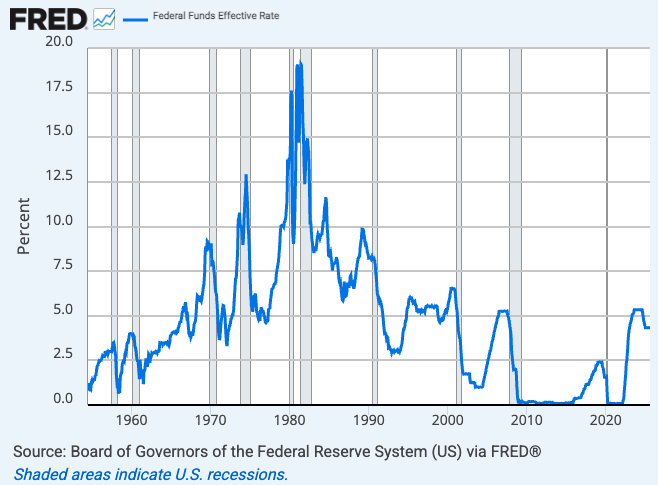

The Federal Reserve just cut interest rates by 0.25 percentage points for the first time since 2024. The new federal funds rate now sits at 4.00% to 4.25%.

That’s a small change on paper, but it matters for your money. Rate cuts can ripple across the economy and affect what you pay on loans and (just as importantly) what you earn on your savings.

So what does this mean for the cash sitting in your savings account or certificate of deposit (CD)? We’re glad you asked.

Table of Contents

High-yield savings rates: Still good, but slipping

If you’ve opened a high-yield savings account in the past year, you’ve likely gotten used to seeing 3.50% to 4.50% APYs. That’s been a welcome change after 2020 and 2021, when savings accounts earned between 0.05% and 0.10%.

But those high yields were never permanent. They rose because the Fed raised rates aggressively to fight inflation. Now that the Fed is starting to cut rates again, with the most recent 0.25% drop, banks have less incentive to pay savers top dollar.

We’re already seeing that shift. Just a few months ago, online banks like SoFi and Betterment were offering APYs of 4.50% or higher. As of this week, many of the best rates are between 3.50% and 4.00%.

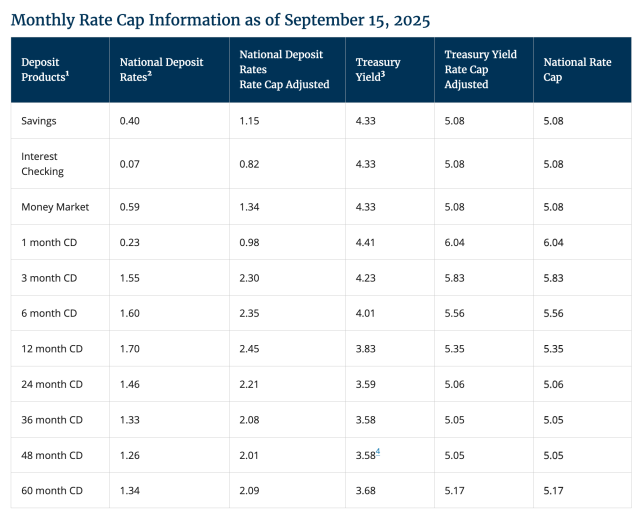

That’s still miles better than a traditional savings account, where the national average is just 0.40%, according to Federal Deposit Insurance Corporation (FDIC) data. But it’s a clear sign that the party could be winding down.

So what does that mean if you have cash parked in savings?

- If you’re at a big bank: You likely won’t notice much change. Your APY was already tiny, and it will stay tiny.

- If you’re at an online bank: Expect slow, steady declines. Your 3.50% account might slip to 3.25% in the coming weeks, and possibly under 3% if more Fed cuts follow.

- If you’re considering moving banks: Now’s the time to compare. Rates are still competitive at around 3.50% or higher, but that won’t last forever. (Check out offers from our partner MyBankTracker for high-yield savings accounts with rates many multiples higher than the national average.)

While the impact on financial products isn’t always immediate, we’ve already seen some APYs decline since the Fed’s decision.

| Company | Old APY | New APY | Change |

|---|---|---|---|

| Betterment | 4.00% | 3.75% | -0.25% |

| Robinhood | 4.00% | 3.75% | -0.25% |

CDs: Lock in while you can

Certificates of deposit (CDs) are the flip side of savings accounts. Instead of a variable rate that can move up or down with the Fed, CDs let you lock in a fixed rate for a set term, usually anywhere from six months to five years. That fixed-rate feature suddenly looks much more attractive when you know rates are heading south.

If you locked in a CD earlier this year, congratulations: You get to ride out your full term at that higher yield, no matter how many times the Fed cuts. But if you’ve been on the fence about opening one, now’s the moment to act (if a CD still makes sense for your financial situation).

Why? Because once the Fed cuts rates, banks follow. A 0.25% cut may not sound like much, but multiply that by a few rounds of cuts, and suddenly today’s 4%-or-higher CD looks pretty sweet compared to what might be available in six months.

Here are a couple of smart CD strategies to think about:

- Laddering: Instead of putting all your money in a single two-year CD, you could spread it across a six-month, one-year, and two-year CD. That way, you’ll have cash coming due at different times, and you can reinvest if rates bounce back.

- Locking in longer terms: If you have a lump of cash you know you won’t need for a while, consider snagging a two- or three-year CD at today’s rates. It’s a simple way to guarantee a solid return if the Fed keeps trimming.

APYs have declined on CDs since the cut.

| Company | Old APY | New APY | Change |

|---|---|---|---|

| Marcus 6-Month | 4.40% | 4.25% | -0.15% |

| Marcus 9-Month | 4.30% | 4.15% | -0.15% |

| Marcus 12-Month | 4.20% | 4.10% | -0.10% |

What about loans and mortgages?

Even though savings APYs are the headline here, borrowing costs are also shifting.

- Prime rate: Big banks cut their prime lending rate from 7.50% to 7.25% after the Fed’s move. That affects credit cards, personal loans, student loans, and HELOCs with variable rates.

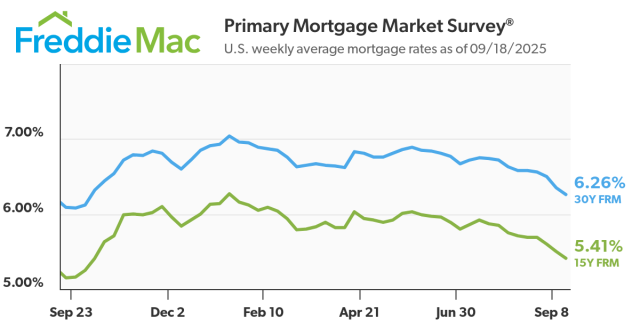

- Mortgages: The average 30-year fixed mortgage rate is now around 6.26%, the lowest in about a year. That’s good news for anyone looking to refinance or buy.

What savers should do right now

Rate cuts can feel like a gut punch if you’ve been enjoying 4% or 5% on your savings. But don’t panic. These cuts are normal, so focus on these tips instead:

- Stick with a bank you like. No single bank always has the “best” rate. Some weeks, one bank will top the list, and the next week it’ll be another. Instead of constantly hopping around, choose a bank that offers a good APY, solid customer service, and the account features you need. If you’re earning more than 3.00% right now, you’re in a great spot.

- Remember the baseline. Even if high-yield savings accounts drop to 2%, they’ll still pay far more than a traditional savings account at a big bank. At 0.40% on average, those old-school accounts don’t even come close. A HYSA almost always keeps you ahead of the rest.

- Use CDs wisely. Opening a CD can be a smart choice if you know you won’t need that money for the entire term you select. But don’t open one solely because you’re afraid of rates dropping (and never use them for emergency funds). Early withdrawal penalties can sting, and tying up cash you might need can backfire. CDs are for extra savings you’re confident you can set aside.

- Balance the good and the bad. Yes, lower Fed rates mean your savings APY will drift down. But there’s a silver lining: Borrowing costs are drifting down too. If you have a credit card balance, a HELOC, or a variable-rate student loan, your rate could drop in the months ahead.

The 0.25% reality check

This quarter-point cut won’t change your financial life overnight. But it signals the start of a new trend: Savings yields are likely heading lower.

If you’ve been enjoying 3%+ APYs on your high-yield savings account, don’t take it for granted. Rates are already slipping, and more cuts could follow.

The bottom line is to lock in what you can, keep your expectations realistic, and remember that even at 2% or 3%, you’re earning far more than you would in a traditional savings account.

Article sources

At LendEDU, our writers and editors rely on primary sources, such as government data and websites, industry reports and whitepapers, and interviews with experts and company representatives. We also reference reputable company websites and research from established publishers. This approach allows us to produce content that is accurate, unbiased, and supported by reliable evidence. Read more about our editorial standards.

- Federal Reserve, Federal Reserve issues FOMC statement

- Federal Reserve Bank of St. Louis, Federal Funds Effective Rate

- Federal Deposit Insurance Corporation, National Rates and Rate Caps – September 2025

- Reuters, Big U.S. Banks Lower Prime Lending Rates After Fed Rate Cut

- Freddie Mac, Primary Mortgage Market Survey

Recommended readings

- Jobs Data Could Spell Rate Cuts Ahead

- Safest Banks in the United States in 2025: Where to Keep Your Money Secure

About our contributors

-

Written by Cassidy Horton, MBA

Written by Cassidy Horton, MBACassidy Horton is a finance writer passionate about helping people find financial freedom. With an MBA and a bachelor's in public relations, her work has been published more than 1,000 times online.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.