On the hunt for a new home? Could your current property use some TLC? A VA home improvement loan may be the answer. Service members and surviving spouses can use these loans to buy a house, repair a house, or both.

VA home improvement loans are among the more elusive VA loan options, but you can get many of the same benefits from a standard VA loan. Keep reading to find the best VA lenders, as well as a few VA home improvement loan alternatives.

| Lender | Loan amounts |

| Prime Lending | Up to $1 million |

| VA Nationwide | $50,000 or $200,000, or up to $2 million for extensive renovations |

| Cross Country Mortgage | $35,000 or less |

| Veterans United | $1.5 million and up with Jump Cash-Out Refi |

Best VA home improvement loans

Choosing the right lender for a VA home improvement loan is crucial to ensure you get the best terms and support throughout the process. Here are top VA renovation loan lenders, focusing on why they’re ideal for veterans looking to finance home improvements.

Prime Lending

Why it’s one of the best veteran home improvement loans

Prime Lending is highly regarded for its exceptional service to veterans seeking home improvement loans. The lender’s expertise in VA loans ensures that veterans receive tailored financial solutions that meet their specific needs.

Prime Lending offers competitive rates, flexible terms, and a streamlined application process, making it easier for veterans to access the funds they need to improve their homes. The lender’s commitment to customer service, combined with extensive experience with VA loans, makes Prime Lending a top choice for veterans.

VA Nationwide

Why it’s one of the best veteran home improvement loans

VA Nationwide stands out for its focus on providing personalized loan options for veterans. The lender offers a range of VA home improvement loans designed to accommodate various renovation projects, from minor repairs to major upgrades.

VA Nationwide’s commitment to transparency and its extensive network of lenders help ensure that veterans get the best possible terms and rates. Additionally, the user-friendly online platform simplifies the loan application process, making it accessible for veterans across the country.

Cross Country Mortgage

Why it’s one of the best veteran home improvement loans

Cross Country Mortgage is a top contender for veterans seeking home improvement loans due to its comprehensive VA loan programs and exceptional customer service. The lender offers a variety of loan options, including those specifically designed for home improvements, ensuring that veterans can find the right fit for their projects.

Cross Country Mortgage’s dedicated loan officers guide veterans through every step of the process, providing expert advice and support. The focus on creating a seamless and stress-free experience makes Cross Country Mortgage a reliable choice for veterans.

Veterans United Cash-Out Refinance

Why it’s one of the best veteran home improvement loans

Veterans United is a top choice for Veterans seeking to use their home equity for renovations or major expenses. Its VA Cash-Out Refinance program allows eligible borrowers to convert equity into cash, offering a flexible way to fund home improvements, consolidate debt, or cover other financial needs.

Backed by deep expertise and a strong reputation as the nation’s #1 VA lender, Veterans United provides clear guidance and personalized support throughout the refinancing process. With competitive rates and a focus on helping Veterans achieve their financial goals, Veterans United Home Loans stands out as a trusted partner for those looking to reinvest in their homes.

How does a VA home improvement loan work?

VA home improvement loans help veterans finance repairs in one of two ways:

- Buying a new home: Roll the purchase price of your home, plus approved repair costs, into your loan.

- Fixing up a home you already own: Use your loan for a cash-out refinance.

With a cash-out refinance, you’ll take out a VA home improvement loan that exceeds your current mortgage balance. The new loan will pay off your existing mortgage, and you’ll use the difference for repairs. Confused? It’s simpler than it sounds.

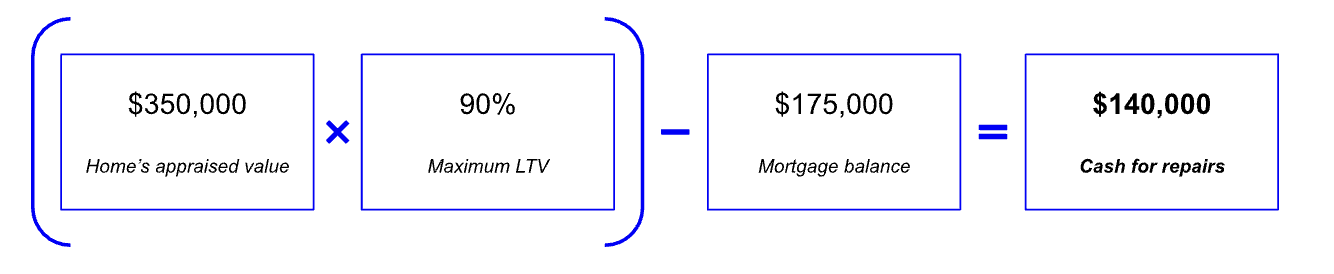

Say your lender will let you borrow up to 90% of your loan-to-value ratio (LTV), which compares what you owe on your home to its value. You owe $175,000, and your home is worth $350,000. In this case, you could pocket $140,000 for repairs.

Whether you’re using your home improvement loan for a new residence or an existing one, you’ll only pay on one loan. If you finance repairs another way, you’d need to juggle at least two separate payments. For many borrowers, that convenience is a prime advantage.

Still, VA home improvement loans can be more complex than other loan types, especially compared to standard VA loans.

VA home improvement loans have many names. Alteration and repair loans, VA rehab loans, VA renovation loans, and VA supplemental loans all refer to the same loan product.

Each of these loans has a similar application and appraisal process, but renovation loans require an additional inspection once repairs are complete. For a closer look at what sets these loans apart, check out the table below.

| Standard VA loan | VA renovation loan | |

| Purpose | Purchase | Purchase or refinance |

| Max origination fee | 1% | 1% |

| Repairs included? | ✖️ | ✔️ |

| Appraisal required? | ✔️ | ✔️ |

| Inspection required? | ✖️ | ✔️ |

Not all repairs are eligible for financing under a VA rehab loan—only those that make your home safer and more habitable. For example, you couldn’t install a new in-ground pool, but you could remove an old one in disrepair.

If your planned repairs won’t qualify, consider applying for a traditional VA loan from these lenders instead:

| Lender | Rates (APR) | Loan amounts |

| Veterans United | 6.52% – 7.07% | No maximum |

| loanDepot | Undisclosed | Up to $2 million |

| New American Funding | Starting at 6.53% | Up to $2 million |

You could also use a home equity line of credit (HELOC). With one of the best HELOCs for veterans, you can pay for repairs without having to restart or replace your mortgage.

VA renovation loan guidelines

It’s a common—and understandable—misconception that all military personnel qualify for VA loans. Your eligibility doesn’t hinge on enlisting alone, however.

The VA’s minimum service requirement means you’ll need 90 continuous days of active-duty service. This requirement may increase to 181 days or more if you served before August 2, 1990.

Don’t meet the active-duty service requirement? You may still be eligible for a VA loan if any of the following apply:

- You’re a current U.S. citizen who served for an allied government during World War II.

- You served in an alternate qualifying capacity (as a Public Health Service officer or as a cadet or midshipman, for example).

- You were discharged for reasons unrelated to misconduct.

With an alteration and repair loan, you aren’t the only one subject to eligibility criteria. Your property, contractors, and renovations all have to pass muster, too. The table below lists supplemental requirements for VA home improvement loans.

| Your… | Must… |

| Property | Serve as your primary residence and pass VA appraisal |

| Renovations | Improve home’s livability |

| Contractors | Have a valid VA builder ID number |

| Timeline | Finish repairs within 120 days of closing |

You could argue that VA rehab loan requirements are more stringent than other types of VA loans. If you’re unsure whether one of these loans is feasible, it may be worth exploring alternatives instead.

What are the types of VA home improvement loans?

There are several other home improvement loans for veterans besides VA rehabilitation loans. Depending on the type of home you want to purchase or the improvements you want to make, you might also consider:

- Farm residence loans: You can use these loans to build, purchase, or repair a farmhouse. If you plan to use farming income to repay your loan, prepare to furnish detailed business information to your lender during the application process.

- Energy-efficient mortgage (EEM) loans: EEM loans can cover up to $6,000 in energy-related improvements, such as installing solar panels or upgrading your thermostats. Note that this isn’t a distinct loan product. Instead, EEM loans are tacked onto regular VA purchase or refinance loans.

Like VA home improvement loans, farm residence and EEM loans are reserved for veterans. There are civilian-eligible options that are worth exploring, as well:

- 203(k) rehab loans: Offered by the Federal Housing Authority (FHA), 203(k) loans function much like VA reno loans. Prospective and existing homeowners alike can leverage these loans to turn a fixer-upper into your forever home.

- Title I property improvement loans: Title I loans are far more lenient when it comes to property type. Manufactured homes, multifamily units, and even commercial buildings are all eligible for Title I loans.

- USDA repair loans: Ideal for countryside dwellers, USDA repair loans help fund home improvements for rural properties. To qualify, your home must be in a designated eligibility tract. Your salary also can’t exceed the very low income threshold for your county.

In addition to filling niche needs for future and current property owners, these loans are a solid alternative for veterans who don’t meet minimum service requirements for a standard VA loan.

Can you get VA home improvement grants?

Depending on your situation, you might qualify for a VA home improvement grant. Unlike loans, grant eligibility isn’t based on credit. Grants also don’t have to be repaid. Not only can grants help you avoid a hard credit inquiry, they can minimize your overall debt burden, as well.

The VA offers several housing modification grants for disabled veterans, including:

| Grant | Max. award amount* |

| Specially Adapted Housing (SAH) | $117,014 |

| Special Home Adaptation (SHA) | $23,444 |

| Temporary Residence Adaptation (TRA) | $47,130 |

| Home Improvements / Structural Alterations (HISA) | $6,800 |

Curious about other grants for veterans? These organizations can help connect you to grant opportunities near you:

- Disabled American Veterans (DAV)

- Bob Woodruff Foundation

- Disabled Veterans National Foundation (DVNF)

- Your state’s Department of Veterans Services

When you reach out, clarify whether you’re looking to purchase a new home or repair one you (or a family member) already own. That way, you can narrow down your grant options and find the right one fast.

Is a VA renovation loan a good option for you?

In many cases, a VA rehab loan can make buying and fixing a home easier. That said, these loans may not be the best choice if you want more control over your renovations.

In the table below, you’ll see a few more scenarios when a VA home improvement loan makes sense—and when it doesn’t.

| Consider a VA reno loan if you… | Reconsider if you… |

| Can meet credit and income qualifications | Don’t meet the VA’s service reqs |

| Are planning repairs that meet VA guidelines | Want cosmetic renovations, not structural |

| Know your repairs can be completed quickly | Can’t meet the 120-day deadline |

| Aren’t eligible for debt-free funding | Could use grant funding instead |

Remember that if you choose a different form of financing, you may need a second loan to cover your home repairs. Before proceeding, carefully consider how this extra debt may impact your credit and monthly budget.

How to select a VA renovation loan lender

Because VA loans are more heavily regulated than conventional mortgages, some loan elements may not vary much between lenders. For example, your origination fee will never be more than 1% of your loan amount, no matter which lender you choose.

Still, not every VA loan is exactly the same. That’s why it’s so important to prequalify with multiple lenders before officially applying.

Prequalifying lets you get personalized loan offers without impacting your credit. It’s a necessary step if you want to find the most affordable lender for your credit range. As you evaluate lenders, compare each one’s:

- APR

- Repayment terms

- Funding speed

- User-friendliness

- Customer service

To make the most informed decision, we suggest prequalifying with four to five lenders. By casting a wide net, you’ll be better assured that you’ve secured a VA loan at the best possible rate.

Use our mortgage calculator to determine your potential borrowing cost with the lenders you’re considering.

How to apply for a VA home improvement loan

Applying for a VA home improvement loan is similar to applying for other types of financing. There are a few key differences, though. Here’s what you’ll do:

- Request a Certificate of Eligibility (COE) from the VA. Your COE verifies that you meet the VA’s minimum service requirement. In most cases, you’ll need a copy of your DD214 to request a COE. Note that you can complete this step now on your own, or you can ask your lender to request your COE on your behalf.

- Gather your paperwork. You’ll need a government-issued photo ID, as well as recent bank statements, pay stubs, or tax returns. You don’t technically need these until you apply for your loan, but prepping your documents now will save time later.

- Check your rates with multiple lenders. If you’re interested in a lender that doesn’t allow prequalification, it’s still worth getting prequalified rates from lenders that do. You could use those as leverage if your preferred lender matches competitors’ rates.

- Submit an application. Once you’ve compared your prequalified offers and selected a lender, you’ll proceed with a full application. At this stage, you’ll upload your proof of income and identity. You’ll also consent to a hard credit check.

Filling out your lender’s application tends to be the quickest step in the process. Many of the best VA lenders offer streamlined applications that only take a few minutes to complete. However, how soon you receive your COE depends on how you request it.

You could get your COE in hand almost instantly if you request it online or through your lender. On the other hand, mail-in COE requests can take up to six weeks.

Once you’re preapproved, you can start shopping for homes. Remember, though, that VA rehab loans require both an initial appraisal and a post-repair inspection. After closing, work with your lender and your builders to ensure that repairs are completed quickly and to VA standards.

FAQ

What is a VA home renovation loan?

A VA home renovation loan enables veterans to finance both the purchase of a home and the cost of improvements with a single mortgage. This loan assists veterans in fixing or remodeling their homes while benefiting from advantageous VA loan terms. It includes low- or no-down-payment options and competitive interest rates.

Can you get specific home improvement loans for disabled veterans?

Yes, specific programs are designed to help disabled veterans make necessary home modifications. These include the Specially Adapted Housing (SAH) grant and the Special Housing Adaptation (SHA) grant. These grants provide funds essential for adapting homes to meet special needs, such as installing ramps, widening doorways, and modifying bathrooms.

What is a VA 203(k) rehab loan?

A VA 203(k) rehab loan doesn’t exactly exist: The 203(k) product is offered through the FHA. not the VA. However, VA’s renovation loans are similar. The VA allows veterans to finance both home purchases and renovations, bundling the costs into one manageable loan package.

Can I get a VA loan for a house that needs repairs?

Yes, you can obtain a VA loan for a house that needs repairs through the VA renovation loan program. This loan covers the purchase price and the necessary repairs, ensuring the property meets the VA’s minimum property requirements. This option lets veterans invest in fixer-uppers while securing affordable financing.

Recap of VA rehab loan lenders

| Lender | Loan amounts |

| Prime Lending | Up to $1 million |

| VA Nationwide | $50,000 or $200,000, or up to $2 million for extensive renovations |

| Cross Country Mortgage | $35,000 or less |

| Veterans United | $1.5 million and up with Jump Cash-Out Refi |

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.