Auto Loan Refinance

- Funds can be available as soon as today

- Lines of credit up to $250K for multiple vehicles

- Tools to track the valuation of your vehicles

- Check your rates without affecting your credit score

- Charges a fee of 1% for each vehicle, plus a $250 fee to release it

- Doesn’t refinance vehicles with over 85K miles or older than 8 years

- Not available in Alabama, California, Delaware, Indiana, Louisiana, Mississippi, Nevada, Rhode Island, Vermont, or Washington

| Rates (APR) | Starting at 6.83% |

| Loan amounts | $10,000 – $150,000 per vehicle |

| Repayment terms | 63-month initial term |

Carputty offers a new way to handle all your auto financing needs by combining everything into a one-size-fits-all line of credit. You can use this line of credit to buy a new or used car, refinance an auto loan, or buy out your lease.

Carputty auto loans at a glance

Carputty financing operates as a line of credit, but it works by giving you access to separate loans when you need them without having to reapply. Each car has its own payment schedule, but you’ll make one single monthly payment for all.

| Term | Details |

| Loan amounts | $10,000 – $150,000 per vehicle |

| Term lengths | 63-month initial term |

| Rates (APR) | Starting at 6.83% |

| Fees | 1% origination fee, $250 asset removal fee when a car is removed |

Carputty uses a hybrid interest rate approach. The interest rate can go up or down at any time, similar to a credit card. When you’re ready to take an “Advance” (i.e., an individual auto loan), the rate at that exact time is fixed for the life of that particular car’s repayment.

Am I eligible for Carputty?

Carputty only works with borrowers who have good or excellent credit. It performs a soft credit check, which doesn’t affect your credit score, every 45 days to ensure you still meet Carputty credit requirements.

When it comes to your vehicle, the requirements are essentially the same for whichever type of loan you’re applying for, with one exception, noted below.

| Requirement | Details |

| Min. credit score | 680 |

| Max vehicle age | 8 years |

| Max mileage | 85,000 miles |

| Location | Not available in Alabama, California, Delaware, Indiana, Louisiana, Mississippi, Nevada, Rhode Island, Vermont, or Washington |

| Max loan-to-value ratio | New cars: 100% of V3 value (or 100% of MSRP when V3 value isn’t available) Used cars: 110% of V3 value (or 90% of MSRP when V3 value isn’t available) |

| Loan amount per vehicle | $10,000 – $150,000 |

| Max combined loan amount | $250,000 |

| Insurance requirements | Full coverage, plus a max deductible of $1,500 |

| Other restrictions | No commercial or business vehicles (other than Turo vehicles). No salvaged or branded-title vehicles. No motorcycles, RVs, aircraft, or watercraft. |

Pros and cons of a Carputty auto loan

Carputty is different from any other car loan you’ve taken out before, so it’s wise to consider all the pros and cons before applying.

Pros

-

Excellent live chat support

-

Available to individuals and Turo hosts

-

Quick same-day funding via wire transfer

-

Combine all auto loans into one payment

-

No need to reapply every time you refinance or buy a car

-

V3 valuation tool allows you to time a sale or new car purchase

-

On-demand line of credit allows you to jump on purchases without delay

-

High Flexline limits (up to $250,000) give you lending flexibility and allow you to cover multiple vehicles with one monthly payment

Cons

-

Not available in California, Mississippi, and Nevada

-

Doesn’t allow joint applicants or cosigners

-

Reports of some dealerships not accepting Carputty loans

-

RVs, motorcycles, boats, and custom vehicles not allowed

-

No choice of term length options; a long 63-month term is standard

-

Tighter vehicle restrictions than many other auto refinancing lenders

-

Doesn’t allow private-party purchases; can only purchase from dealerships

-

Origination and vehicle release fees can add up if you buy, sell, or refinance often

-

Interest rates on the line of credit are variable and can increase before you’re ready to buy or refinance

-

May encourage unnecessary borrowing because it becomes inactive if you go for more than 24 months with no cars on your account

Is Carputty a reputable company?

| Source | Rating (out of 5) | Number of reviews |

| Better Business Bureau | 1.0 | 2 |

| 4.2 | 76 | |

| Trustpilot | 3.3 | 13 |

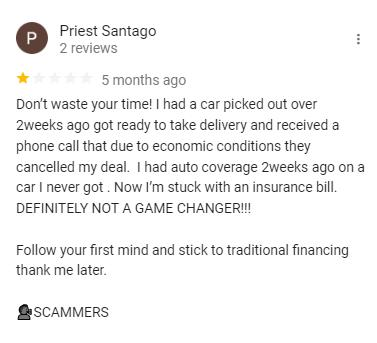

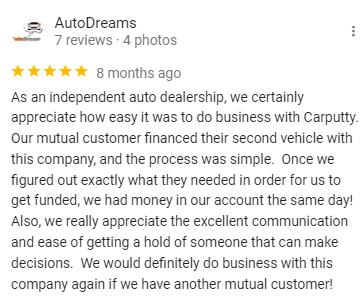

Carputty has only been around since 2021. Given that it’s so new, we’re not shocked to see customers reporting growing pains.

A common comment is that Carputty changed the availability or terms of the lines of credit people already have open. Some customers also report issues finding a dealership willing to accept funds from Carputty because they aren’t familiar with it.

However, plenty of customers are happy with Carputty, praising its quick speed and helpful customer service. Even dealerships mention how easy it is to work with Carputty:

How do I apply with Carputty?

Carputty makes it easy to get started. You can even sign up for a free account to track your car’s V3 value if you want to familiarize yourself with how the company works before you apply.

Here’s how to apply:

- Sign up for an account: You’ll need to enter your name, address, and contact information. Carputty will ask what you’re interested in applying for during the setup process.

- Get preapproved: After you select which type of loan you’re looking for (at the moment, that is), Carputty will do a soft credit check and notify you of your potential rates and terms and how they work.

- Finalize your line of credit: If you like what you see, you can proceed with a full application for a line of credit. You’ll then link your bank account with Plaid and submit to a hard credit check.

- Review the lending decision: If you’re approved for a line of credit, Carputty will notify you. You’ll then sign a lending agreement. Be sure you read the terms carefully so you understand.

- Add a car to your line of credit: To use your line of credit, you’ll request an Advance by adding the car you want to buy or refinance to your account. Carputty will guide you through the rest of the steps.

- Request funds: Carputty will verify that the car you’ve added is eligible for financing. If you’re approved, Carputty sends the funds to the dealership where you’re buying the car (or to your current lender for a refinance loan) via a wire transfer or next-day check.

- Wrap up the final details: Carputty will help you handle the title transfer. It will also charge you its 1% origination fee, which is added to your loan balance. When you’re ready to pay off the car, it will charge another $250 release fee.

Does Carputty have a customer service team?

If you have questions about a new or open Carputty Flexline or want to speak with a customer service team member, Carputty offers two methods for contacting the company:

- Chat live with a customer service agent through the Carputty website. Agents are available Monday through Friday from 8 a.m. to 6 p.m. Eastern time.

- Send an email to [email protected].

How we rated Carputty

We designed LendEDU’s editorial rating system to help consumers identify companies that offer the best financial products. Our experts spend hours researching these companies each year to ensure our ratings are fresh and accurate.

Our most recent evaluation compared Carputty to several auto lenders across a number of factors, including rates, fees, transparency, and customer experience. We weighted, scored, and combined these factors to produce a final editorial rating. This rating is expressed on a scale from 1 to 5, with 5 being the highest possible score. We round all ratings to the nearest tenth decimal place.

| Product | Best for | LendEDU rating |

| Auto loan refinance | Lifetime financing | 4.6 out of 5 |

About our contributors

-

Written by Lindsay VanSomeren

Written by Lindsay VanSomerenLindsay VanSomeren is a personal finance writer living in Suquamish, Washington. She's passionate about helping people manage their money better so that they can live the life they want. In her spare time, she enjoys outdoor adventures, reading, and learning new languages and hobbies.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.