculate the interest you owe: the simple interest method and the precomputed interest method. The simple method is the most common, so we’ll use it here.

- Term: This is how long you have to fully repay your loan, expressed in years or months. When you get an auto loan, the repayment term matches the loan’s amortization. The phrase “amortization” refers to the period used to calculate how much principal and interest you owe each month.

- Monthly payment: This consists of principal and interest. The principal portion is based on an amortization schedule that calculates how much you must pay each month to fully repay the loan during its term. The interest portion is calculated using the monthly outstanding principal balance.

- Fees: This represents money you must pay your lender upfront to get the loan. Some types of fees you might be charged are loan origination, application, processing, and title fees. These fees cover some of the lender’s costs of making the loan. Notably, not all lenders charge fees.

- APR (annual percentage rate): The term APR refers to the interest rate you’ll pay on your loan each year, including fees or additional costs. Since this figure includes the fees you’re charged, it’s higher than your interest rate, making it a better basis for comparison when shopping for a loan.

- Cosigner: This is someone besides the primary borrower who takes responsibility for repaying the loan. Cosigners are often used when the primary borrower can’t qualify for a loan independently. In this case, lenders use the cosigner’s and borrower’s credit and income to approve the loan.

- Total cost: This is how much you’ll pay for the auto loan, including the original loan amount, the total interest paid over the loan’s term, and any fees or other costs you paid your lender to get the loan.

How your auto loan payments are calculated

Your auto loan payments are calculated using your original loan amount, loan term, outstanding principal balance, and the interest rate you’ve agreed to pay. These items are used together to calculate the monthly payment on your auto loan.

There are two ways interest can be calculated into your payment.

- Simple interest method: Most commonly used by lenders, the simple interest method uses your outstanding principal balance to calculate the interest owed monthly. If you prepay some of the principal, you’ll owe less interest than initially planned because you’ll have a lower principal balance.

- Precomputed interest method: Using this method, the amount of interest you’ll pay is calculated upfront. Even if you make extra payments and reduce your outstanding balance faster than expected, you cannot benefit from interest savings like you can with the simple method. This is a crucial drawback.

While the precomputed interest method is uncommon, it’s something to watch out for when shopping for a loan. You may find it offered by lenders who give loans to people with bad credit or dealers who offer buy-here-pay-here auto loans.

We’ll use the simple interest method in an example. Let’s say you get an auto loan with the following characteristics:

- Loan origination date: April 1, 2023

- Loan amount: $30,000

- Fees: $0

- Term: 60 months (five years)

- Interest rate: 6.00% (fixed)

- Monthly payment: $579.98

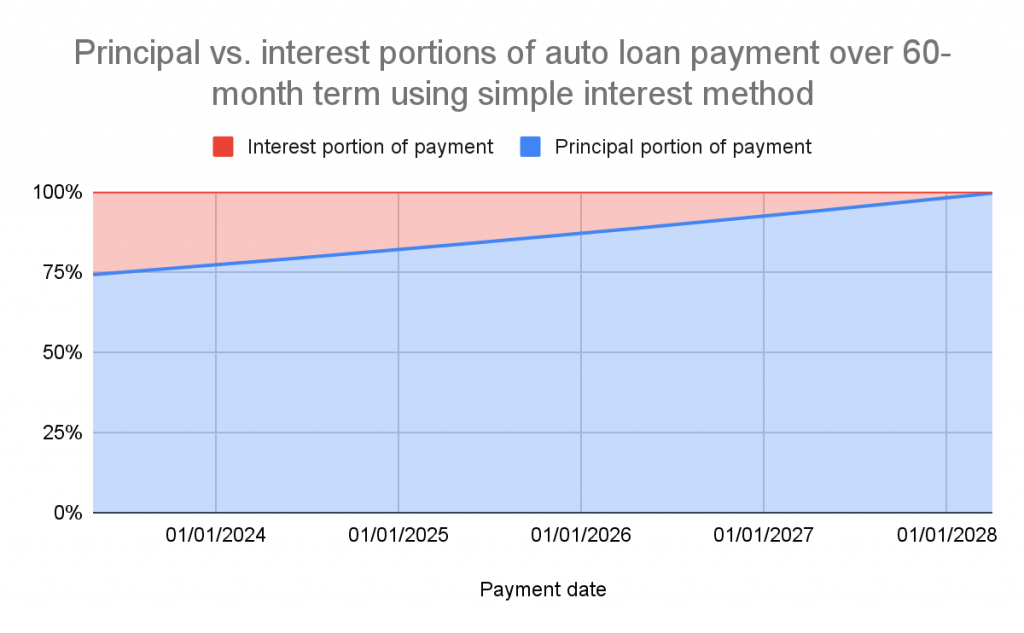

The original loan amount, term, and interest rate are all used to calculate the size of the monthly payment you’ll need to make each month until your loan is fully repaid at the end of its term. The breakdown of your monthly payment on May 1 of each year and your last loan payment is shown below:

| Payment | Date | Balance | Payment | Principal | Interest | Remaining |

| 1 | 05/01/2023 | $30,000.00 | $579.98 | $429.98 | $150.00 | $29,570.02 |

| 13 | 05/01/2024 | $24,695.90 | $579.98 | $456.50 | $123.48 | $24,239.40 |

| 25 | 05/01/2025 | $19,064.66 | $579.98 | $484.66 | $95.32 | $18,580.00 |

| 37 | 05/01/2026 | $13,086.10 | $579.98 | $514.55 | $65.43 | $12,571.55 |

| 49 | 05/01/2027 | $6,738.80 | $579.98 | $546.29 | $33.69 | $6,192.51 |

| 60 | 04/01/2028 | $577.10 | $579.98 | $577.10 | $2.89 | $0.00 |

Your monthly payment always stays the same. However, as you slowly repay the principal, the portion of your payment allocated to the principal increases, and the portion allocated to the interest decreases. This happens because your monthly interest is based on your outstanding principal balance.

Now that you know how auto loan payments are calculated, the following example shows how your monthly payment would change under two other scenarios using two additional repayment terms. It also shows the total cost of your loan under all three scenarios (assuming you didn’t pay any fees).

| Scenario 1 | Scenario 2 | Scenario 3 | |

| Loan amount | $30,000 | $30,000 | $30,000 |

| Rate (APR) | 6.00% | 6.00% | 6.00% |

| Term length | 60 months | 36 months | 84 months |

| Monthly payment | $579.98 | $912.66 | $438.26 |

| Total cost | $34,799.04 | $32,855.69 | $36,813.56 |

As you can see above, even though you’ll have the largest monthly payment with the second scenario, the total cost of your loan is the lowest. Since you’re making larger payments, more of your money is going to interest each month. As a result, you pay less interest over the loan’s life.

For this reason, as you’re considering the loan terms that are right for you, don’t focus solely on the monthly payment. While you may pay less each month with a longer repayment term, your overall borrowing costs will be greater. To reduce your total cost, choose the shortest term you can afford.

How do you qualify for an auto loan?

To qualify for an auto loan, you’ll generally need to show the ability and willingness to repay the loan. Your lender will determine if you meet these creditworthiness criteria by doing such things as reviewing your credit, considering your job history, and evaluating your income.

You’ll get the best rates and terms with good-to-excellent credit. However, some lenders approve people with low credit scores for an auto loan. Regardless of your credit, you can often show that you can afford the payments with a debt-to-income ratio of no more than 45% to 50%.

| 2 critical factors in auto loan qualification |

| Credit score > 670 for best rates |

| Debt-to-income ratio < 45 – 50% |

If you can’t qualify for the loan on your own or want better rates (e.g., you have bad credit or you’re a college student without a steady income), you may be able to use a cosigner. Your lender will also use your cosigner’s income and credit to determine if you qualify and the rates you can get.

Remember that if you use a cosigner, your cosigner is legally responsible for paying for your loan if you fail to do so. If you don’t repay the loan as agreed, you’ll hurt your cosigner’s credit and your own. So, to preserve your relationship, make sure you’re correctly managing the loan.

How do you apply for an auto loan?

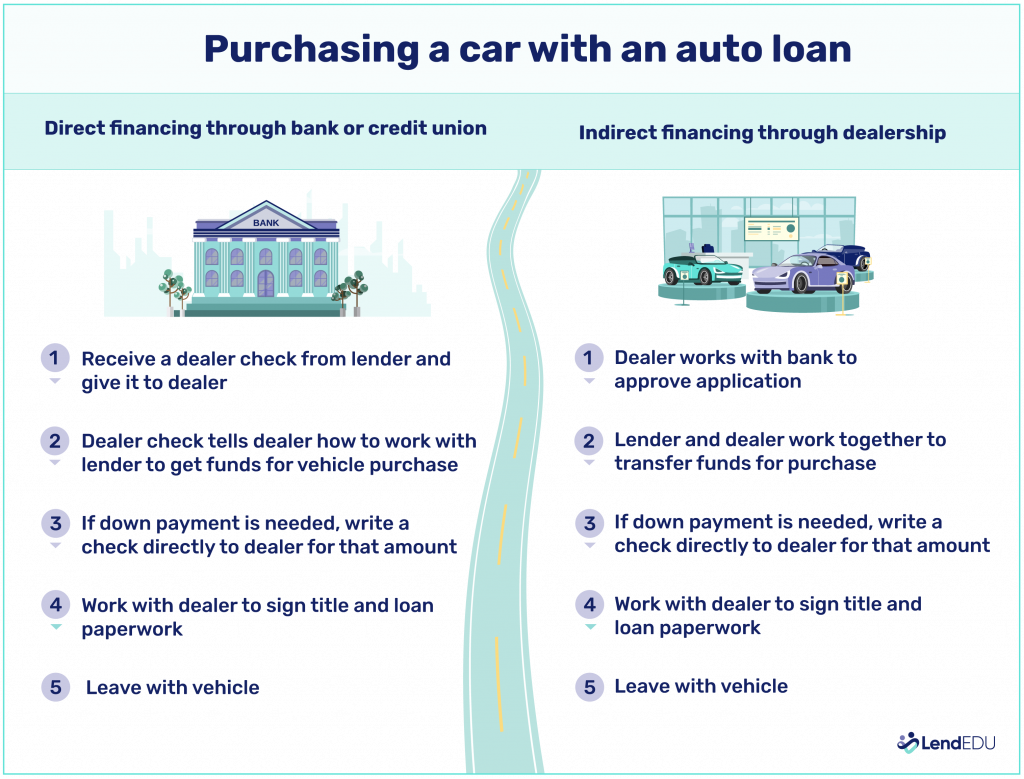

Once you’re ready to get an auto loan, the next step is to apply by submitting an application with personal information and details about your income (such as monthly income and job history). There are two ways to do this:

- Direct financing: When you apply directly at a bank or credit union

- Indirect financing: When you apply at a car dealer

Car dealers are often authorized to accept loan applications for specific lenders, approve the applications automatically if the borrower meets set criteria, and escalate it to the lender for manual approval if not. The dealer itself may also offer financing.

While some dealerships consider your best interests when offering indirect auto loans, some are more focused on selling a car than doing what’s right for you. Lenders allowing indirect loans often require the dealerships to meet lending quality requirements to participate in the loan programs.

Dealers who don’t meet the requirements may eventually be eliminated from the indirect loan program. If you’re considering indirect financing, read reviews about the dealership and its services before proceeding. If it uses high-pressure lending tactics, it may be best to simply walk away.

How do you purchase a car with an auto loan?

Ultimately, you’ll use some or all of the proceeds from your auto loan to pay for the car. If you’re approved for 100% financing, the auto loan will be used to pay for everything. If you must make a down payment, you’ll also contribute cash to the vehicle purchase.

If you apply directly with a bank or credit union, you’ll usually receive a “dealer check” to give to the dealership. This “check” is paperwork telling the dealer how to get paid (e.g., provide a copy of the title and payment instructions). The lender and dealer will work out the details for you.

When you get a loan from a dealer, its finance department will do everything, including processing the application and sending the proceeds to your lender. With direct and indirect financing, you’ll also meet with the dealer’s finance group to finalize the purchase details (e.g., titling the car).

It’s a little trickier if you buy a car from a private party, as you’ll have to do some of the work normally done by the car dealership. Examples include giving your lender a copy of the vehicle’s title and coordinating payment with the seller and lender.

How do you repay an auto loan?

Once you’ve received an auto loan, the next step is to pay for it. After completing the car purchase, you’ll sign loan documents and be given instructions about when your payments will be due and how to make them. You pay your lender online or even send them a check.

Sometimes, you’ll even receive a discount on your interest rate if you set up autopay when you apply for the loan (e.g., a 0.25% reduction in your rate). If you do this, you’ll give your lender payment instructions when you apply, and your payments will be automatically paid on the due date.

However you pay, make your payments on time. If you pay late, you may be charged a fee (e.g., $25 to $50), which can hurt your credit. If you have trouble paying or experience financial hardship, proactively contact your lender. It may be able to help by, for example, temporarily pausing your payments.

If you miss payments, your lender may decide to pursue remedies like repossessing your car and selling it at auction. Depending on your state, if the auction sales price isn’t enough to cover your car loan and any fees, you might be responsible for the deficiency balance. Pay on time to avoid this.

About our contributors

-

Written by Megan Hanna, CFE, MBA, DBA

Written by Megan Hanna, CFE, MBA, DBADr. Megan Hanna is a finance writer with more than 20 years of experience in finance, accounting, and banking. She spent 13 years in commercial banking in roles of increasing responsibility related to lending. She also teaches college classes about finance and accounting.

-

Edited by Jeff Gitlen, CEPF®

Edited by Jeff Gitlen, CEPF®Jeff Gitlen, CEPF®, is the director of growth at LendEDU. He graduated from the Alfred Lerner College of Business and Economics at the University of Delaware.