Living paycheck to paycheck means your money runs out before the month does. There’s no cushion, no breathing room … just a race to make it to the next payday without falling behind.

It’s more common than you might think. LendEDU’s 2025 Personal Finance Survey found that 53% of Americans say they’re living paycheck to paycheck.

And it’s not just low earners—this struggle spans every income level and age group.

But breaking the cycle can bring freedom. The kind where you can handle surprise bills, save for the future, and make choices that feel good (not just necessary). Here’s what it really means to be living paycheck to paycheck in 2025 and how to change it.

Table of Contents

What does living paycheck to paycheck mean?

Living paycheck to paycheck means all your income goes toward covering basic expenses—like rent, groceries, and bills—with little or nothing left over. If a surprise bill hits, there’s no savings to fall back on. Just crossed fingers and maybe a credit card.

You don’t have to be broke to be living paycheck to paycheck, either. Many people earning $50,000, $75,000, or even $100,000 or more still feel trapped. High costs, student loans, or family responsibilities can eat up even a solid income.

If you’re unsure whether you fall into the “living paycheck to paycheck” category, here are a few signs:

- You regularly wait for payday to cover essentials.

- You have no emergency fund (or it’s under $500).

- You rely on credit cards to float between checks.

- An unexpected $100 or $1,000 expense would throw everything off.

Living paycheck to paycheck doesn’t automatically mean you’re financially irresponsible. It’s often a reflection of systemic issues, rising costs, and how hard it is to build margin when everything feels urgent.

Example of living paycheck to paycheck

Meet Anna. She’s a 32-year-old project manager making $68,000 a year. After taxes, she brings home about $4,300 a month.

From there, she pays $1,500 for a two-bedroom apartment, $400 for groceries, $500 for student loans, $300 for health insurance, $800 for child care for her two-year-old, and $500 for her car payment. That leaves her with just $300 for gas, household essentials, and everything else.

When her dog needed an unexpected $700 vet visit, she had no choice but to charge it to her credit card. Now she’s paying it off bit by bit, but it’s stretching her budget even thinner. If she experiences another emergency, she may have to charge that to her card, too, which would only strengthen the cycle she’s trapped in.

How many Americans live paycheck to paycheck in 2025?

More than half of Americans (53%) say they’re living paycheck to paycheck, according to LendEDU’s 2025 Personal Finance Survey. That means over half the country is one unexpected expense away from falling behind.

And it’s not just a low-income issue. Here’s how it breaks down by income:

- 72.8% of people earning under $50,000 are living paycheck to paycheck.

- 44% of people earning $50,000 to $99,999.

- 32.3% earning $100,000 to $149,999.

- Even 20.6% of households earning $150,000 or more say they’re still stuck in the cycle.

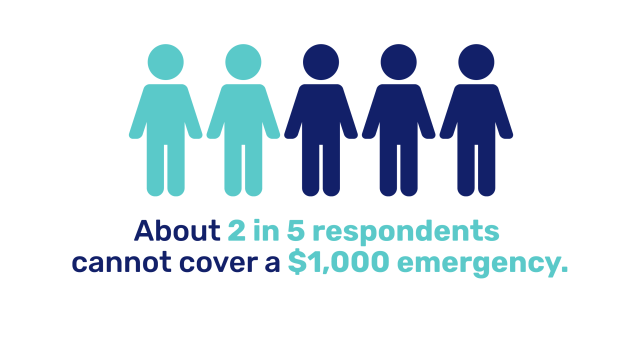

This financial strain also shows up when we look at savings—40.1% of people said they couldn’t cover a $1,000 emergency in cash. Among them, 34% would turn to a credit card, and others would borrow from friends, delay the bill, or simply not know what to do.

It tracks with national trends: The average U.S. personal savings rate was just 4.6% for February 2025, according to BEA.gov. This is a stark reminder of how little margin most households have for saving money.

The paycheck-to-paycheck lifestyle touches all regions and age groups:

- 68.5% of Gen Z and 56.5% of millennials are the most affected.

- Gen X isn’t far behind at 54.5%.

- Even 41.5% of baby boomers report living this way.

- Regionally, the South (57%) and Northeast (54.6%) see the highest rates.

Why do so many Americans feel trapped in the cycle?

There’s no single reason so many people live paycheck to paycheck. It’s a perfect storm of pressures. On the economic side, inflation, housing costs, and high interest rates on loans all contribute. Because many incomes haven’t kept pace, it’s been harder for people to build any breathing room.

But it’s not just about the numbers. Living paycheck to paycheck also takes a toll mentally and emotionally.

When every dollar is already spoken for, it can feel impossible to plan ahead. There’s stress, shame, and burnout. Some people give up on budgeting because it feels like nothing ever changes. Others avoid checking their bank account entirely.

This survival mode mindset is common. And it makes sense. When you’re trying to get through the week, long-term planning feels like a luxury.

When I work with clients living paycheck to paycheck, I begin by reassuring them that their situation is common and that they are not failing in any way. From there, I recommend budgeting apps to help them gain clarity on where their money is going and identify areas where they can cut back or make adjustments. I’ll also advise them to prioritize essential expenses—food, utilities, housing, and transportation (often referred to as “the Four Walls”)—with everything else considered secondary or negotiable.

8 realistic ways to stop living paycheck to paycheck

If you’re stuck in the paycheck-to-paycheck cycle, you’re not alone—and you’re not doomed to stay there. Here are eight practical ways to start making space in your budget and build a little momentum.

1. Get clear on what’s actually coming in and going out

Track every dollar you earn, not in your head, but on paper or in a budgeting app. Most people underestimate their spending. Awareness is the first step toward change.

2. Build a “bare minimum” budget

List only your essential expenses: rent, food, bills, insurance. Knowing your baseline helps you see what’s truly nonnegotiable and what’s not.

3. Stop trusting your bank’s “available balance”

Just because your account says $1,000 doesn’t mean you have $1,000 to spend. If $900 of that goes to rent next week, you’re really working with $100.

4. Set one small emergency fund goal

Start with $500 or $1,000. Even a tiny safety net can keep a car repair or medical bill off your credit card.

5. Pick one high-interest debt to tackle

Focus on one balance—whether it’s the smallest or the one with the highest rate—and throw extra money at it consistently, even if it’s just $10. Momentum builds confidence.

6. Automate one positive money move

Set up $10 a week to savings or automate a bill payment. Taking just one task off your mental load can make managing money feel easier.

7. Find your “leak” and plug it

Takeout? Target runs? Forgotten subscriptions? Find the habit that quietly drains your cash and cut it back just a little.

8. Add in a little joy

Budgeting shouldn’t feel like punishment. Plan one small splurge a month, even if it’s a new book or thrift find.

What to do this week if you’re stuck living paycheck to paycheck

One week of mindful decisions can be the spark that helps you shift out of the paycheck-to-paycheck cycle. If you’re in survival mode, don’t try to overhaul everything. Instead, choose one small step you can take right now:

- Track your spending for the past seven days. Even if it’s messy or surprising, it’s valuable information.

- Cancel one unused subscription. That $12 a month could go toward savings or debt.

- Stash $10 in a separate savings account. Having money is important. It might feel small, but it’s a start.

- List your non-negotiables. What has to get paid this week? Knowing your priorities helps you avoid panic spending.

- Say “no” to one expense. Maybe it’s takeout. Maybe it’s an Amazon buy. Give yourself the win of choosing to pause.

What life looks like when you’re no longer living paycheck to paycheck

Breaking free from living paycheck to paycheck doesn’t mean you’re suddenly rich. It just means you have options.

You can pay your bills without panic. You can say yes to a weekend trip or take a break from a toxic job. A surprise expense doesn’t ruin your month. And maybe for the first time in a long time, you feel like you’re in control.

Even small changes (like a $500 emergency fund or one less debt payment) can make life feel lighter. You stop avoiding your bank account. You sleep a little better. And you finally get to use your money for things that bring peace, not pressure.

This work isn’t easy, but it’s worth it. And you don’t have to do it all at once. One week, one win at a time is enough to start changing your story.

I worked with a couple who had a combined income of $250,000, plus a military pension—yet they were still living paycheck to paycheck. Despite their stable income, they were burdened with several personal loans and carried balances on multiple credit cards.

Together, we built a budget that helped them clearly separate essential expenses from negotiable ones. By trimming non-essential spending, we freed up funds to aggressively tackle their debt using the avalanche method—starting with the credit card carrying the highest interest rate and moving down from there.

Within 24 months, they became completely debt-free (excluding their mortgage) and, most importantly, broke free from the paycheck-to-paycheck cycle.

If you’re not sure where to start, you don’t have to do it alone. A free 45-minute session with a vetted financial advisor from Money Pickle could help you understand your current situation and find a few actionable ways to create breathing room—even if you’re living paycheck to paycheck.

FAQ

Why are people making six figures living paycheck to paycheck?

Earning six figures doesn’t guarantee financial stability, especially if your spending habits rise with your income. This is called lifestyle inflation, and it’s one of the most common reasons high earners still struggle financially.

Add in rising costs for housing, child care, healthcare, and debt payments, and it’s easy to see how someone earning $100,000 or more could still feel stretched thin.

How do I stop living paycheck to paycheck and save my first $1,000?

Start by tracking every dollar you earn and spend. Once you know where your money is going, look for small cuts—like canceling unused subscriptions or eating out one less time per week. Automate your savings, even if it’s just $10 a week.

Consider using a separate savings account to make it harder to spend the money impulsively. The first $1,000 is the hardest, but it builds the momentum you need for bigger goals.

How much of your paycheck should go to living?

A simple rule of thumb is the 50/30/20 rule. That means 50% of your take-home pay goes to needs like rent, groceries, and utilities; 30% to wants; and 20% to savings and debt repayment. If you’re spending more than 50% on essentials, you may need to adjust other areas or find ways to boost your income.

Can I stop living paycheck to paycheck if I earn minimum wage?

It’s tough, but it is possible with the right support and strategy. The key is making every dollar count: take advantage of community resources, cut unnecessary expenses, and find even small ways to increase income—like side gigs or cash-back apps.

Saving even $5 or $10 a week adds up. It may take longer, but you’re still building progress. And once your income grows, those habits will help you stay ahead instead of falling behind.

About our contributors

-

Written by Cassidy Horton, MBA

Written by Cassidy Horton, MBACassidy Horton is a finance writer passionate about helping people find financial freedom. With an MBA and a bachelor's in public relations, her work has been published more than 1,000 times online.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.