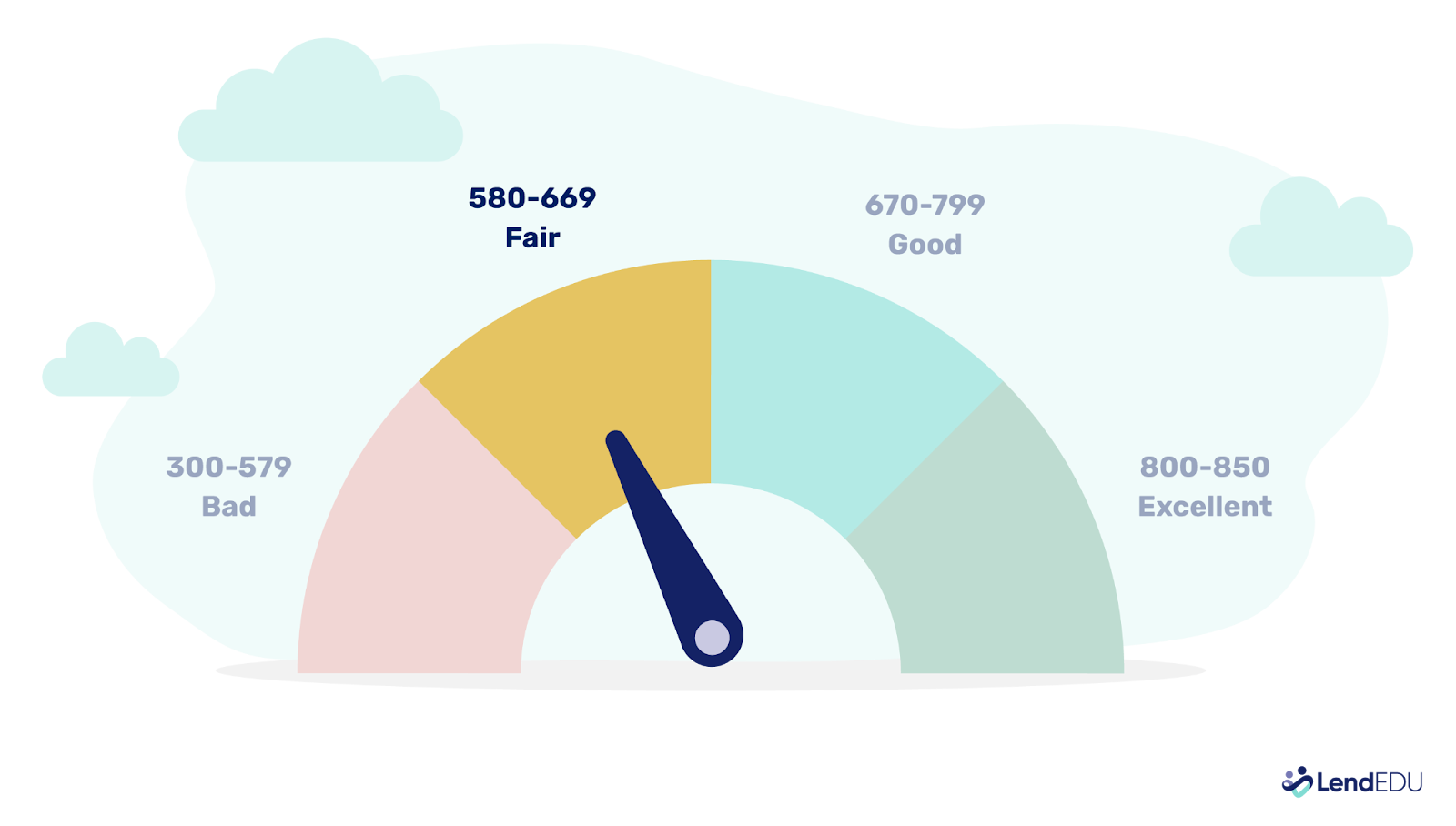

While many HELOC lenders list minimum credit score requirements of around 640 to 680, approvals for fair credit borrowers are rare. Most lenders prefer applicants with scores of 720 or higher. If you have fair credit (580 to 669), getting approved can be difficult, so you may want to consider alternatives like home equity agreements, which often accept lower credit scores.

If you are approved for a HELOC, expect higher interest rates than borrowers with stronger credit, which can increase your overall borrowing costs. Shopping around is key, as lenders weigh credit factors differently and some may offer more flexible terms. Comparing options can help you secure better rates and improve your chances of approval.

Note: If your credit score is below 720, it is unlikely that you will pass the prequalification stage for many HELOC lenders. If your score is higher than 580, the options in this article may work. Below 580, look into home equity agreements as an alternative.

Table of Contents

The best HELOCs for fair credit

We recommend these home equity lines of credit if you have fair credit because they have lower starting interest rates and more lenient credit requirements than other HELOC lenders.

New American Funding

Why it’s one of the best

New American Funding stands out for its speed—borrowers can get approved in as little as five minutes and receive funds in as few as five days when using online notarization. That makes it one of the faster options available for tapping home equity.

It’s accessible with a minimum 620 credit score, but rates and fees may be higher for lower-credit borrowers. There’s a 4.99% origination fee, and you’re required to draw 100% of the funds at closing. After that, you can redraw from your full credit limit during the draw period.

New American Funding doesn’t post rate ranges online, so it’s hard to compare exact costs upfront. It also offers multiple products and can help determine whether a HELOC or cash-out refinance is a better option.

- Approval in five minutes, funding in as little as five days

- Redraw 100% of your credit line over time

- 4.99% origination fee and full draw required at closing

- Not available in New York, Texas, West Virginia

HELOC terms

| Rates (APR) | Fixed at origination and at each draw based on Prime Rate; exact rates undisclosed |

| Funding amount | Up to $400,000 |

| Repayment terms | 2 – 5 year draw; repayment varies based on draw period |

| Availability | Not available in New York, Texas, West Virginia |

Upstart

Why it’s one of the best

Upstart partners with lenders to offer HELOCs in select states, with some partner lenders open to borrowers who have so little U.S. credit history that they don’t have a credit score.

The platform’s flexibility makes it a potential lifeline for those who are typically overlooked by conventional lenders. Eligibility and underwriting guidelines vary by partner, but some may overlook issues like bankruptcies or certain public records.

Appraisals are generally not required, and the process can move fast—some borrowers see closing in as few as two days and funding in as fast as eight days.ⓘ However, origination fees of up to 4.99% apply, and availability is limited to 41 states and Washington, D.C.

- Works with limited/no credit history

- No appraisal, fast approval and funding

- Origination fee up to 4.99%

- Not available in all states

HELOC terms

| Rates (APR) | 3.99% – 18%ⓘ |

| Loan amounts | $26,000 – $250,000 |

| Repayment terms | 3-year draw; 10 or 15-year repayment |

| Availability | Not available in Georgia, Hawaii, Massachusetts, Missouri, Nevada, New York, Rhode Island, Vermont, and Texas. |

LendingTree

Why it’s one of the best

LendingTree’s HELOC marketplace is an excellent option for fair credit borrowers who want to compare multiple lenders without the hassle of multiple applications. Its quick, no-cost prequalification process uses a soft credit inquiry, letting you explore rates and terms without impacting your credit score.

This feature is particularly valuable for fair-credit borrowers, as it allows you to identify lenders willing to work with your credit profile before committing to a full application.

LendingTree’s platform also provides access to both HELOCs and home equity loans, giving you a broader range of options. While its network is limited to participating lenders, its emphasis on transparency and ease of comparison can simplify the search for affordable HELOC terms.

- Quick prequalification with no impact on your credit score

- Access to multiple HELOC and home equity loan offers

- No fees to use the platform

- Available in all 50 states + DC

- Limited to lenders in LendingTree’s network

- Does not disclose the full interest rate range of partner lenders

HELOC terms

| Rates (APR) | Starting at 6.99% |

| Funding amount | $10,000 – $2 million |

| Repayment terms | 5 – 30 years |

| Availability | 50 states + DC |

Stay away from hard credit inquiries—they should only be necessary when you apply for a HELOC. Hard credit checks can lower your score fast.

Eric Kirste, CFP®

HELOC credit scores: Approval odds by score

If your credit score falls in the fair range (580–669), you may see lenders advertise minimums around 640 or even 620. But in practice, it’s rare to get approved for a HELOC with anything below good credit (typically 700–719)—and most approvals go to borrowers with scores of 720 or higher.

Lenders may technically accept applications with lower scores, but strong equity, high income, and low debt are usually required—and even then, approval is far from guaranteed. Here’s how approval odds really play out within the fair credit score range:

| Credit score | Realistic approval odds | What to expect |

| 580 | Nearly impossible | Well below even flexible lender minimums. You’ll likely need to explore alternatives like personal loans or sale-leaseback programs. |

| 600 | Extremely unlikely | Still far below typical thresholds. HELOCs are out of reach for most, even with strong equity. |

| 620 | Very unlikely | May meet some lenders’ stated minimums, but actual approvals are rare without exceptional compensating factors. |

| 640 | Unlikely | This is where minimum requirements start—but in reality, most lenders still deny fair-credit borrowers. |

| 660 | Possible, but not common | A borderline score. You’ll need strong income, low debt, and significant equity to stand a chance. |

| 669 | Better odds, but still limited | At the top of the fair range, you might get offers from more flexible or fintech lenders—but approvals remain limited. |

What to do if you need a HELOC with a 600s credit score

If your credit score is in the fair-credit range—under 700—here are your best options:

- Look into alternatives like home equity loans, personal loans, or cash-out refinances

- Improve your score by reducing credit card debt and avoiding new inquiries

- Consider co-borrowing with someone who has stronger credit

- Explore non-traditional options like shared-equity agreements if you have substantial home equity

💡 Tip: Even if you see a lender advertise a 620 or 640 minimum, don’t assume approval is likely. Check for average funded borrower profiles—or apply with prequalification tools that use soft credit checks to gauge real odds.

What else affects HELOC approval beyond credit score?

Your credit score plays a key role in qualifying for a HELOC, but it’s not the only factor lenders consider. If your score falls in the “fair” range, you may still qualify by strengthening other parts of your application. Showing strong equity, a low debt-to-income ratio, and steady income can help offset a lower credit score and improve your approval odds.

| Criteria | Typical requirement |

| Equity | 15% – 20% equity remaining after HELOC |

| DTI ratio | Less than 43% |

| Income | Stable and sufficient |

Equity

One of the biggest eligibility requirements for a HELOC is how much equity you have built up in your home. Equity is calculated by taking the current market value of your home and subtracting how much you still owe on the mortgage.

Lenders typically want you to have at least 15% to 20% equity remaining after the HELOC is added, based on your home’s appraised value.

For example, if you have a home valued at $400,000 and your mortgage balance is $250,000, your equity is $150,000 or 37.5%. In this case, many lenders would consider offering a HELOC—even with fair credit—because of the strong equity position.

Debt-to-income ratio

HELOC lenders also look closely at your debt-to-income ratio (DTI), which measures how much of your monthly gross income goes toward minimum debt payments like credit cards, loans, and mortgages.

Generally, lenders want your DTI to be 43% or less, including the new HELOC payment. Keeping your DTI low signals to lenders that you can manage additional debt, which can work in your favor if your credit score is borderline.

Income stability

Your income and job history matter as well. Lenders want to see steady employment and enough income to comfortably cover the new HELOC payment on top of your existing debts. Providing recent W2s, pay stubs, or tax returns can help verify your income stability—especially important if your credit score isn’t ideal.

How to choose the best HELOC for low credit scores

As you shop for a HELOC with fair credit, the goal is to find the most affordable loan for your situation. Here are some tips:

Shop around

Get pre-qualified with online HELOC lenders, banks, and credit unions. Look at the interest rates and annual percentage rates (APRs) offered for your credit profile. Rates can vary quite a bit from one lender to the next, so this step pays off.

Understand all the fees involved

HELOCs may come with an application fee, annual fee, inactivity fee, early closure fee, and other charges that can add up quickly. Look for a HELOC with minimal fees.

Check if there is an initial draw requirement

If the lender says you must withdraw a certain minimum the first time you use your HELOC, ensure this minimum is in line with how much you need to borrow. If not, you’ll be forced to take out a large lump sum upfront that you may not need immediately.

Look at the HELOC’s maximum loan-to-value (LTV) ratio allowed for your credit tier

Many lenders have maximum LTVs of 85%, but the cap may be even lower if you have fair credit.

Read all the fine print and policies carefully

For example, some HELOCs only allow interest-only payments for a set period. Consider getting a HELOC from the same lender that services your primary mortgage if they offer a better rate or are more flexible.

Will I pay more for a HELOC with fair credit?

Your credit score has a significant impact on the overall interest you’ll pay on a HELOC. Those with fair credit in the 580 to 669 range typically pay higher interest rates than borrowers with good or excellent credit scores above 670.

For example, let’s say you want to take out a $50,000 HELOC with a 10-year repayment period. A slightly lower interest rate for a better credit score could equate to $10,000 saved in interest paid, as shown in the table below.

| 660 credit score | 720 credit score | |

| Rate | 10% | 8% |

| Total interest paid | $30,000 | $20,000 |

The better your credit score, the lower the interest rate lenders will offer. This can translate into huge savings over the life of the loan, especially for larger loan amounts or longer repayment periods.

If your credit score is borderline between fair and good ranges, it can be worth it to improve your score before applying for a HELOC.

Paying down revolving debt, removing errors from credit reports, and avoiding new credit applications can help. Even a 20 to 30-point boost could qualify you for a better rate.

But if you need HELOC funds relatively soon, apply with your current fair credit score. You can potentially refinance later at a lower rate if your credit improves.

A quick way to raise your credit score is by increasing your credit limit or paying down debt. Try not to use more than 30% of your overall credit limit.

How to apply for a HELOC with fair credit

You’ll follow these steps to apply for a HELOC when you have fair credit:

The full application to approval process can take two to six weeks if everything goes smoothly. Underwriting and appraisal times can vary based on how busy the lender is.

Having your paperwork ready upfront will help expedite the process. The lender will also let you know if it needs any additional paperwork.

Review your credit report for any inaccuracies or incorrect information. Fixing information may lead to increased credit scores.

FAQ

Are there fair-credit home equity loans available?

Yes, fair-credit home equity loans are available, but just like HELOCs, they can be harder to qualify for. Most lenders prefer borrowers with higher credit scores, so if you have fair credit, you may face higher interest rates, lower loan amounts, or stricter requirements. That said, some lenders are more flexible—especially if you have strong home equity, steady income, or a low debt-to-income ratio.

What is the minimum credit score I should aim for before applying for a HELOC loan?

Most HELOC lenders list minimum credit score requirements between 620 and 680, but aiming for at least 680—and ideally 700 or higher—will give you a much better chance of approval. Higher scores can also help you qualify for lower interest rates and better terms, while lower scores often lead to higher costs or more limited options.

How much equity do I need in my home to qualify for a HELOC if I have fair credit?

If you have fair credit, you’ll likely need more equity in your home to qualify for a HELOC. While many lenders require at least 15% equity, borrowers with lower credit scores may be asked to have 20% or more to offset the added risk.

The exact requirement can vary depending on your income, debt-to-income ratio, and other financial factors, but strong equity can significantly improve your chances of approval.

Can I still get a HELOC with a high debt-to-income ratio?

While a high debt-to-income ratio can make it harder to qualify for a HELOC, it’s not impossible. Some lenders have more flexible criteria and are willing to consider applicants with higher ratios, especially if they have strong credit and substantial home equity.

However, a high ratio may result in higher interest rates or lower loan limits.

What are the typical fees associated with applying for a HELOC, and can they be higher if my credit score is low?

When applying for a HELOC, you may face fees such as an application fee, appraisal fee, title search fee, and closing costs. While these charges vary by lender, having a lower credit score could result in higher fees or additional costs, like a risk-based pricing adjustment or higher interest rate.

Some lenders may also require mortgage insurance or impose stricter terms. Be sure to compare offers carefully and ask whether your credit score affects the fee structure.

How does a HELOC affect my credit score?

A HELOC can affect your credit score in several ways. Initially, applying for a HELOC may cause a slight dip in your score due to the lender’s hard inquiry. Over time, responsible use and on-time payments can build your credit history and improve your score.

Can I refinance my HELOC into a fixed-rate loan if I have a low credit score?

Yes, but it may be more difficult. Refinancing a HELOC into a fixed-rate loan is possible with a low credit score, but your options may be limited, and you could face higher interest rates. Some lenders specialize in working with borrowers who have less-than-perfect credit, so it’s worth shopping around. Keep in mind that you may also need enough equity in your home and be prepared for potential closing costs.

How we selected the best HELOCs for fair credit

Since 2018, LendEDU has evaluated home equity companies to help readers find the best home equity loans and HELOCs. Our latest analysis reviewed 850 data points from 34 lenders and financial institutions, with 25 data points collected from each. This information is gathered from company websites, online applications, public disclosures, customer reviews, and direct communication with company representatives.

These star ratings help us determine which companies are best for different situations. We don’t believe two companies can be the best for the same purpose, so we only show each best-for designation once.

About our contributors

-

Written by Cassidy Horton, MBA

Written by Cassidy Horton, MBACassidy Horton is a finance writer passionate about helping people find financial freedom. With an MBA and a bachelor's in public relations, her work has been published more than 1,000 times online.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Eric Kirste, CFP®

Reviewed by Eric Kirste, CFP®Eric Kirste, CFP®, CIMA®, AIF®, is a founding principal wealth manager for Savvy Wealth. Eric brings more than two decades of wealth management experience working with clients, families, and their businesses, and serving in different leadership capacities.