Quick Overview

According to College Atlas, 70 percent of Americans will study at a 4-year college, but less than two-thirds of them will graduate with a degree.

When it comes to freshmen in the U.S., 30 percent of the bright-eyed and bushy-tailed students will drop-out after just one year at campus.

The decision to attend a college or university is a transformative one. However, the decision to drop-out has ramifications that are even more life-changing.

Those without a college diploma are two-times more likely to be unemployed than graduates. A male with a college degree will make roughly $900,000 more in median lifetime earnings than a male with only a high school degree, while a college-educated female will make $630,000 more than a female high school graduate.

Of course, there are outliers (see: Bill Gates, Steve Jobs, Mark Zuckerberg, etc.), but you get the picture.

A college degree from a college or university in the U.S. is valuable; in fact, a degree has a higher return on investment for a U.S. graduate than in any other place on the planet. But, for however much worth an American diploma carries, that little piece of archival paper is incredibly expensive to attain.

So expensive that LendEDU reports about 60 percent of all college graduates require student loan debt to complete their coursework. Additionally, the average borrower will owe roughly $27,975 in student debt.

The point to be made is that perhaps many college dropouts are forced into their situation by circumstance, not choice. At some point, most college student must ask themselves if racking up the student loan debt in order to attain a college degree is worth it.

LendEDU sought to answer these questions by going to straight to the source: We polled 1,000 college dropouts who have student loan debt to better understand their reasoning and current situation.

Average College Dropout Leaves Campus With Over $10,000 in Student Loan Debt

LendEDU polled 1,000 respondents that had dropped-out of a four-year higher education institution and also held some amount of student loan debt. We wanted to find out how much student loan debt they owed when the walked away from college.

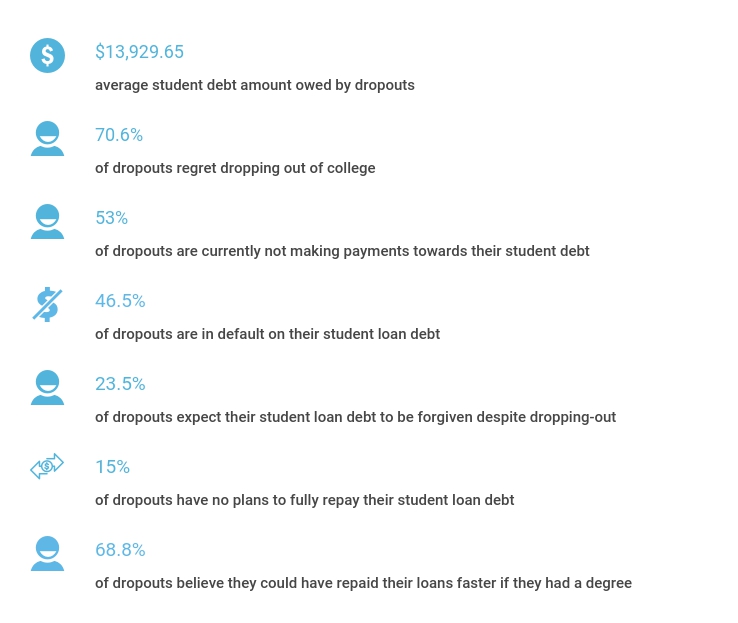

Respondents were given the ability to enter in an exact dollar amount when asked how much student loan debt they held when they made the choice to drop-out of school. After averaging together all 1,000 responses, we found that when the average college dropout finally gave up on college, they owed $13,929.65 in student loan debt.

LendEDU pegs the average student loan debt per graduated borrower figure at $27,975, so the aforementioned debt per dropout amount makes good sense. Under the assumption that most dropouts leave campus by the end of their second year, the debt per dropout figure is nearly half of the four-year debt per borrower figure of $27,975. That figure cut in half would equal $13,987.50, a tick above our debt per dropout figure of $13,929.65.

But, how are college dropouts doing today when it comes to paying down that student loan debt?

More Than Half of College Dropouts Are Not Making Payments Toward Their Student Loan Debt

We asked our respondents the following question: “Are you currently making payments towards your student loan debt?”

Although only by a slim margin, the majority of college dropouts (53%) with student loan debt are currently not making payments to knock down their student loan debt. Meanwhile, 47 percent are presently making contributions towards their educational debt.

Although circumstances could be making things challenging, more college dropouts should be in the act of paying off their student loan debt. Failure to make payments can bring down a consumer’s credit score, while also allowing interest to accrue and make that mountain of debt even more insurmountable.

Forget staying timely with payments, have student debt-laden college dropouts made any contributions whatsoever? To answer that, our poll participants were asked this question: “Have you made any payments towards your student loan debt since dropping out?”

Even though the minority of respondents have not yet made any payments towards their educational debt, it was still over a third (35.40 percent) of those who participated in this poll. Since dropping out, 64.60 percent of respondents have made at least one student loan payment.

Based off of the results from the question just discussed, it should come as no surprise that 57.20 percent of respondents answered “yes” when we asked them, “Are you currently behind on your payments towards your student loan debt?” Only 42.80 percent of college dropouts answered “no” to that question, indicating that they are not behind on repaying their educational debt.

According to LendEDU’s poll, nearly half, 46.50 percent, of student debtors that dropped out of college are in default on their student loan debt. Contrarily, 53.50 percent of this cohort is not in default on their student loan

Defaulting on any type of loan is never a good thing, but it is even more detrimental for college dropouts. Considering that dropouts make, on average, less than graduates, having their wages garnished or their tax refunds withheld because they defaulted on their student loans could cause irreversible damage.

This series of questions related to college dropouts making payments on their student loan debt did not deliver welcomed results for anyone. Generally, dropouts were not making payments, falling behind, and defaulting on their loans.

We then asked them if they believed this trend was having an impact on their credit scores.

As the above pie chart illustrates, the majority of respondents, 60 percent, believe their credit scores have been negatively impacted due to their student loan debt. 21.40 percent were unsure how their credit scores have been affected, but it is more than likely it has taken a turn for the worse. The lowest percentage of respondents, 18.60 percent, maintained that their credit scores have not been hurt because of their educational debt.

Some Dropouts Are Not Planning to Fully Repay Debt

A few questions from this poll pertained to the future plans of the college dropouts that were surveyed. As such, the following question was asked: “Are you planning to fully repay your student loan debt?”

While the vast majority of respondents, 85 percent, stated that they intended to fully repay their student loan debt, there was still a noteworthy number of college dropouts that indicated they had no plans for full repayment. 15 percent of poll participants answered “no” to the aforementioned question.

Unless that 15 percent is or intends on working a job that will qualify them for student loan forgiveness, simply not repaying their student loans in full is not going to work. They can expect to enter default, at which point their wages will be garnished, tax refunds will be withheld, and their ability to maneuver the financial waters will be made incredibly difficult due to a lack of creditworthiness.

We then proposed this question: “How long do you think it will take you to repay your student loan debt?”

By the slightest of margins, “0 to 5 years” was the answer choice of the plurality of respondents, 33.90 percent. 33.50 percent of college dropouts believed they could repay their student loans in 6 to 10 years, while 13.80 percent stated it would take them over 20 years!

11.10 percent estimated that it would them anywhere between 11 and 15 years to fully repay their educational debt. Finally, 7.70 percent of indebted college dropouts, the smallest cohort, answered that repayment would take them between 15 and 20 years.

The final question that dealt with the future intentions of our respondents was phrased as so: “Are you considering going back to college to finish your degree?”

About two-thirds, 64.30 percent, of the 1,000 college dropouts that participated in this poll intended on going back to college to finish up their degrees. Contrarily, 35.70 percent of the respondent poll stated they had no plans to enroll in classes again.

The fact that quite the clear majority of college dropouts with student debt are set on going back to colleges speaks to both the regret in their original choices to drop-out and also the belief that a college degree will greatly aid in their ability to grow their future earning potentials.

That may seem like a characterization, but those two beliefs are actually reinforced by a pair of questions in our poll.

When we asked 1,000 college dropouts with educational debt, “Do you regret dropping out of college?” almost three-fourths, 70.60 percent, of them said “yes.” Only 14.10 percent of poll participants claimed they had not regretted their decisions to leave college before graduating. An additional 15.30 percent were “indifferent” about dropping out.

Why would so many college dropouts regret their decisions to not finish their bachelor’s degrees? Perhaps, it is because they feel a college degree would have landed them a better, higher-paying job that, in turn, would have resulted in a quicker, less detrimental student loan repayment process.

To test this hypothesis, we asked the following: “If you hadn’t dropped out and you received your degree, do you think you would be able to pay back your student loans faster as a result of your degree?”

68.80 percent of our college dropout respondents believed that they would be able to repay their student loan debt faster if they had stayed in school and received their degrees. Only 31.20 percent thought otherwise – implying that a degree would have no impact on their ability to repay their educational debt.

“Financial Reasons” Oft-Cited as Reason for Dropping-Out

The following question was asked to our respondent poll: “Why did you drop-out of college?”

The plurality of college dropouts, 35.30 percent, cited “financial reasons” as the main reason for leaving their respective college campuses. Trailing closely behind was “social/family reasons,” which brought in 34 percent of the vote.

After those two options, there was a significant drop-off. 12.90 percent of poll participants selected “other,” while 11 percent cited “health reasons,” and 5.40 percent dropped-out because of “academic reasons.” Finally, “legal reasons” was an answer option selected by only 1.40 percent of the respondents polled.

Digging further, we asked the 353 respondents that cited “financial reasons” as the main cause for dropping out this question: “More specifically, did you drop out of college because you didn’t want to borrow more student loan debt?”

Around three-fourths (74.79 pecent) of this sub-section of college dropouts responded “yes” to the question found above. Meanwhile, 25.21 percent of those who dropped-out because of financial troubles maintained that student loan debt had nothing to do with their monetary woes.

There were two more questions pertaining to the financials of student debtors who dropped-out of the colleges or universities they were attending. The first one read like this: “Do you regret using student loan debt?”

74.20 percent of college dropouts that are also student debtors regretted their decisions to take out student loans while at a higher education institution. 25.80 percent expressed no such regrets.

The results of this question were not terribly surprising, in fact it would have been thought that more dropouts regretted taking on student loan debt. Because of their decisions to not finish their degrees, all of that student loan debt became essentially worthless, which should have made a higher percentage of dropouts regretful.

A Concerning Number of College Dropouts Do Not Understand Their Repayment Options

The final two questions of LendEDU’s survey pertained to repayment options available to college dropouts with student loan debt. We first asked the following: “Did you expect your student loan debt to be forgiven after you dropped out of college?”

The majority of respondents, 76.50 percent, had no expectations for their educational debt to be forgiven, while 23.50 percent are seemingly anticipating exactly that. Student loan forgiveness only applies to a very small percentage of student loan borrowers, mainly those who have worked in either the government or non-profit sector. Even then, the borrowers must demonstrate a history of successful repayment, which, judging by the results of our other questions, would not apply to many college dropouts.

To be certain, it is not out of the realm of possibilities that a small portion of college dropouts may qualify for student loan forgiveness, but one can only hope this sub-section of student debtors are not paying back their education loans in the hopes that they will simply be forgiven.

The final question was phrased as so: “Do you think you can refinance your student loan debt without a degree?”

40.70 percent, or the plurality, of respondents were unsure if they would be able to refinance their student loans without a degree. 36.80 percent answered that college dropouts could not refinance their educational debt, while 22.50 percent believed they could.

Between the 40.70 percent that were unsure and the 22.50 who believed it possible to refinance their student debt, college dropouts are woefully uneducated to this particular repayment strategy. The majority of student loan refinancing companies have specific underwriting policies that exclude college dropouts from refinancing. Student debtors that lack a degree do not look like the best investment for refinancing companies, and it is easy to understand why.

According to LendEDU, the average rate received after refinancing is 4.82 percent, but that is a privilege reserved for those debtors who appear to have a high chance of successful repayment due to their career outlook and educational backgrounds. Many college dropouts do not meet those guidelines.

Methodology

The results that have been discussed in this report derived from a poll commissioned by LendEDU and conducted online polling company, Pollfish. The poll ran over a four-day span from October 27th, 2017 to October 30th, 2017. All respondents were screened to ensure each of them was a college dropout and a student loan borrower that still has student loan debt. The screener question was the following: “Which of the following best describes your education experience?” Out of six potential answers, the answer that was accepted was the following: “I did not graduate from college, and I do have student loan debt.” In total, 1,000 college dropouts with student debt were polled and asked to answer each question truthfully and to the best of their ability.

See more of LendEDU’s Research

About our contributors

-

Written by Mike Brown

Written by Mike BrownMike Brown uses data from surveys and publicly available resources to identify emerging personal finance trends and tell unique stories.