Although we all hope there is never a need for it, insurance can be invaluable if the unexpected happens.

No one expects or desires an apartment fire, but renters insurance is nice to have at such a moment. Car crashes are quite unpleasant, but if you happen to be involved in one, having collision coverage as part of your auto insurance policy is useful.

But when it comes to life’s big inevitable event – death – a life insurance policy can help in many ways. The fundamental reason to own a life insurance policy is to ensure that the policy holder’s dependents are financially secure should he or she pass away.

Deciding whether to purchase a life insurance policy can be a difficult financial decision to make – not only because of the costs, but also because the topic can be challenging to fully grasp.

LendEDU sought to find out some answers on American’s thoughts on life insurance, so we did what we always do: conduct a survey. Our life insurance-focused survey of 1,000 adult Americans revealed the following key findings:

- 54% of respondents currently have a life insurance policy. 83% of these respondents thought their life insurance policy is worth the cost, but 33%indicated that they do not fully understand how their policy works.

- Among those who do not have a life insurance policy, 53% said they still plan on getting one in the future, while 18% do not and 29% were not sure.

- 65% of poll participants who are currently repaying student loan debtstated that they would rather have an equally valuable monthly student loan payment made toward their debt as opposed to a free life insurance policy provided by their employer.

Full Survey Results

(All survey results derive from an online poll of 1,000 adult Americans conducted by Pollfish and commissioned by LendEDU.)

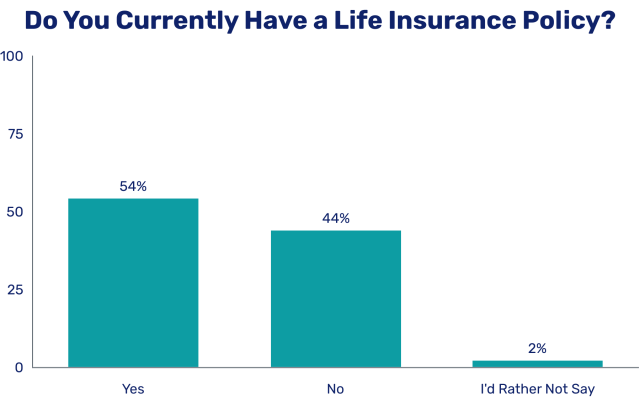

1. Do you currently have a life insurance policy?

a. 54 percent of respondents answered “Yes”

b. 44 percent of respondents answered “No”

c. 2 percent of respondents answered “I’d rather not say.”

2. (Asked only to those who answered “B” to Q1) Which of the following best describes why do you not have a life insurance policy?

a. 20 percent of respondents answered “I have not even thought about it.”

b. 12 percent of respondents answered “I didn’t think it was worth the cost.”

c. 44 percent of respondents answered “I can’t afford one.”

d. 6 percent of respondents answered “I don’t understand how the process works.”

e. 1 percent of respondents answered “I applied but I wasn’t able to qualify for a life insurance policy.”

f. 12 percent of respondents answered “Another reason not listed.”

g. 5 percent of respondents answered “None of the above.”

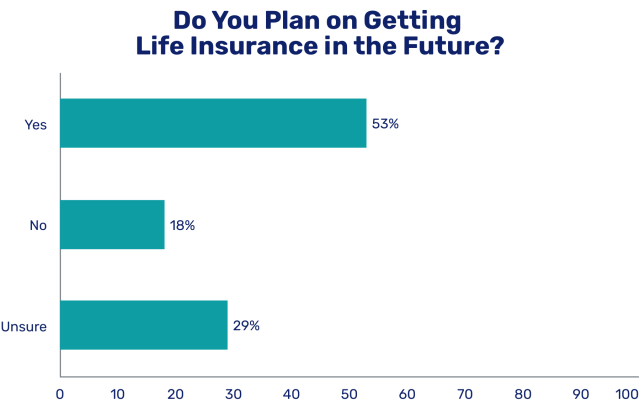

3. (Asked only to those who answered “B” to Q1) Do you plan on getting life insurance in the future?

a. 53 percent of respondents answered “Yes”

b. 18 percent of respondents answered “No”

c. 29 percent of respondents answered “Unsure”

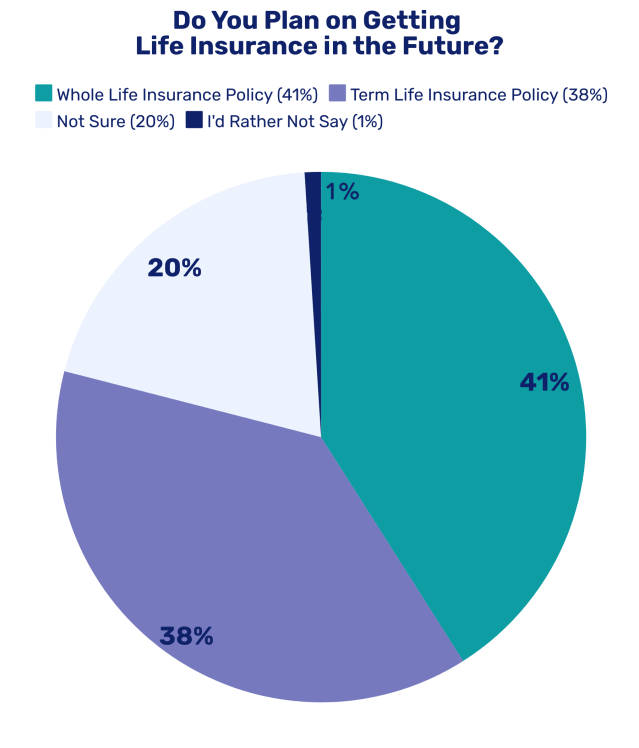

4. (Asked only to those who answered “A” to Q1) Which type of life insurance policy do you currently have?

a. 38 percent of respondents answered “Term life insurance policy”

b. 41 percent of respondents answered “Whole life insurance policy”

c. 20 percent of respondents answered “Not sure”

d. 1 percent of respondents answered “I’d rather not say.”

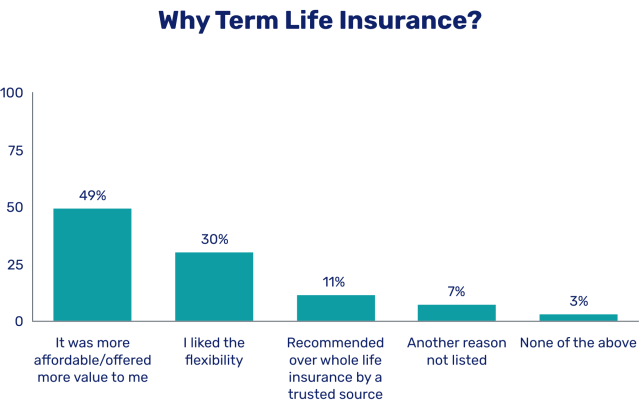

5. (Asked only to those who answered “A” to Q1 and “A” to Q4) Which of the following best describes why you selected a term life insurance policy vs. a whole life insurance policy?

a. 30 percent of respondents answered “I liked the flexibility of a term life insurance policy better.”

b. 49 percent of respondents answered “Term life policy was more affordable/offered more value for me.”

c. 11 percent of respondents answered “I was recommended to get a term life insurance policy instead of a whole life insurance policy by a trusted source.”

d. 7 percent of respondents answered “Another reason not listed.”

e. 3 percent of respondents answered “None of the above.”

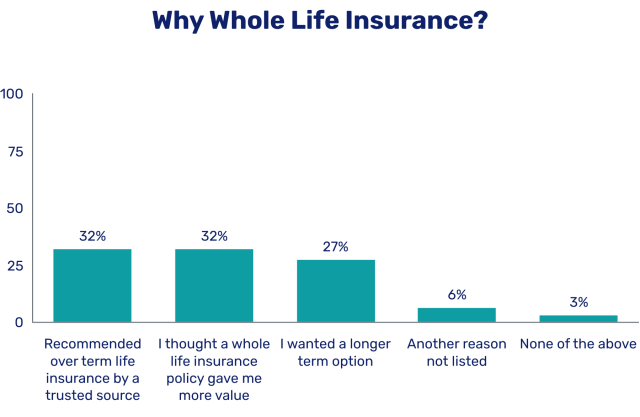

6. (Asked only to those who answered “A” to Q1 and “B” to Q4) Which of the following best describes why you selected a whole life insurancepolicy vs. a term life insurance policy?

a. 27 percent of respondents answered “I wanted a longer term option.”

b. 32 percent of respondents answered “I was recommended to get a whole life insurance policy instead of a term life insurance policy by a trusted source.”

c. 32 percent of respondents answered “I thought a whole life insurance policy gave me more value.”

d. 6 percent of respondents answered “Another reason not listed.”

e. 3 percent of respondents answered “None of the above.”

7. (Asked only to those who answered “A” to Q1) Which of the following best describes why you took out a life insurance policy?

a. 35 percent of respondents answered “To replace lost income for my family/dependents if something ever happened.”

b. 30 percent of respondents answered “To cover burial expenses.”

c. 6 percent of respondents answered “To pay off family’s debt.”

d. 1 percent of respondents answered “To pay for family’s college expenses.”

e. 3 percent of respondents answered “To build cash value.”

f. 1 percent of respondents answered “To diversify my investments.”

g. 1 percent of respondents answered “Business planning.”

h. 6 percent of respondents answered “I was recommended to get a life insurance policy by a trusted source.”

i. 13 percent of respondents answered “I just know that it is an important thing to have.”

j. 4 percent of respondents answered “Another reason not listed.”

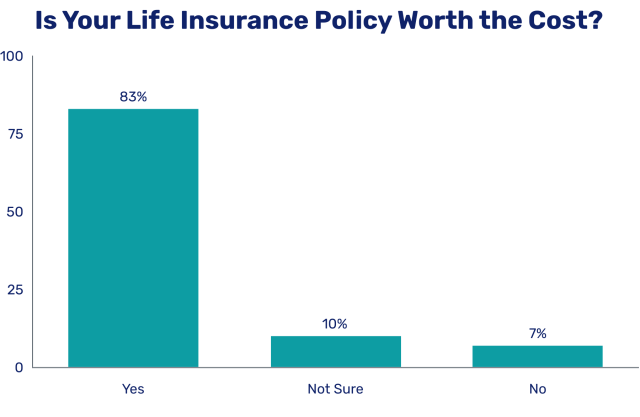

8. (Asked only to those who answered “A” to Q1) Ultimately, do you think your life insurance policy is worth the cost?

a. 83 percent of respondents answered “Yes, it is worth the cost.”

b. 7 percent of respondents answered “No, it is not worth the cost.”

c. 10 percent of respondents answered “Not sure”

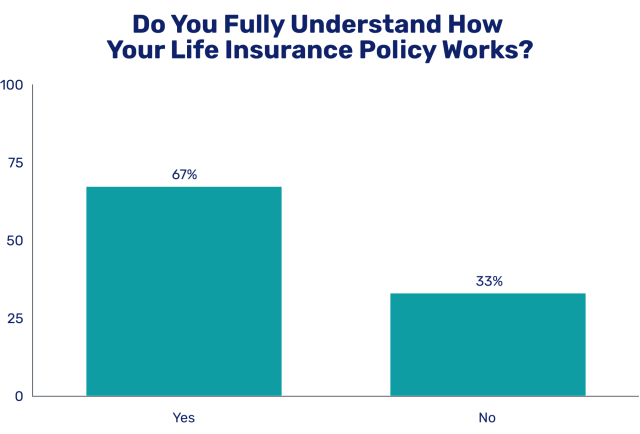

9. (Asked only to those who answered “A” to Q1) Do you believe that you fully understand how your life insurance policy works?

a. 67 percent of respondents answered “Yes, I fully understand how it works.”

b. 33 percent of respondents answered “No, I don’t fully understand how it works.”

10. (Asked only to those who answered “A” to Q1) How did you find your insurance policy?

a. 46 percent of respondents answered “A family member, friend, or colleague referred me to a particular company.”

b. 14 percent of respondents answered “My financial advisor referred me to a particular company.”

c. 24 percent of respondents answered “My insurance agent.”

d. 11 percent of respondents answered “Researching online through Google or another search engine.”

e. 5 percent of respondents answered “I saw an advertisement on t.v., the internet, or in-person.”

11. Over the past few years, an increasing number of startups have begun offering life insurance products. Would you trust a startup company to provide life insurance for you?

a. 20 percent of respondents answered “Yes, I would trust a startup company.”

b. 42 percent of respondents answered “No, I would not trust a startup company.”

c. 38 percent of respondents answered “Unsure”

12. Are you currently working to repay student loan debt?

a. 24 percent of respondents answered “Yes”

b. 76 percent of respondents answered “No”

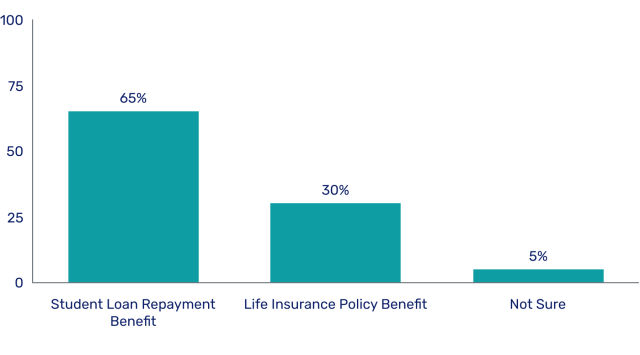

13. (Asked only to those who answered “A” to Q12) If given the option, would you rather have a free life insurance policy provided by your employer or an equally valuable payment made towards your student loan debt each month?

a. 30 percent of respondents answered “Life insurance policy benefit”

b. 65 percent of respondents answered “Student loan repayment benefit”

c. 5 percent of respondents answered “Not sure”

14. Do you think life insurance companies have your best interests in mind or only look at you as a way to make money or lose money?

a. 25 percent of respondents answered “I think they have my best interests in mind.”

b. 47 percent of respondents answered “I think they just look at me as a means to make or lose money.”

c. 7 percent of respondents answered “I’d rather not say.”

d. 21 percent of respondents answered “Not sure”

Observations & Analysis

Over Half of Americans Have Life Insurance, Vast Majority Believe it Is Worth It

In our online poll of 1,000 adult Americans, we found that over half of all respondents, 54 percent, currently have a life insurance policy. This statistic falls right in line with other studies done on life insurance, including LIMRA’s 2018 Insurance Barometer Study that found 60 percent of all people in the U.S. were covered by some type of life insurance.

Amongst those survey participants that currently own a life insurance policy, most of them pointed to one of two reasons when asked why they took out a policy; 35 percent of policy holders want to replace lost income for their dependents should something tragic happen, while 30 percent want their burial expenses to be covered.

When considering life insurance, these are the two often-cited reasons in favor of taking out a policy because we want to ensure our loved ones are financially secure in the event of losing a source of income.

As the above visual represents, the vast majority of respondents that are covered by life insurance believe their policy is worth the associated costs. 83 percent of consumers feel this way, while only 7 percent do not think their policy is worth it, and 10 percent are uncertain.

A life insurance policy can undoubtedly be an expensive month-to-month cost. Depending on the holder’s age and health, the monthly cost can range from $20 to well over $1,000. However, it seems that most of our insured respondents understand the value of the expense and realize how rocky things could become were something to happen, and they did not have a life insurance policy.

Yaron Ben-Zvi, CEO of life insurance company Haven Life, explained how consumers can make their life insurance policies work for them and why it is important to have one. “Life insurance needs aren’t one-size-fits-all,” he said. “Regardless of the exact amount of coverage you need, the idea is that your policy should help protect your beneficiary from financial hardship should anything happen to you.”

He continued, “Therefore, the amount of coverage you purchase should take into account your expenses such as the mortgage or rent, childcare, debts, and any other day-to-day bills you or your family may have.”

Interestingly, despite many poll participants having a life insurance policy and believing in its worth, one-third of policy holders indicated that they do not fully understand how their respective policy works. Life insurance policies can often be long-winded and difficult to grasp, so much so that even policy holders are not entirely sure what they are paying for or how their policies even work.

Further, the opacity of life insurance likely holds back many consumers from taking out a policy because they do not even know where to begin. One study found that 83 percent of Americans would consider life insurance “more intently” if it was easier to understand.

Focusing on those consumers who do not have life insurance, we asked non-policy holders if they plan on getting life insurance in the future.

The results of our survey came back to find that more than half of survey takers, 53 percent, anticipate owning a life insurance policy in the future, while 29 percent are unsure. Another 18 percent bluntly said that they have no intentions on ever taking out a life insurance policy.

Term Life vs. Whole Life: Near Even Split

When in the market for a life insurance policy, there are two main types that a consumer can opt for: term life insurance or whole life insurance.

A term life policy is commonly seen as the more flexible and affordable option. Term life holders have a few choices in terms of length of the policy, usually something like 10, 20, or 30 years. Premium payments for a term life insurance policy are commonly fixed, and the policy will cancel if premiums are not paid. Generally, a term life policy will be from five to 10 percent of the cost of a whole life policy.

Other than being more expensive, a whole life insurance policy differs from a term life in that it offers guaranteed lifetime coverage so long as all premiums are met. Whole life policies also often have a cash value that builds over time; if the cash value grows large enough, a policy holder can take out a loan against the policy to use for something like paying for a child’s education.

Anyways, back to the survey. We asked our poll participants who currently own life insurance which type of policy they have…

In terms of type of policy, there was a near even split when it came to our respondents who owned life insurance. 38 percent of survey takers had a term life policy, while 41 percent had a whole life insurance policy. One percent opted not to disclose their policy type, while 20 percent were not sure which policy they held, which is quite concerning.

Among those who knew which type of policy they owned, we went a step further and asked them why they went in the direction they did.

For those Americans who hold a term life policy, the most common reasons for going that route played into the strengths of all term life insurance policies: flexibility and affordability. 30 percent of respondents said they preferred the flexibility of a term life policy, while 49 percent pointed to the affordability and value of a term life policy.

Interestingly, only 11 percent of term life policy holders said that they received a recommendation from a trusted source to go with a term life instead of a whole life insurance policy. In comparison, 32 percent of whole life policy holders said that they went with a whole life plan because someone they trust recommended it.

Other prevalent reasons for selecting a whole life policy included consumers wanting a longer term option (27 percent) and believing that this type of policy offered more value (32 percent).

Karen Lee, a Certified Financial Planner and founder of Karen Lee and Associates, a financial planning company, offered her advice on whether one should opt for a term life or whole life policy: “Both have their place in the marketplace. Term is inexpensive, especially when you are younger and possibly the best way to insure against premature death. However, most people die of old age, and if you want life insurance coverage that will pay a death benefit later in life, you must go with permanent insurance.”

Free Employer Life Insurance or Equally Valuable Student Loan Payments: Two-Thirds Want the Debt Payments

Being a company that stays involved with the student loan industry, we just had to figure out a way to work student loan debt into this survey. First, we asked our 1,000 adult American respondents if they are currently working to repay student loan debt, and 24 percent of them were. We asked this contingent a follow-up question in which we pitted student loan payments against a life insurance benefit.

Just under two-thirds of the respondents with student loan debt, 65 percent to be exact, stated that they would prefer the equally valuable student loan payment each month as opposed to a free life insurance policy provided by their employer. 30 percent opted for the latter, while five percent were undecided.

As mentioned earlier, the average monthly life insurance cost can range from $20 to well over $1,000 depending on the consumer’s unique circumstances. A monthly student loan payment of $20 may not mean much, but anything over $100 per month could cut away a significant amount of student debt over time.

One important thing to consider for this particular question is the age of the applicable respondents that have student loan debt. Presumably, the younger respondents are going to be the ones with student loan debt and repayment is likely a top priority. Further, young poll participants are probably more confident in their health and lack dependents, both of which lessen the necessity for a life insurance policy. In this case, opting for the student loan payment seems like a no-brainer.

John Espenschied, the Owner of Insurance Brokers Group, shared his suggestion for someone stuck in this hypothetical situation: “If I was a young single person with no dependents I would probably opt for the student loan repayment benefit. Getting your debt reduced will reduce the amount of life insurance you’ll need in the future, since you’ll have little or no debt that needs paying off.”

After reviewing the age demographics of those poll participants who preferred the monthly student loan payment, 63 percent of them were between the ages of 18 and 34, while another 20 percent were between the ages of 35 and 44.

Questions You Should Ask Before Taking Out a Life Insurance Policy

Taking out a life insurance policy is a consequential financial decision so you need to be absolutely sure that life insurance is right for you and something that you can afford.

Below, LendEDU lists a few questions you should ask yourself before committing to life insurance.

Is Life Insurance Really Worth it For Me?

As noted above, life insurance is a consequential financial decision that you need to be prepared and ready for before moving forward with it. And before moving forward, you must decide if life insurance is worth it based on your specific financial and family situation.

Further, depending on what type of life insurance product you are considering, you must also ask yourself if either whole insurance is worth it or if term life insurance is worth it if you decide to go with the latter.

What Life Insurance Policy is Right For Me?

We just mentioned both whole life insurance and term life insurance but haven’t explained either yet. When it comes to life insurance, those are the two main types of products you can select from.

Whole life insurance provides lifetime insurance coverage and policies also accrue a cash value. Meanwhile, term life insurance is a policy that both provides you with an appropriate death benefit and charges affordable premiums for coverage.

How Much Life Insurance Do I Need?

Finally, you must also ask yourself how much life insurance you need before making a final decision on a life insurance product. When calculating how much life insurance you need, things you must consider include your outstanding debts, your annual salary, and your future financial obligations.

By getting a good sense of how much life insurance you truly need, you can feel secure in your coverage while also not making a financial commitment that you can’t sustain.

Methodology

All results found within this report derive from an online poll commissioned by LendEDU and conducted online by polling company Pollfish. In total, 1,000 Americans ages 18 and up were surveyed. The properly-aged respondents were found via Pollfish’s age filtering feature. Respondents were selected randomly from Pollfish’s online user panel of over 100 million. This survey was conducted over a two-day span, starting on Aug. 2, 2018 and ending on Aug. 3, 2018. Respondents were asked to answer all questions truthfully and to the best of their abilities.

See more of LendEDU’s Research

About our contributors

-

Written by Mike Brown

Written by Mike BrownMike Brown uses data from surveys and publicly available resources to identify emerging personal finance trends and tell unique stories.